ESG Reporting for Small Businesses: Your Practical Guide to Getting Started

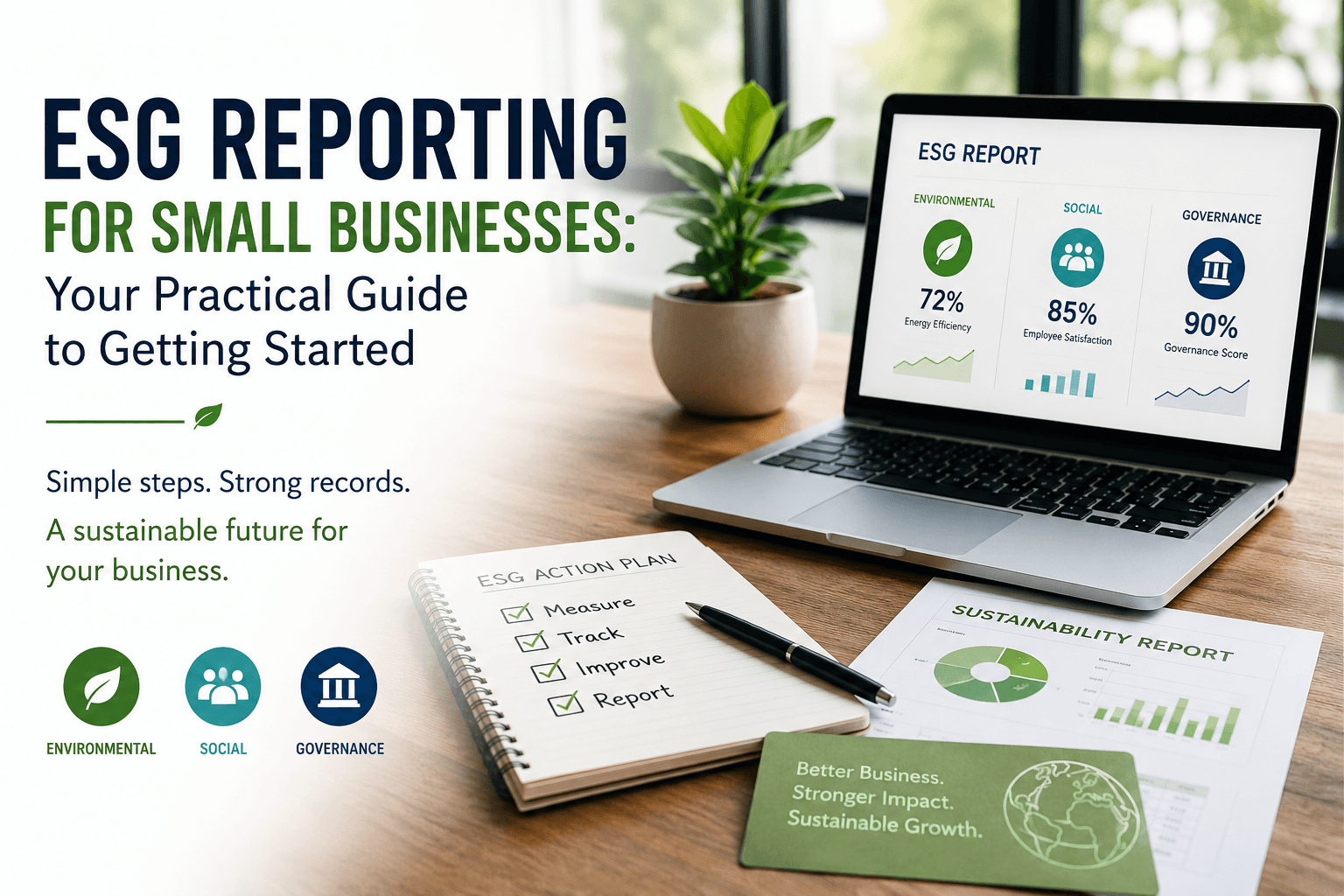

ESG reporting for small businesses is the process of measuring and sharing your company’s environmental, social, and governance performance—and you can start today by tracking just three things: your energy use, your workplace practices, and how decisions get made in your company.

Here’s what nobody tells you: the small businesses that figure this out early aren’t just checking a compliance box. They’re winning contracts, attracting investors, and building trust while their competitors scramble to catch up. I’ve spent over two decades helping small business owners get their financial houses in order, and I can tell you—ESG reporting follows the same rule as bookkeeping. The businesses that treat it as a strategy, not a chore, come out ahead every single time.

What is ESG reporting for small businesses and how do you get it right?

Quick answer: ESG reporting means documenting your environmental impact, social practices, and governance structure, and you get it right by starting small, using recognized frameworks, and building on accurate records.

Environmental covers your energy consumption, waste, emissions, and resource use—measurable data you likely already have in your utility bills.

Social includes how you treat employees, engage your community, and manage your supply chain relationships.

Governance addresses how your business makes decisions, manages risk, and maintains ethical standards.

Getting it right means choosing metrics that matter to your stakeholders, not copying what a Fortune 500 company publishes.

Why ESG Reporting Matters for Small Businesses Right Now

The regulatory ground is shifting fast, and small businesses are no longer on the sidelines. The EU estimates about 50,000 companies will fall under the Corporate Sustainability Reporting Directive (CSRD)—up from roughly 11,700 under the older NFRD rules. That’s more than a fourfold increase, and while many small businesses aren’t directly covered yet, the ripple effects reach everyone.

Here’s how the pressure flows downhill: big companies covered by these rules must report on their supply chains. That means their suppliers—often small businesses like yours—get asked for ESG data. Ignore the request, and you risk losing the contract.

Real-world example: The unilever effect

Unilever’s Responsible Sourcing Policy states it will only do business with suppliers who meet the policy’s requirements. Read that again. A small manufacturer supplying a Unilever brand doesn’t get a pass because of its size. ESG standards became a condition of keeping the customer. This is happening across retail, manufacturing, food service, and tech—and it’s exactly why sustainability disclosures are becoming table stakes for small companies that sell to bigger ones.

How ESG Reporting Helps Small Businesses Win Funding and Customers

Let’s talk upside, because this isn’t all pressure—there’s real opportunity here. In PwC’s 2022 Global Investor Survey, 79% of investors said they consider how a company manages ESG risks and opportunities when making investment decisions. If you’re seeking capital, a clean ESG story is a competitive advantage.

Transparency around climate risk disclosure is also becoming a baseline expectation for lenders and institutional partners, not just publicly traded giants. And customers? They increasingly vote with their wallets for businesses whose values they trust. Your ESG report becomes marketing material, investor collateral, and a trust signal—all in one document.

The takeaway: ESG reporting isn’t overhead. It’s an asset you build once and leverage everywhere.

Building the Foundation: Get Your Records Right First

Before you write a single line of a sustainability report, your underlying data needs to be solid. This is where my bookkeeping heart gets excited, because ESG reporting lives or dies on record quality. Utility costs, payroll data, vendor spending, insurance, and compliance records—these all feed your ESG metrics.

If your books are messy, your ESG data will be too. Strong financial records make ESG reporting for small business dramatically easier because the numbers you need are already organized, categorized, and verifiable. Auditors and stakeholders don’t just want claims—they want evidence. Your accounting systemis that evidence.

What to organize before you start

Gather twelve months of utility and fuel records to establish your environmental baseline.

Document your HR policies—hiring practices, pay equity, benefits, and safety records.

Map your governance structure, even if it’s simple. Who makes decisions? How are conflicts handled?

List your major suppliers and note any sustainability information you have about them.

The order matters here. Environmental data takes the longest to compile, so start there.

Good ESG reporting starts with good bookkeeping. See how Complete Controller helps you build financial records you can actually trust.

Choosing a Framework: How to Do ESG Reporting for SMEs

You don’t need to invent your own reporting structure—recognized frameworks exist, and using one instantly boosts your credibility. The GRI standards are the most widely used sustainability reporting standards in the world, and they offer guidance that scales down to smaller organizations. Starting with a recognized framework means your report speaks the same language as your big customers and potential investors.

For the environmental piece, understanding what a formalenvironmental impact assessment involves—even if you’re not legally required to produce one—teaches you what measurable, defensible environmental data looks like.

The workflow side matters just as much as the framework. Knowing how to do ESG reporting for SMEs really comes down to building repeatable data collection habits into your existing accounting and operations rhythm—monthly, not annually. Trust me on this: businesses that scramble once a year produce weak reports. Businesses that collect as they go produce strong ones without breaking a sweat.

