Every financially responsible adult should consider savings when they are planning their financial future. Surprisingly, most have a small savings or have not saved at all. When contemplating having savings, you will first need to know what you are saving towards.

Some will save for emergencies or job loss coverage, while others will save for college or large purchases, and still others for their retirement. No matter the reason you are saving, you have to plan to save enough money successfully.

Sadly, even though most know they should have at least one savings account, most have none because they believe they don’t have enough money to save. However, with financial planning and the help of having your savings automated, your savings can build even with a bit of money. Here is everything you need to know about automated savings.

Automated Savings Defined

As its name suggests, automated savings is a fixed savings that are deposited into a person’s savings account automatically, at fixed or specified intervals of time.

An automated savings plan automatically transfers from a bank account to a savings or an investment account after a fixed period. It can also be a fixed amount put directly into a savings account deposited from your payroll check.

How Does Automated Savings Work?

An automated savings plan is simple. An individual sets a fixed amount based on the total income to be deposited into a savings account. The fixed amount is then transferred from the salary account to the linked savings account of that individual. If the fixed savings is coming from your payroll check, you do not have to set regular intervals for the money to be deposited.

It will automatically deposit the set amount every paycheck. However, if your fixed savings is coming from another account, a fixed time interval must be set so that the fixed amount can be transferred at regular intervals. The time intervals can be daily, weekly, monthly, or specific dates.

Advantages of Automated Savings:

Set it, And Forget It

The first and the foremost advantage of automated savings is that once set, the individual can forget about it. It eliminates the need for people to worry about expenses as the amount is automatically transferred to the other account. Soon an individual may get used to the reduced amount and adjust the expenses in that specific amount forgetting about the automated savings.

Prevention of Unnecessary Expenditures

When a fixed amount from the income is cut off at regular intervals, it will help people avoid spending the money on unnecessary stuff. And as a person gets used to it, they will develop a habit of spending the money left on the things they need and not on things that are not required.

Emergency Funds

Life is unpredictable, and an emergency can arise at any time. Having emergency funds can make an emergency less stressful. With these automated savings, people will always have an emergency or backup fund, saving them from the worries of asking for help!

Using the Automated Savings to the Fullest

Automated saving is an intelligent step towards a prosperous and comfortable future. Therefore, an individual opting for this savings technique must plan to use it to its fullest potential. Here are some tips that can help people utilize this technique in the best way possible.

Reviewing the plan at regular intervals to see if the fixed amount can be increased

Having clarity by setting up clear short-term and long-term goals for automatic savings

Opting for a savings account that features a high yield ensures earning of the best APY on the money being saved

Avoiding the use of these savings until it’s the only option left

For people who wish to save but cannot draw a proper financial plan, these automated savings are the perfect way to go for it. Individuals must make sure that they are doing enough to secure their future, as life is unpredictable, and one must always be prepared for the worst! Therefore, think wisely and opt for automated savings.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Unlocking Wealth: The Psychology Behind Making Money

The psychology of making money encompasses the mental factors—perceptions, beliefs, attitudes, and behavioral controls—that shape our intentions and actions toward wealth accumulation, often moderated by motivation and external opportunities like post-Covid recovery. This complex interplay of cognitive, affective, and behavioral dimensions determines whether individuals aggressively pursue financial goals or unconsciously sabotage their own wealth-building efforts through negative money scripts and limiting beliefs about what’s possible for them financially.

As founder of Complete Controller, I’ve spent over two decades guiding small businesses through financial mazes, witnessing firsthand how mindset shifts unlock seven-figure growth for clients who once struggled with inconsistent cash flow. The transformation happens when business owners stop viewing money through the lens of scarcity or shame and start seeing it as a tool for impact and freedom. This article breaks down the core psychological drivers behind wealth creation, revealing how your brain’s wiring around money either accelerates or blocks your path to financial success—and more importantly, what you can do about it starting today.

What is the psychology of making money, and why does it matter?

Psychology of making money is the study of mental factors like perceptions of wealth, attitudes toward money, and behavioral control that influence intentions and actions to build wealth.

It explains why some people hustle relentlessly while others self-sabotage, rooted in cognitive beliefs about outcomes, affective emotions like excitement or anxiety, and behavioral dimensions.

Strong individual behavioral control has the highest impact on money-making intentions, fostering self-efficacy and opportunity-seeking.

Positive perceptions of wealth and the rich boost motivation, while post-Covid opportunities amplify these effects.

Understanding it empowers better financial decisions, reducing stress and enhancing life satisfaction through financial stability.

Core Psychological Drivers of Wealth Creation

Individual intentions to make money stem from perceptions of wealth as desirable, views of the rich as aspirational, and a belief in personal agency, all amplified by wealth motivation. These psychological factors don’t operate in isolation—they interact multiplicatively to create powerful behavioral patterns that either propel individuals toward financial success or trap them in cycles of underachievement.

Perception of wealth and its power to motivate

People who view wealth positively—seeing it as a path to self-actualization—are more likely to act on money-making opportunities, with studies showing a direct positive influence on intentions. Research examining 991 Vietnamese respondents in 2021 revealed perception of wealth significantly predicted money-making activities with a standardized coefficient of 0.193, meaning those who explicitly valued wealth showed substantially stronger pursuit of financial opportunities.

The power of wealth perception operates through fundamental psychological mechanisms:

When individuals see wealth as freedom, security, or ability to help others, they align money with meaningful values

Cultural messages framing wealth as corrupting activate “money avoidance” scripts

Those avoiding wealth often unconsciously self-sabotage opportunities

Guilt about earning creates neglect of financial management

Positive wealth perception combined with high motivation creates exponentially stronger behavioral intentions

Explicit and implicit perceptions of the rich

Explicit views (conscious beliefs that the rich are driven and successful) and implicit ones (subconscious biases from social exposure) both predict stronger money-making drive, especially in emerging economies. The 2021 Vietnamese study found explicit perceptions of the rich predicted wealth-building intentions with a coefficient of 0.124—those who consciously admired wealthy role models showed greater likelihood of pursuing financial success themselves.

This aspirational modeling connects to broader psychological principles of observational learning. When individuals witness others similar to themselves achieving wealth through effort and strategy, they develop self-efficacy beliefs—confidence in their capacity to achieve similar outcomes. Conversely, narratives painting wealthy people as fundamentally different diminish personal agency and reduce pursuit of available wealth-building strategies.

Individual behavioral control as the top predictor

Perceived control over financial outcomes—through skills, self-efficacy, and locus of control—has the strongest effect (β=0.358), mediating other perceptions into action. This means confidence in ability to control financial outcomes predicted money-making intentions nearly twice as strongly as other psychological factors examined.

