Making a good plan

Planning is conditioning your behavior for a future programmed action in a strategic way. You certainly have several dreams if you are young and starting to structure your financial life. Is that a student exchange or a vacation trip? Buying a new car? Have money to open a business? All this is possible regardless of your salary. But, of course, if there is planning.

And there’s Luiz Barsi, who will not let us lie! With discipline and patience, in addition to well-defined goals within his investment strategy, he obtained more than R$1 billion on the stock exchange.

Create an expense control worksheet

Target detected an amount defined; it is time to understand how your salary will reach it, which goes through the elaboration of domestic budget control. A spreadsheet detailing your finances will help you review your priorities. More than that, it will make you realize that many expenses can be reduced or readjusted.

The simple structuring of personal finances makes it possible to reduce expenses by 20% to 30%. To do so, record all your expenses and income for a later critical evaluation of what can be resized.

Understand that the most successful know how to give up

You have already defined your target in the planning; you already know how much it costs and your monthly expense structure. It remains to measure the size of your financial sacrifice- how much you will have to save monthly to get where you want. Life is a game of loss and gain. In your case, this means that ensuring a certain monthly amount will certainly impose certain waivers.

In other words, that nightclub on Saturday, those daily Uber trips that are much more comfortable than taking public transport, that cool outfit you saw in the mall window last week, etc.

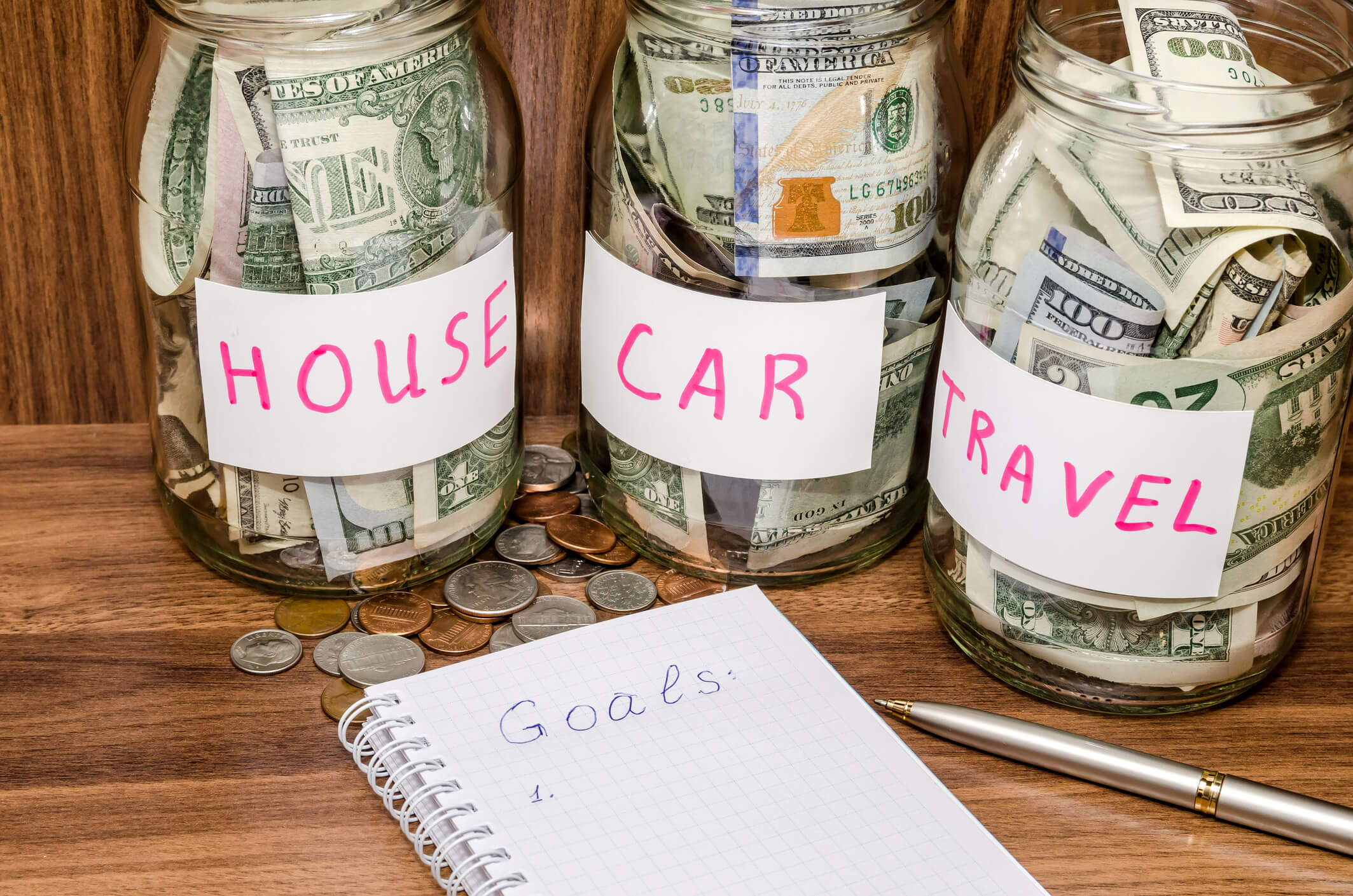

Set realistic goals

A warning: goals are not personal desires! I want to put all my salary together to buy a Ferrari, but I know it would be absurd to believe I can get through the month without spending a cent.

Be realistic; do not work with unrealistic dreams. Instead, stipulate feasible financial benchmarks, potentially concrete targets capable of materializing with effort, discipline, and determination. That is thinking about the long term.

Monitor your performance permanently

The process of building a stabilized financial life requires constant feedback. It is an incremental process, a dynamic path involving permanent readjustments, adjustments, and intense monitoring of your expenses to check if you are still on the right path.

It would be best to constantly reevaluate yourself to find new possibilities to generate income or save money. It is necessary to check if it could avoid any of the waivers to reinstate some expense that would be important to you and that, because you cut it, caused problems.

Believe in your ability to achieve set goals

Believe that you can materialize your planned goals. It would help if you had empathy with yourself. Rest assured: your disbelief in your ability to build something negatively conditions your actions, inducing you to weaken at crucial moments in your financial journey.

Many failures originate not in your pocket but in your mind, skeptical of the success of your audacious financial planning. It would be the case of someone with high financial goals, which impose heavy waivers on the consumption of essential items and involve changes in habits that are difficult to consolidate.

Be patient in pursuing your financial goals

We are taught to enjoy today and pay tomorrow. The culture of installment plans, financing, and overdrafts, almost non-existent in developed countries like Japan (where children learn to save early), usually slows our financial growth.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.