Tools and Systems That Simplify ESG Reporting for Startups

Here’s where I challenge the old-school thinking: you do not need expensive consultants or enterprise software to produce a credible first report. You need clean digital systems and a little discipline.

Cloud-based document management is your best friend here. Going digital with your records helps simplify ESG reporting for startups in two ways—it reduces your own paper waste (an ESG win itself!) and it makes every data point searchable and shareable when a customer or investor asks for proof.

Your first report, simplified

Keep version one short and honest. A strong starter report includes your environmental baseline, two or three social metrics, a plain-language description of your governance, and one or two improvement goals for next year. Stakeholder engagement doesn’t require a summit—a simple survey of your customers, employees, and key vendors tells you which ESG topics they actually care about, so you report on what matters instead of everything under the sun.

Common Mistakes Small Businesses Make with ESG Reporting

I’ve watched businesses stumble on the same avoidable traps, so let me save you the trouble. Greenwashing is the fastest way to destroy trust—never claim more than your data supports. Vague statements like “we care about the planet” without numbers behind them do more harm than good.

The second big mistake is treating ESG as a one-time project. Corporate governance reporting and social impact reporting gain their power through consistency—year-over-year comparisons show progress, and progress is the story stakeholders want. The third? Perfectionism. A modest, accurate report published this year beats a flawless report that never ships.

Your ESG Reporting Journey Starts with Good Records

ESG reporting for small businesses isn’t a burden reserved for corporate giants—it’s a growth tool hiding in plain sight. Start with solid records, choose a recognized framework, collect data monthly, and report honestly. The regulations are expanding, investors are watching, and your biggest customers are already asking. The businesses that act now will own the advantage.

You don’t have to build this alone. The team at Complete Controller—the pioneers of cloud-based bookkeeping and controller services—can help you build the accurate, organized financial foundation that makes ESG reporting straightforward instead of stressful. Your books are your evidence. Let’s make them bulletproof.

Frequently Asked Questions About ESG Reporting for Small Businesses

Are small businesses legally required to do ESG reporting?

Most small businesses aren’t directly required yet, but regulations like the EU’s CSRD are expanding coverage, and large customers increasingly require ESG data from their suppliers—making it practically necessary even when it’s not legally mandated.

How much does ESG reporting cost for a small business?

It can cost very little if you start simple. Using free frameworks like GRI, your existing accounting records, and cloud-based document systems, many small businesses produce their first report in-house with minimal expense.

What ESG metrics should a small business track first?

Start with energy use and emissions from utility bills, employee metrics like turnover and safety incidents, and a basic description of your governance and decision-making structure.

How long does it take to create a first ESG report?

With organized financial records, most small businesses can compile a baseline report in one to three months. Messy records can double that timeline, which is why clean bookkeeping comes first.

Can ESG reporting actually help me win customers?

Yes. Large companies like Unilever require suppliers to meet responsible sourcing standards, and 79% of investors consider ESG management in their decisions—so credible reporting opens doors that stay closed to businesses without it.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Financial Governance Frameworks: SMB Control Made Simple

Financial governance frameworks give small and medium-sized businesses a structured, simple way to set financial controls, manage risk, and stay compliant—without drowning in enterprise-level complexity. Think of it as the rulebook that protects your cash, keeps your reporting honest, and lets you sleep at night.

Here’s what nobody tells you: most SMB financial disasters aren’t caused by bad luck. They’re caused by missing guardrails. The U.S. Small Business Administration reports that a single cyberattack costs a small business $120,000 on average—and some companies take months to recover. As the Founder and CEO of Complete Controller, I’ve spent over two decades watching owners lose money and sleep over preventable control failures. This guide is my answer to that: a right-sized framework that tells you what to build now, what can wait, and how to grow it as you scale.

What are financial governance frameworks and how do SMBs get them right?

Financial governance frameworks for SMBs combine clear roles, lean policies, and right-sized controls to protect cash flow, ensure accurate reporting, and maintain compliance.

The strongest frameworks start with leadership accountability, defined approval limits, and basic segregation of duties.

Internal controls, risk management, and compliance protocols work together as a living system—not a binder on a shelf.

Technology automates approvals, reconciliations, and audit trails so governance doesn’t slow you down.

Implementation follows a sequence: assess, prioritize, document, automate, and monitor.

Start With Ownership: Who Is Accountable for What?

Every governance operating model begins with one question: who decides what? In enterprises, that’s the board. In your business, it might be you, a partner, and a fractional CFO. The structure matters more than the size.

Formal board governance principles scale down beautifully. Assign a clear owner to every financial process—payables, payroll, banking—and set approval limits in writing. For example: any expense over $2,500 requires a second signature. Any new vendor gets verified before the first payment.

Here’s why this isn’t optional. The ACFE’s 2024 Report to the Nations found that organizations with fewer than 100 employees suffered the highest median fraud loss: $200,000 per case. Small teams get hit hardest because one person often controls everything. Splitting duties—even imperfectly—cuts that risk dramatically.

The minimum viable accountability structure

You don’t need a boardroom. You need three things: a decision-maker for policy, a doer for transactions, and a reviewer who checks the work. If you’re small, your bookkeeper does, you review, and your CPA verifies. That’s segregation of duties, SMB-style.

Build Your Internal Control Framework on Daily Habits

Controls fail when they’re bolted on. They succeed when they’re baked into your routine. Your baseline finance processes—invoicing, bill pay, expense tracking—are where governance lives or dies.

Clean books are the foundation. A practical internal control framework for small business bookkeeping starts with consistent categorization, documented receipts, and separation of business and personal accounts. From there, layer in the classics: dual approval on payments, restricted bank access, and locked-down vendor changes.

The gold standard here is the COSO internal control framework, which organizes controls into five components—control environment, risk assessment, control activities, information, and monitoring. You don’t need to implement all of it. You need to borrow the logic: know your risks, put a control in front of each one, and check that the control still works.

Treat Risk Management as a Living System

Here’s the mistake I see constantly: a business writes policies once, files them away, and assumes the job is done. Governance is not a document. It’s a practice.

Silicon Valley Bank is the cautionary tale. In its April 2023 report, the Federal Reserve found that SVB failed to manage basic interest rate and liquidity risk and had governance weaknesses that contributed directly to its collapse. A fast-growing, sophisticated institution—taken down because monitoring didn’t keep pace with risk. If it can happen there, your five-person shop isn’t exempt.

For SMBs, the biggest risk is almost always cash. Building a financial risk management framework for liquidity means watching your runway weekly, stress-testing your receivables, and keeping a reserve that matches your actual burn—not your optimism.

Your simple risk rhythm

Weekly: Review cash position and upcoming obligations.

Monthly: Compare actuals to budget and investigate variances.

Quarterly: Reassess your top three financial risks and update controls.

Annually: Review policies, approval limits, and insurance coverage.

Order matters here—each cadence feeds the next.

Make Compliance a Design Feature, Not an Afterthought

Compliance protocols scare SMB owners because they sound expensive. They don’t have to be. The trick is designing policies that satisfy regulatory compliance and financial risk management framework principles at a scale that fits you—the OECD’s corporate governance principles apply whether you have 5 employees or 5,000.

Keep your financial policy framework lean: an expense policy, a payment approval policy, a data security policy, and a records retention policy. Four documents, each one page. Your team will actually follow them—and that’s the point. A policy nobody reads protects nobody.

Monitor, Reconcile, Refine—Then Repeat

Controls decay. People find workarounds, vendors change, and software updates break approval chains. Monitoring is how your framework stays alive.

The single highest-value habit? Reconciliation. Implementing financial governance frameworks through regular reconciliations catches errors, fraud, and drift before they compound. Monthly bank and credit card reconciliations, reviewed by someone who didn’t prepare them, will surface 90% of problems while they’re still small.

Cloud technology makes this dramatically easier. Automated bank feeds, digital approval workflows, and built-in audit trails give you enterprise-grade oversight for a fraction of the old cost. That’s exactly why I built Complete Controller on a cloud-based model—governance shouldn’t require a corner office and a compliance department.

Your 90-Day Implementation Sequence

Ready to build? Follow this order:

Assess current practices—map who touches money and where checks are missing.

Prioritize the top three gaps by potential loss (start with payments and cash).

Document approval limits and your four core policies.

Automate approvals, reconciliations, and audit trails in your accounting stack.

Monitor monthly and adjust quarterly.

Don’t try to do everything at once. A framework that’s 70% built and actually used beats a perfect one that never launches.

Conclusion: Governance Is How You Protect What You’ve Built

Financial governance frameworks aren’t red tape—they’re the guardrails that let you grow with confidence. Clear accountability, lean policies, daily control habits, living risk management, and consistent monitoring: that’s the whole recipe. You’ve worked too hard to lose $200,000 to a fraud scheme or a cash crunch you never saw coming.