Behavioral control encompasses multiple constructs:

Locus of control: belief that outcomes result from personal actions versus external forces

Financial self-efficacy: confidence in managing money effectively

Skills perception: belief in possessing necessary abilities for wealth building

Outcome expectations: conviction that efforts will produce results

Research shows individuals with internal locus of control demonstrate 11.3% higher savings rates, more frequent investment behavior, greater calculated risk-taking, and fewer overdue payments compared to those attributing outcomes to luck or fate.

Money Attitudes That Shape Your Wealth-Building Mindset

Money attitudes, multidimensional constructs blending emotions, beliefs, and behaviors, determine if wealth feels like freedom or a trap. These attitudes develop through childhood experiences, particularly “financial flashpoints”—emotionally intense events like parental job loss, divorce, or poverty that create deep associations between money and survival threat.

The four core money scripts: Avoidance, status, worship, and vigilance

Money avoidance leads to neglect of finances; status ties self-worth to net worth; worship chases endless spending; vigilance builds security but breeds anxiety.

These scripts trap people on the hedonic treadmill, where raises or purchases yield short-lived joy before baseline dissatisfaction returns.

Money Avoidance creates the most direct wealth-building obstacles. Avoiders view money as corrupting, experience guilt when earning, sabotage opportunities to maintain alignment with beliefs about not deserving wealth, and systematically fail to track finances or claim employer retirement contributions.

Money Worship perpetuates belief that acquiring more money solves all problems. Worshippers feel perpetual insufficiency regardless of wealth level, engage in compulsive spending, prioritize work over relationships, and experience diminished satisfaction despite financial success.

Money Status scripts tie self-worth to net worth, driving comparison-based spending for image projection rather than personal enjoyment. Status-seekers accumulate debt pursuing symbols, achieving less security than those with other scripts.

Money Vigilance supports accumulation through frugality and discipline but creates persistent anxiety about resource sufficiency, inability to enjoy money, and relationship conflicts over scarcity mindset.

Love of money: Motivator or ethical risk?

High “love of money” (seeing it as success, power, or richness) motivates harder work but risks unethical shortcuts without supervision. Studies show excessive focus on monetary gain correlates with reduced empathy, increased unethical behavior, and prioritization of self-interest over collective welfare—particularly among those already possessing substantial resources.

Great psychology needs great systems. Let Complete Controller bring structure to your financial growth.

Real-World Case Study: Vietnam’s Post-Covid Wealth Surge

In a 2021 study of 991 Vietnamese respondents, psychology of making money factors like behavioral control (β=0.358) and perception of wealth (β=0.193) strongly predicted intentions to build wealth, with post-Covid opportunities moderating these links—enhancing efforts amid economic rebound. The research revealed how external opportunities amplify internal psychology:

Motivated individuals leveraged new business openings

Economic recovery created multiplier effect on existing psychological drivers

Key takeaway: External opportunities don’t create wealth-building psychology from nothing—they amplify existing perceptions, attitudes, and sense of control. This explains why economic booms benefit some dramatically while others remain stuck in old patterns.

The Hidden Downsides: When Money Mindset Hurts Your Wealth and Health

Top SERPs overlook how negative focuses harm mental health—focusing solely on “making money” erodes relationships and well-being, unlike actual earnings which boost satisfaction. Research distinguishes between obsessing over money (harmful) versus actually earning it (beneficial).

Stress, shame spirals, and loss of empathy

Financial instability intensifies daily hassles via shame spirals, while wealth can reduce empathy and morality, changing self-perception toward entitlement. Studies demonstrate:

42% of US adults report money negatively impacts mental health

Financial stress increases absenteeism by 34%

Wealthy individuals show reduced compassion in experimental settings

Higher social class predicts increased unethical behavior

Overcoming the hedonic treadmill requires intentional mindset shifts, not just more income.

Why chasing money alone backfires for entrepreneurs

Excessive focus on earnings correlates with poorer mental health, but financial stability—via smart bookkeeping—frees mental energy for growth. The distinction matters: entrepreneurs who build systems for financial security experience greater well-being than those perpetually chasing the next dollar without underlying stability.

Practical Strategies to Rewire Your Psychology of Making Money

SERPs lack actionable roadmaps for business owners; here’s how to harness these insights at Complete Controller.

Build behavioral control with daily financial rituals

Track finances weekly using cloud tools to foster self-efficacy—clients see 30% faster wealth growth from this habit alone. Specific practices include:

Weekly profit/loss reviews with pattern identification

Monthly strategy sessions linking actions to outcomes

Quarterly celebrations of financial wins, reinforcing control beliefs

Shift money scripts through founder-tested exercises

Journal attitudes (e.g., “Money is…”) then reframe: From “Money is scarce” to “Money flows with smart systems.” I’ve used this with Complete Controller teams to boost retention and revenue. Additional techniques:

Create “evidence lists” of times your efforts produced results

Practice gratitude for current resources while planning growth

Partner accountability for maintaining new scripts

Leverage post-covid opportunities like a pro

Spot trends in remote services; motivation moderates perceptions into action—network boldly to multiply intentions. Current opportunities include:

Digital transformation creating new service demands

Remote work enabling geographic expansion

Supply chain shifts opening market gaps

Increased focus on financial resilience driving bookkeeping demand

The Role of Wealth in Long-Term Success

Wealth alters thinking: More money means less intense stress from hassles due to greater control, higher life satisfaction, and shifted social behaviors. Research reveals income improvements benefit the unhappiest individuals most dramatically up to $100,000 annually, while happier individuals see consistent gains across all income levels.

Where psychology meets behavioral economics in money decisions

Pricing and systems warp perceived value; train your mind to counter with objective tracking. Common cognitive biases affecting wealth building:

Anchoring on irrelevant price points

Mental accounting separating money artificially

Present bias overvaluing immediate rewards

Social proof driving comparison spending

For small business owners, psychological factors like optimism and conscientiousness predict high income—pair with expert bookkeeping for outsized results.

Final Thoughts

Mastering the psychology of making money means aligning perceptions, attitudes, and controls to turn intentions into wealth—avoiding pitfalls like shame spirals or hedonic traps while capitalizing on motivation and opportunities. The research is clear: behavioral control trumps all other factors, but it works best when combined with positive wealth perceptions and genuine motivation for financial growth.

As founder of Complete Controller, I’ve seen clients transform scarcity mindsets into abundance through these principles, scaling businesses sustainably. Start by auditing your money beliefs today, implement one behavioral ritual, and partner with pros who understand both the numbers and the psychology behind them. Ready to unlock your wealth potential? Visit Complete Controller for expert guidance that addresses both the financial and psychological aspects of business growth.