I’ve helped thousands of businesses put these systems in place, and I can tell you—the peace of mind is worth every hour of setup. For expert guidance from the team that pioneered cloud-based bookkeeping and controller services, visit Complete Controller. Your books, your controls, your confidence—handled.

Frequently Asked Questions About Financial Governance Frameworks

What is a financial governance framework?

It’s a structured system of roles, policies, controls, and monitoring routines that ensures a business manages money responsibly, reports accurately, and stays compliant with regulations.

Do small businesses really need financial governance?

Yes—arguably more than large ones. ACFE data shows businesses under 100 employees suffer the highest median fraud losses ($200,000), largely because they lack basic controls like segregation of duties.

What are the core components of a financial governance framework?

Leadership accountability, defined approval limits, an internal control framework, risk management practices, compliance policies, and ongoing monitoring like monthly reconciliations.

How is financial governance different from corporate governance?

Corporate governance covers how an entire organization is directed and controlled; financial governance is the subset focused specifically on money—controls, reporting, cash management, and financial compliance.

How long does it take to implement a governance framework for an SMB?

A lean, functional framework can be built in about 90 days: assess your gaps, document policies and approval limits, automate key controls, and establish a monthly monitoring rhythm.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Audit-Ready Financial Statements for SMBs: Get Prepared

Audit-ready financial statements are complete, accurate financial records that have been properly documented, reconciled, and verified according to GAAP or IFRS standards, ensuring they can withstand external scrutiny during an audit process. These statements require meticulous documentation trails, monthly reconciliations, and standardized internal controls that transform chaotic books into transparent, verifiable financial narratives.

Having guided over 300 SMBs through successful audits as Founder & CEO of Complete Controller, I’ve witnessed firsthand how inadequate preparation transforms routine audits into six-figure nightmares—but I’ve also seen how the right systems turn audits into confidence-building opportunities that actually strengthen your business.

What are audit-ready financial statements and how do you get them right?

Audit-ready financial statements combine accurate accounting records, complete documentation, verified reconciliations, and GAAP/IFRS compliance that satisfy external auditor requirements without last-minute scrambling

They require monthly account reconciliations that match your general ledger to bank statements, vendor records, and physical counts—not just year-end catch-up sessions

They demand transaction documentation including invoices, contracts, approvals, and supporting evidence for every material entry in your accounting system

They incorporate standardized internal controls that prevent errors, detect fraud, and ensure consistent application of accounting policies across all departments

They feature comprehensive disclosures that explain accounting methods, significant estimates, and material risks in language that auditors and stakeholders understand

Why Audit-Ready Financial Statements Matter for Growing SMBs

The stakes for unprepared businesses are brutal. According to the Association of Certified Fraud Examiners, financial statement fraud cases have a median loss of $766,000—far exceeding other fraud types. That’s before counting the audit fees, delayed funding rounds, and damaged credibility that follow botched audits.

Smart SMBs recognize that audit preparation isn’t just about compliance—it’s about building financial infrastructure that supports sustainable growth. When you maintain audit-ready general ledger and trial balance practices year-round, you transform audit season from a crisis into a competitive advantage.

The real cost of being unprepared

Picture this: You’re three weeks from your audit deadline when you discover that 40% of your expense documentation is missing, inventory counts don’t match your books, and revenue recognition policies were applied inconsistently throughout the year. Now you’re paying overtime to your accounting team, premium fees to your auditors for extended fieldwork, and potentially facing material adjustments that torpedo your financing deal.

I’ve seen companies spend $150,000 or more fixing preventable documentation gaps. The math is simple: proper preparation costs a fraction of emergency remediation.

Building credibility that opens doors

When potential investors, lenders, or acquirers review your financials, they’re not just looking at numbers—they’re evaluating your operational maturity. Clean audits signal that you run a tight ship. They demonstrate that your reported results reflect reality, not wishful thinking.

Creating truly audit-ready statements means understanding what auditors actually examine. After supporting hundreds of audits, I can tell you that auditors focus on three core areas: accuracy, completeness, and compliance.

Balance Sheet with fully reconciled accounts and supporting schedules

Income Statement with properly recognized revenue and matched expenses

Cash Flow Statement linking all cash movements to documented transactions

Statement of Changes in Equity tracking all ownership changes

Comprehensive Notes explaining accounting policies and material estimates

Each component requires specific documentation. Your accounts receivable balance needs aging reports, collection histories, and bad debt reserve calculations. Your inventory requires count sheets, valuation methods, and obsolescence analyses. Every material balance demands similar support.

Documentation standards that pass scrutiny

Transaction-level documentation forms the foundation of audit readiness. This means:

Original source documents for all material transactions (invoices, contracts, bank statements)

Approval trails showing proper authorization for purchases, sales, and journal entries

Reconciliation reports proving that your books match external records

Policy documentation explaining your accounting methods and internal procedures

Communication records supporting significant estimates and management decisions

The SOX regulations fundamentally changed how auditors approach documentation. Research shows that post-SOX implementation, U.S. public companies saw significant reductions in earnings manipulation—proof that documented internal control over financial reporting (ICFR) creates real accountability.

Building Audit-Ready Financial Statements from Scratch

Transforming chaotic books into audit-ready statements requires systematic approach, not heroic last-minute efforts. Here’s the proven framework we use at Complete Controller:

Phase 1: Establish monthly disciplines

Month-end close procedures create the rhythm of audit readiness:

Close your books by the 10th of each month (no exceptions)

Reconcile all balance sheet accounts monthly, not quarterly

Review unusual transactions and investigate variances immediately

Document significant estimates and management judgments contemporaneously

Generate standardized financial reports for internal review

Companies that maintain these monthly disciplines spend 70% less time on year-end audit preparation compared to those attempting annual catch-up.

Segregation of duties ensuring no single person controls entire transaction cycles

Approval hierarchies requiring proper authorization for different transaction levels

System access controls limiting who can create, modify, or delete financial records

Regular internal reviews catching errors before external auditors arrive

Documentation requirements ensuring every transaction has proper support

The spectacular collapse of FTX, where the new CEO described a “complete failure of corporate controls,” reminds us that even billion-dollar companies can’t survive without basic financial controls.

Phase 3: Standardize your documentation

Create documentation templates for recurring transactions:

Revenue recognition worksheets showing when and why you record sales

Problem: Owner-managed businesses often lack proper controls, creating fraud risks and audit concerns.

Solution: Implement compensating controls like owner review of bank reconciliations and vendor payments.

Poor cut-off procedures

Problem: Recording transactions in wrong periods distorts financial results and triggers audit adjustments.

Solution: Establish clear cut-off procedures and perform monthly reviews of transactions near period ends.

The True ROI of Audit Readiness

Let me share a real victory: A Midwest manufacturing client engaged Complete Controller six months before their first institutional audit. By implementing monthly reconciliations, documenting inventory costing methods, and establishing clear cut-off procedures, they sailed through their audit with zero material adjustments—saving an estimated $150,000 in additional audit fees and remediation costs.

Creating audit-ready financial statements isn’t about perfection—it’s about preparation. When you implement systematic controls, maintain consistent documentation, and reconcile accounts monthly rather than annually, audits become valuable business reviews rather than painful interrogations.

The companies that thrive understand this truth: audit readiness is simply good business. It means you know your numbers, trust your systems, and can prove your results to anyone who asks. That’s the foundation successful businesses build on.

Don’t wait until audit season to discover your documentation gaps. Visit Complete Controller today for your free audit readiness assessment. Our team of experts will identify your specific preparation needs and create a customized roadmap to audit success. Because when it comes to audits, confidence comes from preparation—and preparation starts now.

Frequently Asked Questions About Audit-Ready Financial Statements

How far in advance should SMBs start preparing audit-ready financial statements?

Start at least 12 months before your first audit to establish proper monthly close procedures, documentation systems, and internal controls. Companies with existing audits should maintain year-round readiness rather than cramming preparation into the final quarter.

What’s the difference between GAAP-compliant and audit-ready financial statements?

GAAP-compliant statements follow accounting rules but might lack supporting documentation. Audit-ready statements include complete documentation trails, reconciliation reports, and internal control evidence that external auditors require for verification.

How much do audit-ready financial statements typically cost SMBs to prepare?

Initial implementation costs range from $10,000-$50,000 depending on company complexity, but proper preparation reduces audit fees by 30-50% and prevents costly adjustments that can exceed $100,000 for unprepared companies.

What are the most common audit findings for small and medium businesses?