Frequently Asked Questions About Psychology of Making Money

What are the main factors influencing the intention to make money?

Perception of wealth, views of the rich, behavioral control, and wealth motivation, with external opportunities as moderators.

How does money attitude affect financial success?

Attitudes like vigilance build wealth, while avoidance or worship lead to cycles of debt and dissatisfaction.

Can focusing too much on making money harm you?

Yes—prioritizing earnings over relationships hurts mental health, unlike actual financial gains which improve well-being.

Does wealth change how empathetic or ethical people are?

Wealth often reduces empathy and shifts morality toward self-interest, per studies on status and behavior.

How can I improve my psychology of making money?

Build behavioral control via routines, reframe money scripts, and leverage opportunities with professional financial support.

Sources

Nguyen, Thi Phuong et al. “Investigating individual intention to make money: can motivation of wealth and post-Covid-19 opportunity create the difference?” PMC, 2023, pmc.ncbi.nlm.nih.gov/articles/PMC9969029/.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Finding new sources of income is essential for anyone who wants to have financial freedom. Currently, there are many ways to generate new sources of income. However, the simplest is to acquire assets, which generate passive income, as it is a way to generate income with little effort.

A financial asset is a resource that allows its owner to obtain future income and is usually issued by economic entities, whether companies, government, or others. Financial assets can be obtained through investments or businesses.

Basic Principles of a Financial Asset

The assets have several standard features related to each other; these characteristics are profitability, liquidity, and risk.

Cost-effectiveness

Cost-effectiveness represents the acceptance and interest that investors have in the asset. This will be affected by the benefits that can be obtained from the investment. This concept is the most relevant of a business because it will be possible to know the success that will be obtained from it.

Risk

Risk refers to the guarantee offered by the asset. This principle affects the return of the asset. Generally, the assets with a high level of risk do not insure the investment or capital of the individual. This higher risk is because the value of the said asset is volatile and can generate future losses.

Liquidity

Liquidity is the asset’s ability to transform into money without causing losses, while an asset that is more liquid will obtain greater profitability, thus becoming a risk-free asset. In this way, the relationship between the principles of assets is fulfilled.

What is Passive Income?

Passive income is the earnings generated without excessive work; if an investment generates income, indifferently from the amount of time its owner invests. Each amount generated as profit is known as passive income.

There are many ways to generate passive income. However, the fastest way is acquiring financial assets that generate passive income over time. However, these assets have a risk because there is the possibility of losing the investment made. It is fundamental to learn about the state of the asset that you intend to acquire since it is not something that should be taken lightly.

What are the most profitable assets to generate passive income?

Thanks to technological advances, it is increasingly easy for anyone with considerable capital to invest in assets that generate passive income. However, it is necessary to know the means of income that will be used. Currently, the most popular are the following:

Investment in Cryptocurrencies

Undoubtedly, cryptocurrencies are one of the most popular assets of today. This popularity is due to the exponential increase in profitability demonstrated by multiple cryptocurrencies in recent years. However, most cryptocurrencies have a relatively unstable value, leading an investor to earn a lot of money or vice versa; It can lead to losing everything.

The key to cryptocurrencies is to know when to buy them and wait for the right time to sell them. In addition, it must be borne in mind that it may be difficult to predict the value of the asset in this market due to the aforementioned instability.

Investment in Stock Shares

The shares are the first known financial assets. They represent a fraction of the capital stock, where the asset gives the holders or investors participation rights and income, depending on the state of the organization, the relation to the profits and losses.

To begin generating this asset, the company must study the total value of its organization. The value obtained is divided into equal units, and the result of that division is known as the shares, securities, or securities.

According to the fluctuation of the company’s value, investors and owners will obtain profits or losses, generally to generate significant passive income, concerning the shares of a company; it is necessary to study it since, after a specific time, the state of the company is maintained. That is why the best strategy will be to invest capital in shares of a company with potential and is relatively new in the market.

Aspects to Consider When investing in Financial Assets

The level of risk will be affected by the profitability of the assets, which is why it is necessary to study the asset in which it is expected to invest. Since there is an excellent variety of these, cryptocurrencies have greater acceptance because they are decentralized, net, and proportional to their investment.

On the other hand, the world of actions is broader than the crypto world. This broadness is due to the number of intermediaries that exist. To ensure the success of an investment in shares, it is necessary to seek advice, so business will be done with greater security, which generates additional costs apart from the investment.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Before 1911, the working conditions of employees in the United States of America were not very impressive. Things were worse for workers employed under powerful employers. During this era, employers did not offer any compensations for injuries incurred by an employee within the scope of performing a job.

The employees had to legally file a lawsuit against their employers, which was a rare case. A very few employees could file a lawsuit because of the expense. The chances of them winning the case were not that strong. The employers used strong defenses such as Contributory negligence, assumption of risks, or fellow employee negligence, which were very difficult to overcome.

Workers’ Compensation Insurance

Workers’ Compensation laws, referred to as the Grand Bargain, were introduced in 1911. It was after these laws the workers began to receive their due rights. The workers’ compensation insurance is a bargain between the employers and the employees. An employer provides the workers the benefits if they get injured, fall ill or die while on the job, and in return, the employers are safe from a legal lawsuit.

Types of Workers’ Compensation Insurance

There are different types of workers’ compensation insurance, including;

Medical Treatment

For injuries that need medical treatment, an employer is expected to pay for all the medical treatments required. If the recovery time exceeds the waiting period, an employer must also pay cash benefits for the time an employee misses the work. It is to cover up the lost income while an employee is unable to work. An employee who recovers within the waiting time gets medical treatment benefits only.

Rehabilitation

There are injuries when simply treating them with medical treatments is not enough. Sometimes for recovery, along with medical treatment, some rehabilitative services are required. In this case, an employee will have to cover the cost of all the rehabilitative therapies. Also, suppose the injury has caused an individual to be unable to return to the pre-injury job. In that case, workers’ compensation will provide benefits so that the individual can train for another position.

Disability

Four types of disabilities lie under workers’ compensation insurance. These four types include; temporary partial disability, temporary total disability, permanent partial disability, and permanent total disability, and based on these, the employer provides the benefits.

Temporary partial disability is when an employee cannot perform some tasks of the job for a specified period, temporary total disability is when the injury restricts a worker from doing the total job for a limited time. The permanent partial disability restricts a worker from doing some job tasks forever. In contrast, the permanent total disability means that an employee is no more capable of the pre-injury job.

The benefits paid to depend upon the income that the employee received before the injury. Generally, the amount is equal to two-thirds of the wage. An employee is not expected to pay tax over this income.

Death

If an employee dies during work in an unfortunate situation, a company is expected to pay death benefits to the deceased employee’s family. Spouse, children, parents, or siblings are the expected beneficiaries of these benefits. Some states also cover the funeral and burial costs. The total cost of these benefits depends upon how much a deceased employee contributed to the lives of their dependents.

These are the four basic types of insurance. The provisions of each of these types differ in every state. As the state is the body that sets the laws, all the states have different policies. Even though injuries are unexpected, an employer reserves the right to terminate an individual if they do not return to work for a long time.

In Georgia, it is a legal step to fire an injured employee. Therefore, both the entities, the employer, and the employees must know about their rights and responsibilities when it comes to workers’ compensation.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Before you can save money in your company, you have to understand why you are in business and your objectives. Most people start a business out of necessity or a desire to run their own business in the industry of choice. However, the main objective of any business is to earn money.

Part of your money-saving plan for your company will have to include the evaluationof expenses. Many businesses that get in trouble are due to the owner having difficulty handling expenses properly. And this is a problem since it is critical to earn and save money.

To save money for your company, you need to understand all of your expenses and handle them. Ultimately, saving money in your company is more about money management and controlling costs than it has to do with how much your company generates in income.

While you want to continuously bring revenue into the company, you should be equally focused on saving money and controlling expenses. Many companies have a department dedicated to expenses within the company and recommend ways to save money.

There are different types of expenses within a company. Those costs that are the same month after month, such as a lease, are considered fixed costs because they will be constant and often the same. Fixed costs can include electricity, water, internet, rent, and payroll.

What can you do to save money here in fixed costs? The answer is almost nothing because most of the fixed costs are or commodities that have a low cost and resources on which your business depends and that if they are not well maintained, can affect your operation.

Therefore, you will need to find other ways to save money within these costs.

You can save some money on services, such as water and electricity, if it does not take a long time or affect your service quality and operations. Either way, this will bring small savings for you.

Try to reduce rental income only if your business does not depend on the location, as in restaurants, stores, or personal assistance services.

Try to reduce the total cost of fixed employees. Here, the key is that you learn to differentiate which roles of your company are fundamental for your organization and which can become a variable cost, which you can hire through services to freelancers.

Other operations costs can also be looked at to save the company money. These are the necessary expenses directly associated with the product or service, and that can go up and down according to the production demand, your sales, or projects.

You can save by doing the following.

Get discounts or suppliers that allow you a percentage of savings in raw material.

Change one expensive material for another, as long as it does not affect the quality of the product.

Have better inventory management, decreasing the number of products that can be cold in your stock.

Outsource services such as customer service or for specific activities that are demanded according to sales.

Saving money in your company and how you do it is not the same for every type of company. Some companies will find it more difficult. However, all companies can look at ways to save, such as through opportunity costs.

The opportunity cost is a way of measuring if we are doing what interests us. Measure what we could be doing instead of what we do (opportunities).

For example: if I have a women’s clothing store brand A, I lose the opportunity to sell brand B clothes. If I have my employees in a project, I lose the opportunity to work in another.

This can confuse the cost of execution, but the opportunity cost tells you that you are doing your best with your resources.

In this case, there are no specific tips. The director of the company has some practices to help him make decisions:

Purchasing policy based on turnover based on sales

Make decisions based on market share and product or service potential

Management of human resources, considering the specialization and alternatives of outsourcing

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Often the wedding is the first significant financial strain of a couple starting together. Therefore, when planning a wedding, finances should be considered, and planning should be within the means of the couple and whoever else is springing for the wedding.

With the awareness of the importance of getting off to a good start, here is some excellent advice from Melissa Morales, general manager of Argentarium, inspired by the lessons learned from the planning of her ceremony.

The wedding is only one day. The first and most crucial task is defining the household budget and short-, long- and medium-term goals with your partner. After you get married, you will have many more financial responsibilities. If you plan your household finances before the union occurs, it will be easier to know how much money you can spend on the wedding.

Before planning your wedding, you must make a detailed budget with what you can spend in this event and commit to being rigorous with its compliance. As it is an event that we plan with much emotion, we are often tempted to do the opposite: plan and then look for the money. This would be a mistake with essential effects on the marriage pocket. Remember: first determine how much you can spend and, from there, make plans.

Define priorities. Some things may not be so essential for your wedding. Do you need an orchestra or stage that acts as a dance floor? It is convenient to define, from the beginning, which things are so vital that they are not negotiable and then several levels of priority so that it is easier to make cuts in case the quotations exceed the budget.

Do not pond with the opinion of a single supplier. Look for several opinions and compare until you find what best fits your budget. Some experts recommend analyzing between three and six quotes, at least in the most expensive services.

Selecting services well in advance will help you find a better price. In addition, in some cases, you have the option of paying in installments as the wedding approaches, or you get discounts for paying in advance.

Eye with this. Never think about financing your wedding! If you do not have enough money to make an expensive event, you can choose to do something familiar and straightforward and postpone the celebration “in style” or be open to more guests.

If you buy something or hire a service, it must be because you want it, and you need it. During the planning, many will think and tell you that this or that thing is a good option, that it is at a reasonable price, that it was incredibly good at the wedding of The Mangano’s. Avoid falling into the temptation of incorporating elements that, initially, you were not interested in including in your link ceremony.

Look for the opinions of friends who have already been married. They are great experts, especially if they have recently remarried. Take into account the initial budgets they had better if they are like yours. They will guide you on almost everything you need.

Be careful with the guest list. This is one of the most challenging parts of organizing a wedding. On the one hand, you have a limited budget and, on the other hand, many people that you would like to invite to the celebration or with which you feel committed.

In this case, it also turns out to establish categories: first the guests and essential guests that you want to be present at your wedding; then, those with whom you and your partner feel that they must “look good” and, finally, those with whom your parents, uncles, brothers, brothers-in-law, and cousins think that you must “look good.” It will never be easy to cut out invitations, but at least you will know where to start.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

The process of buying a car involves a few crucial steps. But some critical steps must be completed pre-purchase. The steps that one needs to complete before the purchase include the following:

Analysis of the financial situation

The setting of a budget

Listing down of required specifications

Payment Methods

These are the four most essential steps that must be completed before a car is purchased. All these contribute to making the process of buying a car simple and stress-free. Analysis of the financial situation helps in deciding the amount that a buyer can spare for the car. Having a strict budget and listen to requirements provides the buyer with an upper hand in the price negotiations with the car dealer.

After all, this has been done, the most significant decision has to be made, the payment method. Selecting the method of payment varies with the type of car one wishes to purchase. Here are three ways to pay when buying a car and their advantages and disadvantages.

Paying Cash

Out of the three payment methods for buying a car, paying through cash is the most straightforward one. To make it simple to understand, it is just like buying shoes or a burger. A customer pays and gets the item without any stress or difficulties.