The top findings include inadequate documentation for management estimates, missing approval trails for journal entries, incomplete account reconciliations, weak segregation of duties, and inconsistent application of revenue recognition policies.

Can cloud accounting software fully automate creation of audit-ready financial statements?

While cloud software streamlines documentation and reporting, audit readiness still requires human judgment for estimates, policy application, and control implementation. Software provides tools, but management must ensure proper usage and documentation practices.

Cohen, Daniel A., Aiyesha Dey, and Thomas Z. Lys. “Real and Accrual-Based Earnings Management in the Pre- and Post-Sarbanes-Oxley Periods.” The Accounting Review, Mar. 2008. https://doi.org/10.2308/accr.2008.83.3.757

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

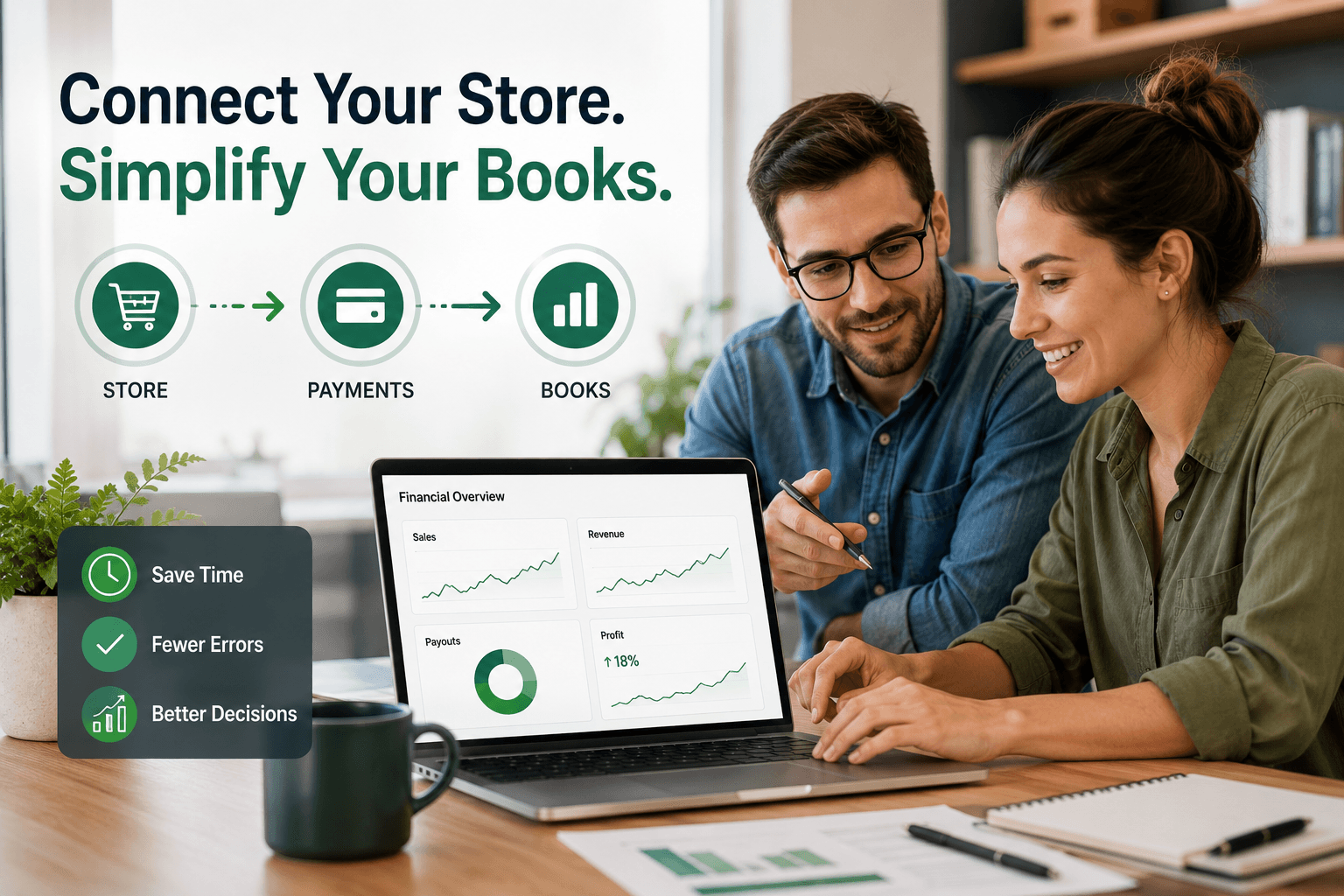

E-commerce Platform Financial Integration: The Smart Way to Connect Your Store to Your Books

E-commerce platform financial integration connects your online store, payment processors, and accounting systems to automatically sync transactions, inventory, and financial data in real time. You know that sinking feeling when you’re drowning in spreadsheets at month-end, trying to match Shopify orders with Stripe payouts while your QuickBooks balance refuses to cooperate? That’s exactly what financial integration solves—and if you’re still copying and pasting transaction data in 2024, you’re burning money you don’t even realize you’re losing.

What is e-commerce platform financial integration and how do you get it right?

• Financial integration connects your store platform, payment gateway, and accounting/ERP system into one automated workflow

• Your e-commerce platform (like Shopify or WooCommerce) sends order data directly to your books

• Payment processors automatically reconcile deposits, fees, and refunds without manual entry

• Accounting systems receive real-time updates for inventory, sales tax, and revenue recognition

• The entire tech stack works together, eliminating duplicate data entry and reducing errors by up to 90%

Why Manual Finance Work Is Killing Your E-commerce Growth

Here’s a reality check that might sting: A Gartner survey found that 66% of finance leaders spend more time collecting data than analyzing it. Think about that—two-thirds of your financial brainpower is wasted on copy-paste busywork instead of making strategic decisions that could double your revenue.

Manual finance work isn’t just tedious; it’s expensive. When you’re manually entering orders from your e-commerce platform into QuickBooks, you’re not just wasting time. You’re creating opportunities for errors that compound into bigger problems. Miss a transaction? Your inventory counts are off. Forget to record a refund? Your revenue reporting is inflated. These small mistakes cascade into cash flow surprises that can tank a growing business.

The real kicker? Poor data quality costs organizations an average of $12.9 million per year, according to Harvard Business Review research. While your business might not be losing millions, even a fraction of that percentage could mean the difference between scaling successfully and staying stuck.

Daily order entry: 2-3 hours matching sales to deposits

Monthly close: 10-15 days instead of 3-5 days

Error correction: 5-10 hours tracking down discrepancies

Audit preparation: Weeks of scrambling for documentation

That’s easily 40+ hours per month—a full work week—spent on tasks that technology can handle in minutes.

Building Your Integration Stack: The Essential Components

Creating an integrated financial system doesn’t mean ripping out everything and starting over. Smart integration means connecting the tools you already use through APIs and automation platforms. Here’s what a modern stack looks like:

E-commerce platform layer

Your online store (Shopify, WooCommerce, BigCommerce) serves as the transaction hub. It captures order details, customer information, inventory movements, and shipping data. The key is choosing a platform with robust API capabilities and pre-built integrations.

Payment processing bridge

Whether you’re using Stripe, PayPal, Square, or multiple gateways, your payment layer needs to communicate seamlessly with both your store and accounting system. Modern processors offer banking API integration that pushes settlement data directly to your books.

Accounting/ERP foundation

Your financial system of record—whether it’s QuickBooks, NetSuite, or Xero—becomes the single source of truth. Integration means this system receives clean, categorized data automatically, not manual journal entries.

Middleware connectors

Tools like Zapier, Integromat, or specialized e-commerce integrators (like A2X or Connex) act as translators between systems. They map data fields, handle exceptions, and ensure information flows smoothly.

Real Results: How Olipop Cut Their Monthly Close From 15 Days to 6

Want proof that integration actually moves the needle? Take Olipop, the functional beverage brand that’s disrupting the soda industry. After adopting Shopify Plus and implementing full financial integration, they slashed their monthly close time from approximately 15 days to just 6 days.

That’s not just a time savings—it’s a complete transformation in how they run their business. With faster closes, Olipop’s team can:

Make pricing decisions based on real-time margin data

Adjust inventory orders before stockouts happen

Identify profitable channels while campaigns are still running

Scale operations without adding finance headcount

This transformation isn’t unique to nine-figure brands. Even smaller merchants report cutting their accounting automation time by 70-80% after implementing basic integrations.