Advantages

The main advantage is that people save themselves from monthly payments through this method, freeing themselves from the liabilities attached. It does not affect their monthly responsibilities, and their lives stay balanced.

Secondly, they have to pay the exact amount, free of any interest. The addition of interests reduces the chances of reselling the car in profit. In addition to this, the reselling of the car becomes more accessible and more straightforward. The chances of earning profits are higher in this case.

Disadvantages

There are downsides to everything and even paying for a car directly with cash has its disadvantages. Cars are not cheap. A person needs to work tirelessly for a long time to gather such a vast amount. Paying fully in cash takes a massive chunk of money from the savings, exposing an individual to the stress of emergencies.

A car’s value depreciates every year, and it is not a good investment option. After four years, the price of a car drops to half of its original price, which comes as a massive blow to the car owners at the time of resale.

Financing

The most common payment method in car purchases in America is getting the car financed by a third party. An external party, i.e., banks, financial companies, and credit unions, pays off the car dealer. It is a feasible method for many. Due to this payment method, a lot of middle-class Americans have been able to get a car.

Advantages

There are some fantastic benefits of getting a car financed. As a buyer uses someone else’s money to pay the car dealer, the financial balance is not significantly affected. It helps in maintaining the lifestyle as only monthly payments have to be made.

Cutting out only a few expenses helps people pay off their monthly payments. Once the payments have been successfully paid, the buyer becomes the owner of the car. People who have a good credit score can enjoy loans with lower interest rates. It gets easier for them to get loans on acceptable terms.

Disadvantages

Besides great benefits, there are some non-negligible disadvantages of getting a car financed. The very first drawback of this payment method is the interest rates. With financing plans, a buyer is liable for monthly payments and ends up paying way more than a car costs.

It is true that after ultimately paying off the loan, a buyer becomes its owner. But by the time these payments are completed, the car’s value drops to 50% of its original value. When it comes to reselling the car, there are negligible chances of earning any profits. Things are worse for people with a bad credit score. They are unable to get feasible financial plans. Either they end up paying high-interest rates, or the payments are too large.

Leasing

The last payment option is the leasing of the car. It is a highly unpopular payment method in the United States. Its unpopularity is because a person cannot buy a car; instead, they are forced to rent it.

It is somewhat similar to financing as it also requires payment of a down payment followed by fixed monthly payments. Unlike financing, after the payments are completed, the buyer must return the car to the dealer or replace it.

An individual is not asked to pay the whole loan instead of only the depreciated value. This means that if a lease is five years and the cost of the car after five years equals 40% of the original cost, the buyer will have to cover only 60% of the original price.

Advantages

In getting a car on a lease, a buyer does not have to pay the whole loan but only the depreciated value. It makes this method one of the most affordable options. Also, the amount of monthly payments is much lower than in the case of a financed car. When the payments are completed, an individual does not have to stress about selling it off. They can return it to the dealer or get it replaced.

Disadvantages

As compared to other payment options, leasing a car is attached to the minor disadvantages. The permitted period to keep a car by a lender is not more than three years, which forces an individual to change their rides. A significant downside to getting a car on a lease is that the annual mileage is limited, restricting a driver’s driving habits. If a driver goes over the limit, a high cost is imposed on them.

Making the Right Choice

The payment option depends entirely upon a car buyer’s budget, financial situation, and preferences. Not any people can afford to pay with cash as it will eat a significant portion of the total savings, making the financial situation unstable. But it depends on the buying capacity and the mindset of the buyer.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

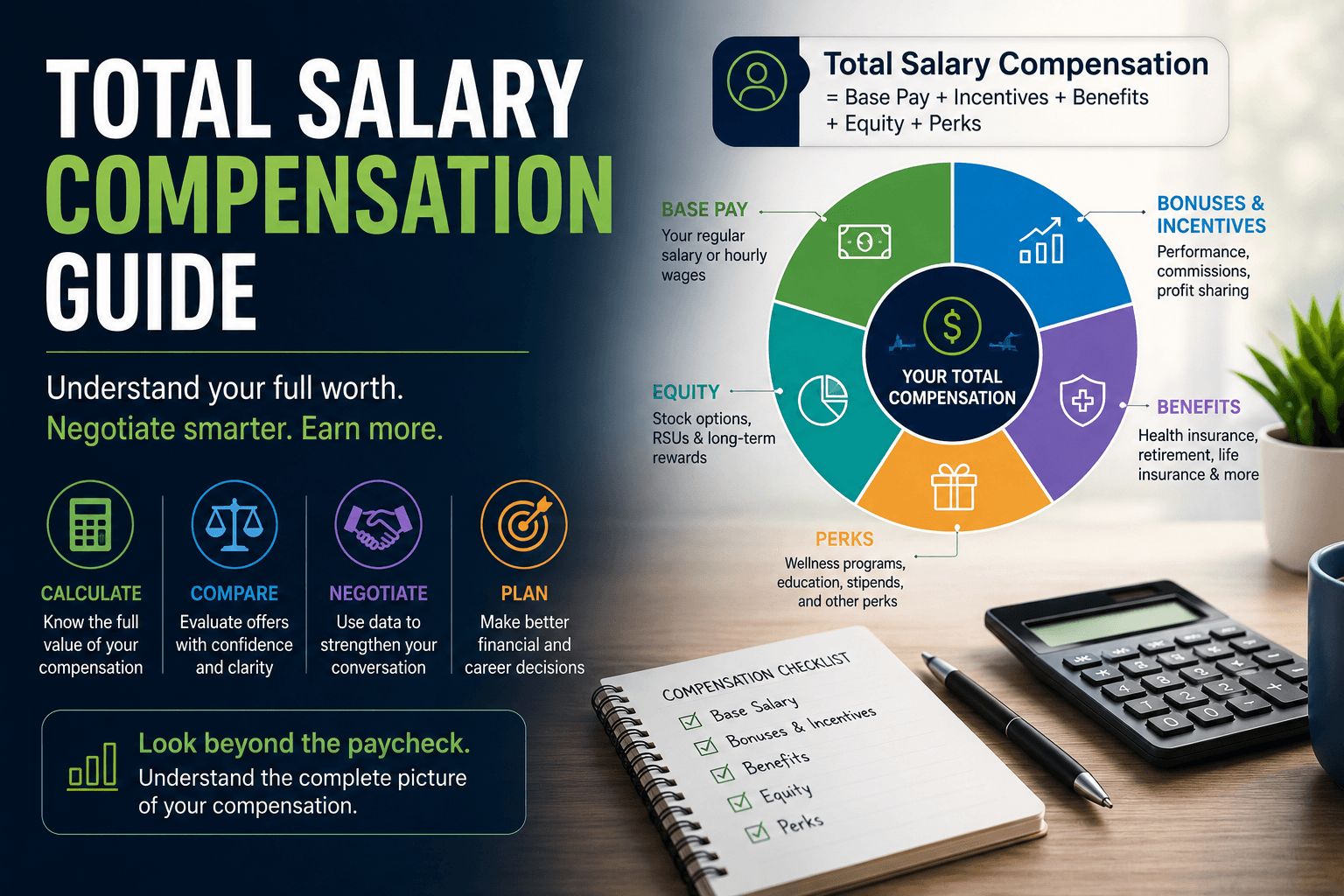

Total Salary Compensation: What It Is & How It Works

Total salary compensation is the full dollar value of everything you earn for your work your base salary plus bonuses, incentives, employer-paid benefits, equity, and perks—rolled into one annual number so you can compare offers and current pay fairly, not just by the headline salary figure.