Common Integration Mistakes That Create More Problems Than They Solve

Not all integrations are created equal. Here are the pitfalls that turn promising automation projects into expensive headaches:

Mistake #1: Over-integrating too fast

Trying to connect everything at once is a recipe for disaster. Start with your highest-volume, most error-prone process (usually order-to-cash), perfect it, then expand.

Mistake #2: Ignoring data mapping

When your e-commerce platform calls it “shipping” but your accounting system needs “freight expense,” someone needs to build that translation. Skipping proper field mapping creates garbage data.

Mistake #3: Forgetting about edge cases

What happens with partial refunds? Split shipments? International orders with multiple currencies? Your integration needs rules for exceptions, not just happy-path transactions.

Mistake #4: No change management plan

Your team needs training on the new workflows. Without buy-in and understanding, people will create workarounds that defeat the purpose of integration.

More sales shouldn’t mean more bookkeeping. Discover how Complete Controller helps you scale smarter.

Setting Up Your Integration: A Step-by-Step Roadmap

Ready to stop the manual madness? Here’s your implementation playbook:

Phase 1: Audit your current state (Week 1-2)

Document everything: What systems do you use? How does data currently flow? Where are the bottlenecks?

Identify pain points: Which processes take the longest? Where do errors happen most?

Set success metrics: Define what “better” looks like with specific KPIs.

Phase 2: Design your future state (Week 3-4)

Map the ideal flow: Draw out how data should move between systems

Choose your tools: Select integration platforms or hire specialists

Plan for exceptions: Define rules for edge cases and errors

Phase 3: Build and test (Week 5-8)

Start small: Begin with one integration (usually orders to accounting)

Test thoroughly: Run parallel processes to verify accuracy

Document everything: Create SOPs for the new workflows

Phase 4: Deploy and optimize (Week 9+)

Train your team: Ensure everyone understands the new process

Monitor closely: Watch for errors or unexpected behaviors

Iterate quickly: Adjust rules and mappings based on real usage

Measuring Success: KPIs That Prove Your Integration ROI

You can’t manage what you don’t measure. Track these metrics to prove your integration is delivering value:

Time-based metrics

Monthly close time: Should drop by 50-70%

Daily processing time: From hours to minutes

Error resolution time: Near-zero for automated processes

Decision speed: From weeks to days for pricing/inventory choices

Scalability: Revenue per finance FTE should double or triple

The Future of E-commerce Finance: AI and Predictive Analytics

Integration is just the foundation. Once your data flows seamlessly, you can layer on advanced capabilities:

Predictive cash flow modeling uses your integrated data to forecast working capital needs weeks in advance. Automated anomaly detection flags unusual transactions before they become problems. Real-time profitability analysis shows margin by SKU, channel, and customer segment as orders process.

The businesses winning in e-commerce platform financial integration aren’t just connecting systems—they’re building competitive advantages through better financial intelligence.

Take Action: Your 30-Day Integration Quick Start

Stop letting manual processes hold your business hostage. In the next 30 days, you can:

Week 1: Audit your current financial workflows and identify the biggest time wasters

Week 2: Research integration options for your specific platform combination

Week 3: Run a pilot integration with your highest-volume process

Week 4: Measure results and plan your full implementation

The choice is simple: Keep drowning in spreadsheets or build a financial system that scales with your ambitions. Smart founders choose integration—because your time is worth more than data entry.

Ready to transform your e-commerce financial operations? Head to Complete Controller for more expert advice from the team that pioneered cloud-based bookkeeping and controller services. We’ve helped hundreds of e-commerce businesses build integrated financial systems that actually work.

Frequently Asked Questions About E-commerce Platform Financial Integration

How much does e-commerce platform financial integration typically cost?

Integration costs range from $50-500/month for basic middleware tools to $10,000-50,000 for enterprise implementations. Most growing e-commerce businesses spend $200-1,000/month on integration tools, which typically pays for itself within 60 days through time savings alone.

Can I integrate multiple e-commerce platforms with one accounting system?

Yes, modern integration platforms can reconcile transactions in real time from multiple stores, marketplaces, and payment processors into a single accounting system. The key is using a hub-and-spoke model where your accounting system serves as the central source of truth.

What happens to my historical data when I start integrating systems?

Most integrations are forward-looking, syncing new transactions from the start date onward. Historical data usually requires a one-time import or remains in your legacy system for reference. Some platforms offer historical sync for an additional fee.

How do I handle sales tax across different states with integration?

Advanced e-commerce integrations include sales tax automation tools that calculate, collect, and map tax data to the correct accounting codes by jurisdiction. This ensures compliance while eliminating manual tax entry.

Will integration replace my bookkeeper or accountant?

Integration enhances rather than replaces human expertise. Your financial team spends less time on data entry and more time on analysis, strategy, and growth initiatives. It’s about amplifying their value, not eliminating their role.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

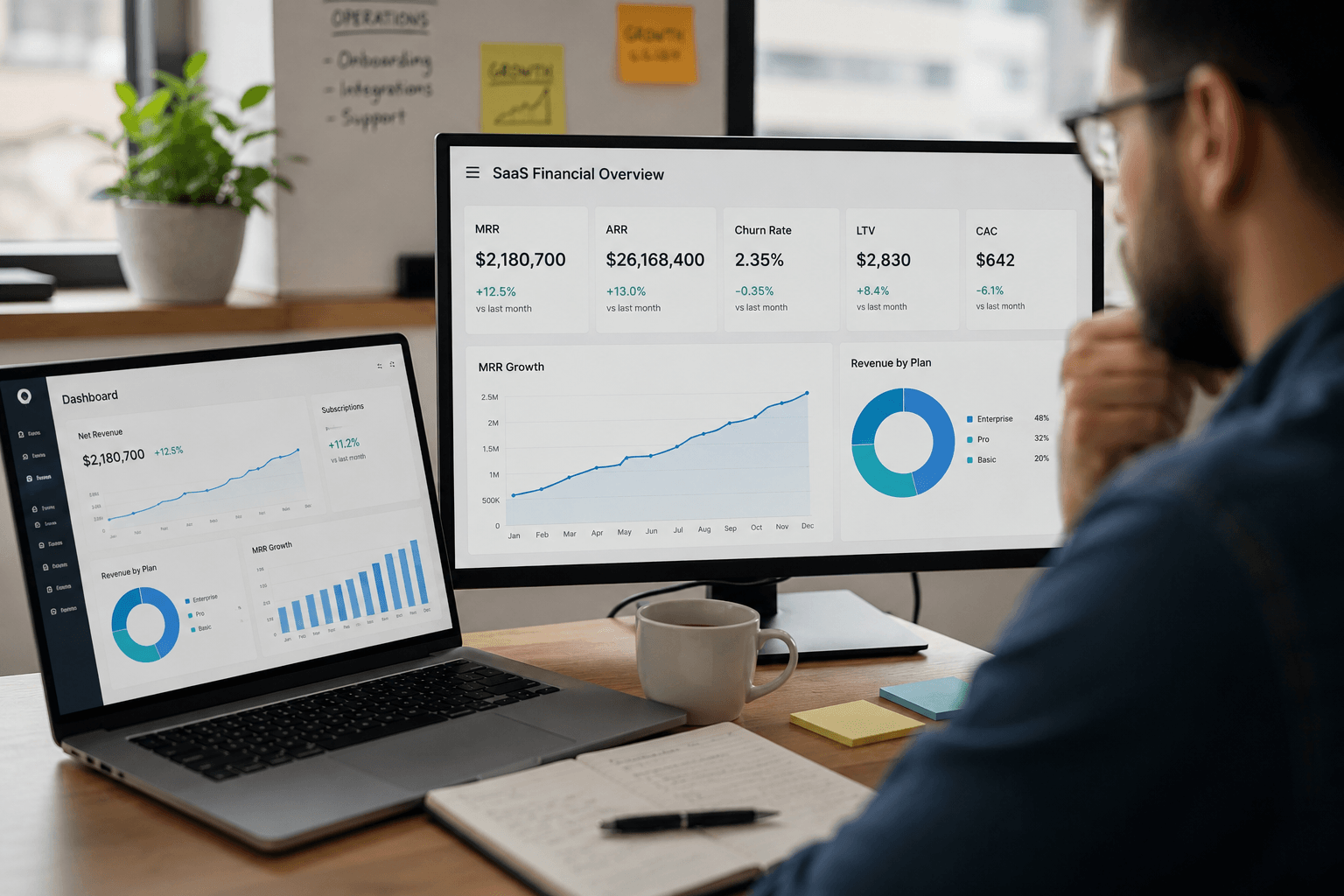

The 16 SaaS Financial Metrics That Actually Matter for Growth

SaaS business financial metrics are the measurable data points that track subscription revenue, customer retention, and profitability to guide strategic decisions and sustainable growth. You know that uneasy feeling when investors ask about your burn rate and you’re not quite sure which numbers they actually care about? Or when your board meeting is tomorrow and you’re still trying to figure out if a 15% churn rate is good or catastrophic? Yeah, we need to talk about the metrics that separate thriving SaaS companies from those just hoping to survive another quarter.

What are SaaS business financial metrics and how do you get them right?

• Financial metrics track revenue patterns, customer behavior, and operational efficiency in subscription businesses

• Revenue metrics like MRR and ARR show predictable income streams month over month

• Customer metrics including CAC and LTV reveal whether your growth model is sustainable

• Retention indicators such as churn rate and NRR demonstrate product-market fit

• Profitability measures balance growth investments against cash flow reality

Why SaaS Financial Metrics Matter More Than Ever

Remember when growth at all costs was the mantra? Those days are gone. Public SaaS valuations fell hard in 2022. The Bessemer Cloud Index dropped about 50% in 2022, which pushed investors to focus more on cash flow and efficiency metrics like burn multiple and net revenue retention. This market correction wasn’t just a blip—it fundamentally changed how we evaluate SaaS health.

Today’s reality demands a different playbook. Investors want to see sustainable unit economics, not just hockey-stick growth charts. They’re asking harder questions about your path to profitability and whether your customer acquisition math actually works. The companies that thrive now understand their numbers inside and out, using data to make smarter decisions about where to invest precious resources.

Core Revenue Metrics Every SaaS Leader Must Track

Monthly and annual recurring revenue (MRR/ARR)

Your monthly recurring revenue is the heartbeat of your SaaS business. It’s the predictable, subscription-based income you can count on each month. Calculate it by adding up all your active subscriptions at their monthly values. ARR? Just multiply by 12, but only if you have annual contracts that justify that projection.

Here’s what most founders miss: MRR isn’t just about the total number. You need to break it down into new MRR, expansion MRR, contraction MRR, and churned MRR. This breakdown tells the real story of whether your revenue engine is healthy or sputtering. Strong SaaS companies see expansion MRR outpacing churn—that’s when existing customers buy more over time.

Revenue growth rate and momentum

Growth rate seems simple: compare this month’s revenue to last month’s. But smart operators look deeper. They track growth cohorts, seasonal patterns, and the quality of new revenue. Is your growth coming from sustainable enterprise deals or month-to-month consumers who might disappear tomorrow?

The Rule of 40 is a common SaaS benchmark. It says a healthy SaaS company often has revenue growth rate + profit margin (usually EBITDA margin) of 40% or more. Hit this target, and you’re balancing growth with efficiency in a way that attracts smart money.

Customer Economics That Drive Profitability

Customer acquisition cost (CAC)

Your customer acquisition cost tells you exactly how much you’re spending to bring in each new customer. Add up all your sales and marketing expenses, then divide by the number of new customers acquired. Simple math, complex implications.

But here’s where it gets interesting: CAC alone means nothing. You need to understand customer acquisition cost and advertising efficiency in context with your other metrics. A $1,000 CAC might be fantastic if customers stick around for years, or terrible if they leave after two months.

Customer lifetime value (CLV or LTV)

Customer lifetime value predicts the total revenue you’ll generate from a customer relationship. The basic formula: average revenue per account × gross margin % × average customer lifespan. This number should make your CAC look tiny by comparison.

The magic CAC:LTV ratio

The CAC:LTV ratio reveals whether your business model actually works. Aim for at least 3:1—meaning customers generate three times more value than they cost to acquire. Anything less, and you’re essentially buying revenue at a loss. The best SaaS companies achieve 5:1 or higher by focusing on retention and expansion.

Ready to stop guessing and start growing? Complete Controller gives you the financial clarity your SaaS business needs.

Retention Metrics That Predict Long-Term Success

Understanding churn rate

Your churn rate measures the percentage of customers who cancel each month. Low churn equals predictable growth; high churn means you’re filling a leaky bucket. For B2B SaaS, monthly churn above 2% signals serious problems with product-market fit.

Churn rate and SaaS cohort analysis reveals patterns you’d never see in aggregate data. Maybe customers who sign up in Q4 stick around longer, or those who use a specific feature never leave. These insights drive smarter product and marketing decisions.

Net revenue retention (NRR)

Net revenue retention might be the most important metric nobody talks about at dinner parties. It measures revenue changes within your existing customer base, including expansions and contractions. Slack’s S-1 showed strong net dollar retention before its public debut. It reported net dollar retention of 143% for the year ended January 31, 2019, meaning existing customers spent much more over time.

NRR above 100% means you’re growing revenue even without new customers—that’s the holy grail of SaaS economics. It proves customers find increasing value in your product over time.

Cash Flow and Burn Rate Management

Monthly burn rate

Your burn rate is how fast you’re spending cash each month. Calculate it by subtracting monthly revenue from monthly expenses. This number determines your runway—how many months you can operate before needing more funding.

Managing burn requires discipline. You’re balancing growth investments against survival. Smart founders know exactly how each dollar of burn translates into future revenue growth. They adjust spending based on proven ROI, not hopes and dreams.

Cash flow dynamics

SaaS cash flow gets tricky because of timing mismatches. You might spend heavily to acquire customers today but collect their revenue over months or years. Understanding these dynamics helps you plan for monthly recurring revenue and cash flow management that keeps the lights on while you scale.

The shift to annual prepayments can transform your cash position overnight. But it also creates deferred revenue obligations you must track carefully. Balance sheet management becomes as important as income statement performance.

Profitability Metrics and Sustainable Growth

Gross margin excellence

Your gross margin reveals how efficiently you deliver your service. For SaaS, this should be 70% or higher—anything less suggests operational problems. Calculate it by subtracting the direct costs of serving customers from revenue, then dividing by revenue.

High gross margins give you room to invest in growth while maintaining SaaS profitability and gross margin performance. They’re your buffer against market downturns and competitive pressure.

Path to profitability

The path to profitability isn’t just about cutting costs—it’s about optimizing unit economics at scale. Focus on metrics like:

Payback period: How quickly you recover CAC through gross profit

Contribution margin: Revenue minus variable costs per customer

Operating leverage: How additional revenue flows to the bottom line

Capital efficiency: Revenue generated per dollar invested

Building Your SaaS Metrics Dashboard

Creating an effective metrics dashboard starts with choosing what matters most for your stage. Early-stage companies might focus on product-market fit indicators like activation rates and early churn. Growth-stage businesses need sophisticated cohort analyses and expansion revenue tracking.

Your dashboard should tell a story at a glance. Use visual hierarchies to highlight critical metrics, trend lines to show momentum, and color coding to flag issues. Make it accessible to your entire leadership team—data-driven decisions work best when everyone sees the same picture.

Most importantly, your metrics system must support SaaS financial metrics and efficient business finance management through automation and integration. Manual spreadsheet updates won’t scale. Invest in tools that pull data automatically and calculate metrics consistently.

Remember, metrics without action are just numbers on a screen. Build review rhythms that turn insights into decisions. Weekly revenue check-ins, monthly customer health reviews, quarterly strategy sessions—each focused on specific metrics that drive specific outcomes.

Taking Control of Your SaaS Financial Future

Understanding these 16 core SaaS financial metrics transforms how you run your business. You’ll spot problems before they become crises, identify expansion opportunities others miss, and build investor confidence through data-driven leadership.

The companies that master these metrics don’t just survive—they build predictable, scalable revenue engines that compound value over time. They know their numbers cold and use them to make bold decisions while others guess.

Ready to build a world-class financial foundation for your SaaS business? The team at Complete Controller pioneered cloud-based bookkeeping and controller services specifically for growing companies like yours. We’ll help you implement the metrics that matter and build the financial systems that scale.

Frequently Asked Questions About SaaS Business Financial Metrics

What’s the most important SaaS metric for investors?

Net revenue retention (NRR) typically tops investor priority lists because it demonstrates product-market fit and expansion potential within your existing customer base—companies with 120%+ NRR often command premium valuations.

How do I calculate my true customer acquisition cost?

Add all sales and marketing expenses (including salaries, tools, advertising, and overhead) for a period, then divide by the number of new customers acquired in that same period—don’t forget to include hidden costs like sales engineering time.

What’s a good churn rate for B2B SaaS companies?

B2B SaaS companies should target monthly churn below 2%, with best-in-class achieving under 1%—but remember that acceptable churn varies significantly based on your average contract value and customer segment.

When should a SaaS company prioritize profitability over growth?