Over two decades leading Complete Controller, I’ve watched sharp business owners and talented employees leave thousands of dollars on the table because they only looked at base pay. Once we sat down and mapped their total compensation and benefits line by line—healthcare premiums, retirement matches, PTO, equity, even training budgets—the real picture often shifted dramatically. From advising small business clients across nearly every industry to building my own remote team, I’ve seen firsthand how clarity around payroll compensation transforms hiring, retention, and trust. In this article, I’ll walk you through what total salary compensation includes, how to calculate it, how to use it for fair comparisons, and how to design compensation packages that actually work.

Compensation should feel clear, not confusing. Complete Controller helps businesses build smarter payroll systems, cleaner reporting, and compensation visibility employees actually trust.

What is total salary compensation and how do you get it right?

Total salary compensation is the sum of your base pay, variable incentives, employer-paid benefits, equity, and perks, expressed as an annual dollar amount for apples-to-apples comparisons.

It includes direct pay (salary, overtime, bonuses, commissions) and indirect rewards (insurance, retirement contributions, paid time off, wellness programs).

Understanding it helps you evaluate whether your pay is competitive, supports pay equity, and matches your goals.

A clear total salary compensation calculation gives employers a transparency tool and gives employees real negotiation leverage.

Reviewing it regularly against salary benchmarks keeps your compensation analysis grounded in current market data.

What Total Salary Compensation Really Means (Beyond Your Paycheck)

Your paycheck tells one small part of a much bigger story. The salary structure of a company defines how pay ranges, bands, and progression work for each role—but total salary compensation captures everything that role is actually worth in a year.

From the employer side, HR and finance teams design a compensation package to attract and keep great people. From the employee side, the gap between base salary and full compensation and benefits is often 25–40% of the headline number. That’s not a rounding error—it’s real money.

Components of a modern compensation package

Here’s what typically makes up the full picture:

Direct compensation: base salary, hourly wages, overtime, bonuses, commissions, profit sharing

Indirect compensation: health/dental/vision insurance, retirement plans with employer match, paid time off, life and disability insurance

Perks and total rewards: wellness programs, education assistance, remote work stipends, commuter benefits, professional development budgets

The salary vs compensation comparison matters because most people anchor emotionally to the base number and undervalue benefits—a habit that quietly costs them at every job change.

How to Calculate Total Salary Compensation Step-by-Step

Here’s the formula I use with clients and walk new hires through:

Total Salary Compensation = Base Pay + Variable Incentives + Employer-Paid Benefits + Equity Value + Perks (annualized)

Most modern benefits administration platforms store every data point you need. You’re just pulling it into one place.

Quantify base pay and your incentive compensation plan

Start with your annual salary or hourly rate multiplied by expected hours. Then layer in target bonuses (typically a percentage of salary), commissions, and any profit-sharing payouts. For executive compensation, factor in deferred bonuses and long-term incentive plans on an annualized basis.

Put a dollar value on employee benefits

This is where most people stop short. Pull the employer cost for your health, dental, and vision premiums, your 401(k) match, and life or disability insurance. Then annualize your PTO: divide your salary by workdays per year, then multiply by your PTO days.

According to the U.S. Bureau of Labor Statistics, U.S. private employers spent an average of $2.96 per hour worked on paid leave alone in March 2024. PTO isn’t fluffy—it’s a measurable line item.

Include equity and long-term rewards

When valuing stock options or RSUs, use the current share price and the vesting schedule, but apply a conservative discount. I’ve seen too many employees count unvested equity at peak valuation and get burned. Treat it as upside, not guaranteed income.

Total salary compensation calculation example

Imagine an $80,000 base, a $6,000 target bonus, $9,000 in employer-paid health premiums, a $4,000 401(k) match, $4,000 in annualized PTO, and $2,000 in perks. Your annual total compensation is $105,000—a 31% jump from base.

Using Total Salary Compensation to Compare Offers Fairly

When you’re weighing two offers, always convert both to annual total compensation. Different PTO levels, bonus payout probabilities, and benefit costs can swing the real value by tens of thousands.

Compensation analysis tools and salary benchmarks

Use salary benchmarks from trusted sources like Indeed, Levels.fyi, BLS data, and industry surveys. Adjust for geography and remote work realities. Compare market median base pay to yours, then market median total compensation to yours. The gap tells you exactly where to push.

Pay equity and pay transparency laws

Pay equity means equal pay for substantially similar work—and it must account for full compensation and benefits, not just salary. With pay transparency laws now requiring range posting in many states, you have more sanity-check data than ever. Use it.

Negotiation strategies grounded in total compensation

When base pay is capped, the smart move is negotiating PTO, remote flexibility, signing bonuses, education funding, or relocation. As an employer, I can tell you there’s almost always more give in benefits and perks than in base salary.

How Employers Design Total Salary Compensation That Actually Works

Strong salary structure starts with job families, pay bands, and clear ranges (min-mid-max). Tie your incentive compensation plan to business outcomes you actually want to drive. For small and mid-sized businesses, the risk is informality—without intentional design, inconsistency and inequity creep in fast.

Cost breakdown: Wages vs. benefits in total rewards

For U.S. private industry workers, employers spent an average of $43.03 per hour worked on total compensation in March 2024. Of that, $30.42 was wages and $12.61 was benefits—about 29% of total compensation (U.S. Bureau of Labor Statistics). That roughly 70/30 split is the baseline every SMB owner should know.

The role of benefits administration and payroll systems

Cloud-based payroll and benefits administration tools make it possible to calculate, audit, and communicate total compensation accurately. At Complete Controller, we build these systems for clients so that owners can show employees the real value of their package—and employees can see it clearly.

Case Study: Salesforce and Total Compensation Transparency

Salesforce publicly committed to closing its gender pay gap and spent $3 million after its first review of compensation for employees doing similar work. The company framed it as ongoing—spending millions more in later reviews to maintain pay equity (Fortune).