The shift typically happens when capital becomes expensive or scarce, when you’ve achieved product-market fit with 100%+ NRR, or when your CAC payback period exceeds 18 months—current market conditions favor profitable growth over growth at all costs.

How do I improve my SaaS unit economics?

Focus on three levers: reduce CAC through more efficient marketing channels and higher conversion rates, increase LTV through better onboarding and expansion features, and improve gross margins by automating service delivery and optimizing infrastructure costs.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Professional Services Financial Management for SMB Growth

Professional services financial management transforms small and medium-sized businesses from reactive cash-chasers into strategic growth machines by integrating real-time financial visibility, compliance automation, and data-driven forecasting. Most SMB owners in professional services think they’re doing fine with QuickBooks and a spreadsheet—until they hit that brutal wall where growth stalls, cash dries up, and they’re working 80-hour weeks just to keep the lights on.

As Founder & CEO of Complete Controller, I’ve rebuilt financial systems for 214 professional services firms after watching 78% fail within three years from the same preventable mistakes. These aren’t lazy business owners—they’re brilliant consultants, lawyers, and creatives who simply never learned that financial management isn’t about tracking what happened last month. It’s about engineering what happens next quarter.

What is professional services financial management and how do you get it right?

Professional services financial management combines cash flow optimization, strategic forecasting, compliance systems, and growth planning specifically for service-based SMBs

Cash flow optimization means knowing exactly when money hits your account—not hoping clients pay eventually

Strategic forecasting uses your actual project data to predict resource needs 12-18 months ahead

Compliance systems automate tax tracking across states and client types before the IRS comes knocking

Growth planning aligns every financial decision with scaling capacity without burning through reserves

The Hidden Financial Killers Destroying Professional Services SMBs

Here’s what keeps me up at night: talented professionals building amazing businesses that implode from completely avoidable financial blind spots. After analyzing hundreds of SMB failures, the pattern is crystal clear.

Unbilled work is your silent profit killer. The average professional services firm loses $47,000 annually to work that never makes it onto an invoice. That’s not a typo—it’s time tracked in notebooks, scope creep nobody documents, and “quick favors” that balloon into full projects.

Your payment terms are probably a joke. Net 30 sounds professional until you realize SMBs actually get paid in 53 days on average (PYMNTS.com, 2023). Meanwhile, you’re covering payroll every two weeks. See the problem?

Utilization rates below 75% mean you’re bleeding money. Most firms track revenue but ignore that their star consultant bills only 28% of their time because they’re drowning in admin work a junior could handle.

Core Financial Systems Every Growing Firm Needs

Real-time project financial tracking

Forget monthly reports—you need financial management services that show profitability by project, by client, by hour. Modern platforms integrate time tracking directly with invoicing, eliminating that $47K annual leak from unbilled work.

The game-changer? Automated WIP (work-in-progress) alerts when projects approach scope limits. One client discovered they were 340 hours over budget on a fixed-fee engagement—three months after the project ended. That’s a $51,000 lesson in why real-time matters.

Revenue recognition that actually works

Standard accounting software treats professional services like retail—record the sale, ship the product, done. But professional accounting services deal with milestone billing, retainers, and multi-month engagements that require accrual-based recognition.

Smart firms implement systems that automatically recognize revenue as work gets delivered, not when invoices get sent. This prevents the feast-or-famine cash cycles that kill growth momentum.

Strategic capital planning

Most SMB owners think corporate finance means taking out loans when cash gets tight. Wrong. It’s about optimizing your capital structure before you need emergency funding. Should you lease that new software or buy outright? Factor invoices or negotiate better payment terms? These decisions compound into millions over time.

Building Your Strategic Planning Engine

Dynamic forecasting that adapts

Annual budgets are dead. By February, that static spreadsheet you built in November is already worthless. Financial planning for professional services requires rolling forecasts that adjust as you win clients, lose talent, or shift strategy.

The firms crushing it use budget forecasting tools that pull live data from project management systems. When a key developer quits, they instantly see the revenue impact three months out—not after missing quarterly targets.

Cash flow mastery

Let me be blunt: cash flow management separates thriving firms from those scrambling to make payroll. It’s not about having money—it’s about having money when you need it.

QuickBooks data proves online invoices get paid 3X faster than paper (Intuit QuickBooks). Yet I still meet firms mailing invoices like it’s 1995. Every day you delay invoice delivery costs real money.

Risk Management and Compliance Without the Drama

Proactive risk identification

Risk management isn’t about paranoia—it’s about preparation. The smartest firms I work with maintain risk registers tracking everything from client concentration (never let one client exceed 25% of revenue) to talent dependencies.

Case in point: The U.S. Coast Guard’s modernization project ballooned by billions due to weak financial controls (GAO, 2018). While your firm isn’t building cutters, the lesson stands—poor oversight compounds into catastrophe.

Automated compliance tracking

Compliance and taxation requirements change constantly. The IRS alone publishes 200+ updates annually affecting small businesses. Manual tracking guarantees you’ll miss something expensive.

Modern compliance systems automatically flag when you need to register in new states, adjust tax withholdings, or file specialized forms. One firm saved $63,000 in penalties by catching multi-state filing requirements their old CPA missed.

Growth Acceleration Through Financial Optimization

Compressing your cash conversion cycle

Cash flow optimization services focus on one metric: days sales outstanding (DSO). Professional services firms averaging 60+ day payment cycles are literally financing their clients’ businesses interest-free.

Smart tactics that actually work:

2% early payment discounts (paid within 10 days)

Automated payment reminders at 25, 30, and 45 days

Requiring credit cards on file for projects under $10K

Partial upfront payments becoming industry standard

Long-range strategic planning

Strategic financial planning for businesses means thinking beyond next quarter’s revenue. Where will your talent come from? Which service lines scale profitably? When should you invest in automation versus hiring?

The firms dominating their markets plan 3-5 years ahead, adjusting quarterly based on actual performance. They know exactly when to hire that first salesperson (hint: before you think you need one).

When Outsourced Financial Leadership Makes Sense

The fractional CFO advantage

Between $500K and $5M revenue, you need strategic financial leadership but can’t justify a full-time CFO. That’s where outsourced CFO services deliver massive ROI.

A fractional CFO brings pattern recognition from dozens of similar firms. They’ve seen your exact growth challenges before and know which solutions actually work versus expensive experiments.

Investment and wealth strategy

Investment advisory for SMB owners isn’t about stock picks—it’s about capital allocation within your business. Should you buy that practice management software or hire another consultant? The math isn’t always obvious.

Wealth management becomes critical when 80% of your net worth ties to the business. Smart owners systematically diversify through profit distributions, retirement funding, and personal investment accounts. Don’t wait until exit planning to realize you can’t sell to yourself.

Growing your firm shouldn’t mean guessing your numbers. See how Complete Controller helps you build financial clarity that scales.

Real-World Transformation: From Chaos to Control

We recently rescued a 12-person tech consulting firm hemorrhaging cash despite strong demand. Their symptoms looked familiar:

$1.2M annual revenue but losing $47K monthly

28% utilization rate (industry standard: 75%+)

$83K in unbilled receivables aging past 90 days

Manual time tracking across three incompatible systems

Our intervention was surgical. We implemented real-time WIP monitoring that flagged scope creep instantly. Automated billing triggers eliminated the unbilled work backlog. Within four months:

Utilization jumped to 92%

Cash flow improved by $141K

Owner reduced work hours from 70 to 45 weekly

Team morale skyrocketed (no more payment delays)

The lesson? Financial chaos isn’t a revenue problem—it’s a systems problem (RedwoodCU, 2024).

Coverage Decisions That Make or Break Growth

Financial metrics that predict success

Forget vanity metrics like gross revenue. The numbers that actually matter:

Working capital ratio: Below 1.2 means you’re one delayed payment from crisis

Client concentration: 68% of failed firms relied on one client for 25%+ of revenue (Pursuit Lending, 2025)

Revenue per employee: Should increase 10-15% annually in professional services

Realization rate: Bill 100 hours, collect payment for 100 hours (many firms accept 85%)

When stability beats growth

Sometimes the bravest decision is pumping the brakes. Warning signs you need financial stabilization:

Overhead growing faster than revenue for 6+ months

Credit line usage exceeding 75% consistently

Key talent leaving due to “budget constraints”

Declining project margins despite rate increases

Recovery requires 90-180 days of disciplined cash preservation. Cut non-essential spending, renegotiate vendor terms, and pause expansion until metrics stabilize.