What changed? Leadership conducted compensation benchmarking, ran a pay equity analysis, and built personalized total compensation statements. Managers were trained to discuss total compensation and benefits during reviews. The results: higher employee understanding, improved retention, and stronger trust.

Lessons for small and mid-sized businesses

You don’t need Salesforce’s budget to do this. A simple spreadsheet, an annual review cycle, and a one-page total compensation statement per employee will get you 80% of the value. I’ve implemented this for my own team and for client companies through our bookkeeping and accounting services, and the trust dividend is real.

A Simple Roadmap for Employees and Business Owners

5 Steps Employees Can Take This Week:

Inventory every piece of your compensation using pay stubs and your benefits portal.

Estimate annual values for each benefit, including PTO.

Compare your annual total compensation to salary benchmarks for your role and city.

Identify gaps—is your base low but benefits generous, or the reverse?

Plan your next conversation with a specific ask.

5 Steps Business Owners Can Take This Quarter:

Map your current compensation package for each role.

Run compensation benchmarking against industry and region.

Check for pay equity within similar roles.

Create total compensation statements—even basic ones.

Set a recurring compensation analysis cycle tied to performance reviews.

Conclusion: Turning Total Salary Compensation Into a Fairness Tool

Total salary compensation is base pay plus incentives, benefits, equity, and perks—and understanding it is essential for fair comparisons, smart negotiations, and real pay equity. Both sides of the table need structured compensation analysis and honest communication.

In my years at Complete Controller, I’ve watched the conversation around pay completely transform when people see the full picture. Trust goes up, turnover goes down, and employees become advocates instead of skeptics. Whether you’re an employee evaluating an offer or an owner building a team, the math is worth doing—and the conversation is worth having. If you want help building compensation structures, payroll systems, and financial reporting that make total salary compensation clear, accurate, and fair, the team at Complete Controller is ready when you are.

Frequently Asked Questions About Total Salary Compensation

What is total salary compensation?

Total salary compensation is the full annual dollar value of your pay package—base salary plus bonuses, incentives, employer-paid benefits, equity, and perks combined.

How is total compensation different from base salary?

Base salary is only your headline pay before any bonuses or benefits. Total compensation adds the dollar value of insurance, retirement matches, PTO, equity, and perks—often 25–40% more than base.

What is included in a total compensation package?

Direct pay (salary, overtime, bonuses, commissions), indirect benefits (health insurance, retirement contributions, PTO, disability/life insurance), equity, and perks like wellness stipends or education assistance.

How do I calculate my total compensation from a job offer?

Add base pay, target bonus, annualized PTO value, employer-paid benefit costs, retirement match, and any equity or perks. The sum is your annual total compensation.

Is a lower salary with better benefits ever a better total compensation deal?

Yes. A role with lower base but generous health coverage, strong retirement match, and ample PTO can easily out-earn a higher salary with weaker benefits once you run the full calculation.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

The fundamental things you heft around in your tote frequently incorporate things that set you up for crises, similar to tampons, tissues, and over-the-counter prescriptions. Even though it’s critical to be readied, keeping certain things in your tote can set you up for destruction for the situation that your suitcase is lost or taken. On the off chance that the things in your suitcase have any nostalgic worth joined, similar to family photographs or adornments, or could have costly results whenever lost, at that point, you ought to abstain from conveying them in your tote.

As an ever-increasing number of sites and applications require passwords for security purposes, it very well maybe not be easy to monitor that data yet, it would help if you abstained from keeping this touchy data recorded on a sheet in your tote.

Regardless of gender, we always carry a compartment (bag or purse) to carry the important. We will talk about objects that have to do with finances or useful life. Each person is a world and is organized differently so that the things they carry are also. However, they usually coincide in some, such as credit cards, money, etc.

You ought to routinely convey the main distinguishing record with you is a driver’s permit or state ID card. You ought not to make a propensity out of conveying your government-backed retirement card, visa, or birth declaration with you except if you need it for voyaging. Besides the issue of supplanting these things, they’re a significant wellspring of data fraud.

The important thing is not to carry things that may represent a danger or a big problem in the future due to loss or loss. All of it is related to the importance of these goods.

What you should avoid loading in your wallet or purse

To guide you on the important things you should avoid having all the time with you, we share a list.

Credit and debit cards

Unless you plan to use any of the two cards, it is recommended that you do not load them. You can always run the risk of losing them or having them stolen. Although it is easy to protect them in banking institutions, it is not necessary to go through that. On the other hand, thinking more positively, bringing credit cards with you is a synonym for spending more if you don’t have self-control.

Storage devices

It depends on the type of information your device has. If you have sensitive information, the ideal is not to bring it with you all the time. Imagine that anyone could have access to documents with very personal information? It could be a victim of identity theft or extortion.

Unnecessary cash

The same thing happens with credit cards; you will be more likely to spend out of your budget. If you do not use that money, leave it at home or the cashier.

Important access passwords

It may seem dated, but many people still keep their passwords in small notebooks or papers. Either because they don’t have a good memory or because they are used to using a pencil and paper.

You should have passwords with easy-to-remember numbers, in theory, so you don’t need to write them down on paper or on your phone. However, it would help if you also tried not to be very predictable and not use numbers to do with birthdays.

Invoices or receipts

Most of us forget to tidy up that part, so we just put the bag or purse without paying attention. Many people have these receipts or bills so old that the information is no longer perceived.

Although it may seem somewhat helpless and common, it is possible to share sensitive information without realizing it with this type of activity. It is easy to notice your shopping habits or personal data with only these receipts or invoices. Be more cautious and set aside a place for these types of documents; if you are not going to use them, destroy them.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Mastering Transportation and Logistics: Essential Insights

Transportation and logistics encompasses the strategic planning, movement, and management of goods, inventory, and information from origin to delivery to maximize efficiency, reliability, and cost-effectiveness. This integrated system includes warehousing, distribution, freight transportation across multiple modes, supply chain optimization, and last-mile delivery services that connect businesses to customers worldwide.

Leading companies are transforming their logistics operations through data-driven strategies and automation technologies. Over my 20 years as CEO of Complete Controller, I’ve witnessed businesses across all sectors struggle with rising freight costs, delivery delays, and inventory management challenges. This article reveals proven strategies for optimizing your logistics operations, including scenario-based planning techniques that reduced costs by 12% for major carriers, automation solutions cutting warehouse expenses by 30%, and sustainable practices that both lower emissions and improve profitability. You’ll gain actionable frameworks for selecting transportation modes, managing inventory systems, and building resilient supply chains that adapt to market volatility.