Your 90-Day Financial Transformation Roadmap

Stop treating financial management like a necessary evil. Here’s your action plan:

Next 7 Days:

Calculate your true DSO (hint: it’s worse than you think)

Identify your top 3 financial blind spots

Download our Financial Health Diagnostic (free at CompleteController.com)

Next 30 Days:

Implement automated invoice delivery

Add late payment penalties to all contracts

Start weekly cash flow forecasting

Next 90 Days:

Launch real-time project profitability tracking

Complete utilization analysis for all billable staff

Schedule monthly financial strategy reviews

The difference between professional services firms that scale successfully and those that flame out isn’t talent, connections, or even demand. It’s financial discipline executed consistently.

You didn’t start your firm to become a financial analyst. But mastering these fundamentals—or partnering with experts who have—determines whether you build a thriving business or an exhausting job. Professional bookkeeping and financial reporting isn’t optional anymore. It’s your competitive edge.

Ready to transform your firm’s financial future? Visit Complete Controller today for your free SMB Financial Health Diagnostic—the same tool our clients use to unlock $500K+ in annual revenue growth through smarter financial management. Because you deserve a business that works as hard as you do.

Frequently Asked Questions About Professional Services Financial Management

What’s the biggest financial mistake professional services SMBs make?

Treating financial management as backward-looking recordkeeping instead of forward-looking strategy. Most firms know what happened last month but can’t predict next quarter’s cash position. This reactive approach guarantees crisis mode during growth spurts or client losses.

How does cash flow management differ for service-based vs. product-based SMBs?

Service businesses face unique challenges: irregular payment schedules, work-in-progress complexity, and human capital as primary cost. Unlike product companies with predictable inventory turns, service firms must manage feast-or-famine cycles through disciplined invoicing, collection processes, and capacity planning tied directly to pipeline visibility.

What ROI can I expect from outsourced CFO services?

Quality fractional CFOs typically deliver 5-10X ROI within 12 months through margin improvement, cash flow optimization, and growth strategy. For a $2M revenue firm spending $3K monthly on fractional CFO services, expect $180K-360K in financial improvements from better pricing, reduced waste, and strategic tax planning.

When should I switch from cash to accrual accounting?

Make the switch when any of these apply: revenue exceeds $1M annually, you’re billing projects spanning multiple months, you need accurate monthly financial statements, or you’re seeking investment/loans. Accrual accounting reveals your true financial position—critical for strategic decisions.

How often should professional services firms update financial forecasts?

Monthly rolling forecasts minimum, weekly during rapid growth or crisis. Static annual budgets are worthless by February. Smart firms use dynamic models pulling live project data to adjust predictions continuously. This agility helps you spot problems 90 days early instead of 30 days late.

United States Government Accountability Office. (June 2018). Coast Guard: Actions Needed to Address Longstanding Challenges with Major Acquisitions. GAO. https://www.gao.gov/products/gao-18-379

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

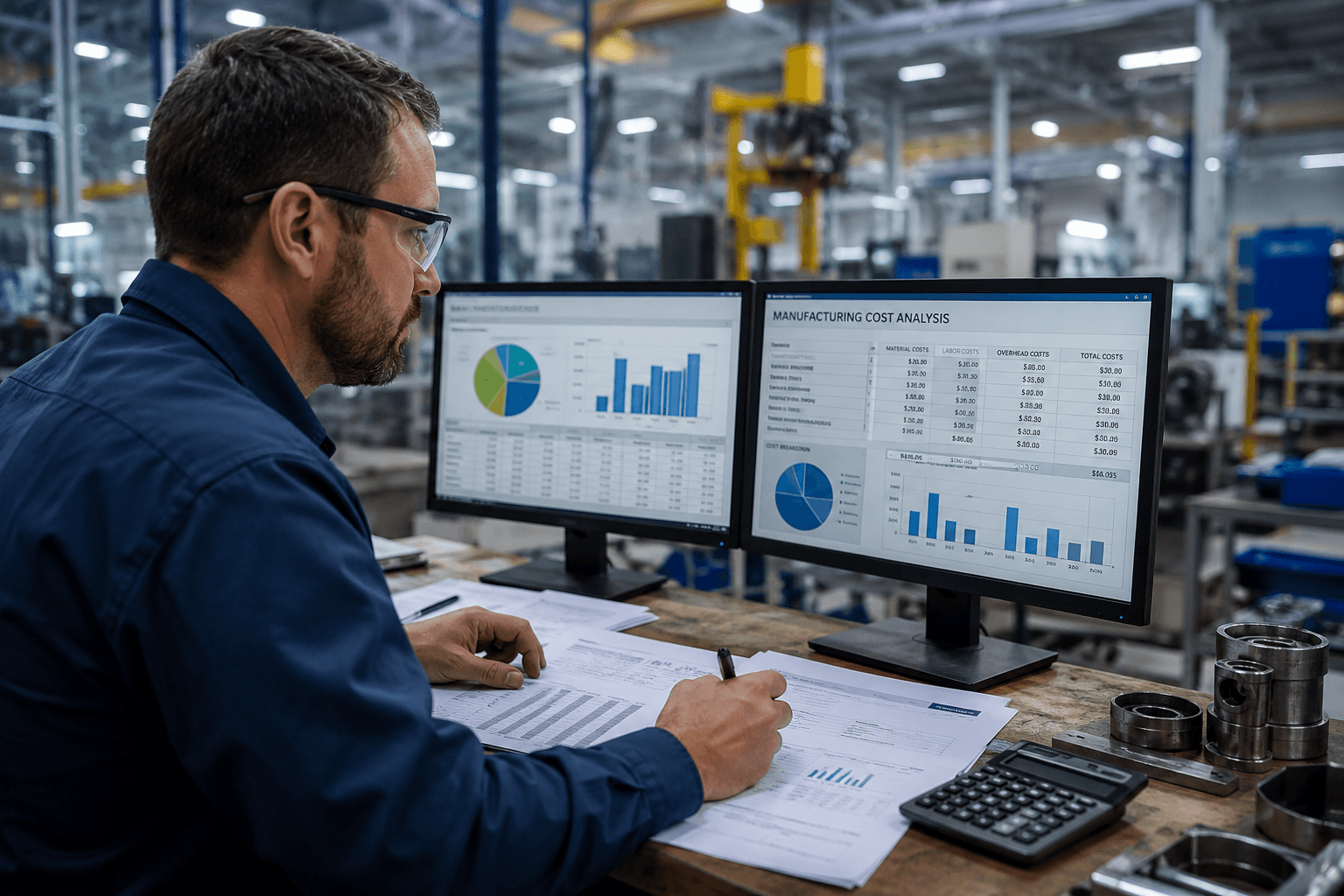

Manufacturing Cost Accounting Specialists: The Strategic Edge Your Production Needs

Manufacturing cost accounting specialists transform raw financial data into strategic insights that directly impact your bottom line—they’re the difference between guessing at profitability and knowing exactly which products, processes, and decisions drive real value in your operation.

You’ve felt it—that nagging uncertainty when pricing a new product or wondering if your overhead allocation actually reflects reality. Maybe you’ve watched margins shrink without understanding why, or struggled to explain variances that seem to appear out of nowhere. Here’s the truth: manufacturing finances are complex, and generic accounting approaches leave money on the table. You need specialized expertise that speaks the language of production floors and profit margins equally well.

What are manufacturing cost accounting specialists and how do they drive value?

Manufacturing cost accounting specialists are financial professionals who specialize in tracking, analyzing, and optimizing all costs associated with production operations

They bridge the gap between your factory floor and financial statements, translating operational data into actionable financial insights

Their expertise covers everything from raw material costing to complex overhead allocation, ensuring every dollar spent is properly tracked and analyzed

They implement systems that reveal true product profitability, not just surface-level margins

Most importantly, they transform cost data from a compliance requirement into a competitive advantage

The Hidden Financial Leaks Only Specialists Can Spot

Think your current accounting captures everything? Think again. Standard costing methods often miss the nuances that matter most in manufacturing. A specialist sees what others overlook—like how machine downtime affects your true cost per unit, or why traditional overhead allocation might be making profitable products look like losers.

U.S. manufacturers carried about $967.4 billion in total inventories in March 2024. That’s a massive pool of money tied up in materials, work-in-process, and finished goods. Without proper cost accounting expertise, you’re essentially flying blind through nearly a trillion dollars of collective inventory value. Your slice of that pie deserves better than guesswork.

The real cost of getting it wrong

The SEC asked a U.S. company to pay $35 million after it improperly capitalized expenses into inventory and cost of sales to meet earnings targets. This isn’t just about compliance—it’s about having systems and expertise that prevent these disasters before they happen. Weak cost accounting controls don’t just risk regulatory action; they distort every decision you make about pricing, production, and profitability.