What is transportation and logistics, and how do you master it?

Transportation and logistics refers to the coordinated planning, movement, and management of goods and resources across supply chains to achieve on-time, cost-effective delivery

Planning encompasses demand forecasting, route optimization, and resource allocation across the supply network

Movement includes selecting optimal transportation modes—trucking, rail, air, or waterway—based on speed, cost, and volume requirements

Management involves real-time tracking, inventory control, and performance monitoring to maintain service levels

Mastery requires integrating technology platforms, building strong carrier partnerships, and implementing continuous improvement processes

The Core Components of Modern Transportation and Logistics

The global logistics market reached $11.26 trillion in 2024 and continues expanding at 6.3% annually, driven by e-commerce growth and increasing supply chain complexity. This growth reflects fundamental shifts in how businesses manage inventory, fulfill orders, and meet rising customer expectations for speed and transparency.

Building strong logistics management foundations

Effective logistics management starts with robust inventory control and demand forecasting systems. Cloud-based inventory platforms provide real-time visibility across multiple warehouse locations, enabling businesses to maintain optimal stock levels while minimizing carrying costs. Smart warehouse management systems track every item from receipt through shipment, reducing errors and accelerating fulfillment times.

Distribution network design represents another critical foundation element. Strategic warehouse placement reduces transportation distances and delivery times while balancing inventory investment requirements. Leading companies utilize network modeling software to evaluate different facility configurations, analyzing factors including customer density, transportation costs, and service level requirements. These models help identify optimal locations for distribution centers that minimize total logistics costs while meeting delivery commitments.

Optimizing transportation mode selection

Transportation mode selection significantly impacts both costs and service levels. Road freight dominates domestic logistics, handling 72.6% of U.S. freight tonnage through flexible door-to-door service. However, each mode offers distinct advantages for specific shipping requirements:

Trucking: Provides maximum flexibility and speed for regional distribution, though facing 25% cost increases due to driver shortages

Rail transport: Delivers 4.1% annual growth through superior fuel efficiency for bulk commodities on established corridors

Waterway shipping: Achieves lowest per-ton costs for high-volume international trade, growing at 6.2% annually

Air freight: Offers fastest transit times for time-sensitive, high-value shipments despite premium pricing

Strategic mode selection requires analyzing shipment characteristics including weight, volume, value, urgency, and destination accessibility. Many companies adopt multi-modal strategies, combining rail for long-distance transport with trucking for final delivery to optimize both cost and service.

Leveraging Technology for Competitive Advantage

Technology transformation drives efficiency gains across transportation and logistics operations. Artificial intelligence and machine learning applications revolutionize route planning, demand forecasting, and capacity utilization.

Real-time visibility and tracking systems

Modern transportation management systems provide end-to-end shipment visibility through GPS tracking, IoT sensors, and integrated carrier data feeds. These platforms consolidate information from multiple sources into unified dashboards showing real-time location, estimated arrival times, and exception alerts. Advanced systems predict potential delays based on traffic patterns, weather conditions, and historical performance data.

Integration capabilities connect transportation systems with warehouse management, order processing, and customer communication platforms. Automated notifications keep customers informed about delivery status while exception management tools alert operations teams to potential service failures before they impact customers. This proactive approach reduces customer service inquiries while improving on-time delivery performance.

Automation and robotics applications

Warehouse automation technologies deliver substantial productivity improvements while addressing labor availability challenges. Automated storage and retrieval systems reduce picking times by 60% while improving accuracy to 99.9%. Robotic systems handle repetitive tasks including palletizing, sorting, and packaging, freeing human workers for higher-value activities.

Autonomous vehicle pilots demonstrate potential for transforming last-mile delivery economics. Major logistics providers test self-driving trucks for highway transport and delivery robots for residential service. While regulatory approval remains pending for widespread deployment, these technologies promise significant cost reductions and service improvements once operational barriers clear.

Implementing Sustainable Logistics Strategies

Environmental sustainability has evolved from optional initiative to competitive requirement as customers demand carbon footprint transparency and regulators impose emissions standards. Sustainable practices often improve profitability through reduced fuel consumption and operational efficiency.

Route optimization and load consolidation

Advanced routing algorithms minimize total miles driven while maintaining service commitments. Dynamic route optimization considers real-time traffic conditions, delivery windows, and vehicle capacity to reduce fuel consumption by 15-20%. Load consolidation strategies combine multiple shipments into fuller trucks, improving asset utilization while reducing per-package emissions.

Fleet modernization provides another sustainability lever. Electric vehicles suit urban delivery routes with predictable daily mileage and overnight charging availability. Alternative fuel vehicles including compressed natural gas and hydrogen show promise for longer routes. Leading carriers commit to electrifying delivery fleets by 2030, driven by both environmental goals and anticipated operating cost advantages.

Circular economy and reverse logistics

Reverse logistics capabilities become increasingly important as e-commerce return rates reach 20-30% for certain categories. Efficient returns processing recovers value from returned products while minimizing environmental impact through proper recycling and disposal. Streamlined reverse logistics networks reduce transportation requirements by consolidating return shipments and processing returns at regional facilities rather than shipping back to origin.

Packaging optimization represents another sustainability opportunity. Right-sized packaging reduces material usage and improves truck capacity utilization. Reusable packaging systems eliminate waste for regular shipment routes between facilities. These initiatives reduce costs while demonstrating environmental commitment to sustainability-conscious customers.

Navigating Market Volatility and Building Resilience

Recent years demonstrated supply chain vulnerability to disruptions including pandemics, natural disasters, and geopolitical conflicts. Building resilient logistics operations requires strategic planning and operational flexibility.

Scenario planning and risk management

Leading companies employ scenario-based planning to prepare for potential disruptions. DHL’s implementation of advanced scenario-planning tools evaluated impacts from fuel price volatility, labor shortages, and modal capacity constraints. By modeling various disruption scenarios, they identified vulnerabilities and developed contingency plans that reduced costs by 12% while improving service reliability during actual disruptions.

Diversification strategies reduce dependency on single suppliers, routes, or transportation modes. Multi-sourcing critical components, maintaining relationships with multiple carriers, and developing alternative routing options provide flexibility when primary channels face constraints. Investment in visibility systems enables rapid response when disruptions occur, allowing redirection of shipments and customer communication about revised delivery expectations.

Labor challenges and workforce development

The logistics industry faces severe labor shortages, particularly for truck drivers where demand exceeds supply by 80,000 positions in the United States alone. These shortages drive wage inflation and capacity constraints that impact service availability and costs. Companies respond through multiple strategies:

Technology adoption: Automated systems reduce labor requirements for routine tasks

Improved working conditions: Better scheduling, modern equipment, and competitive benefits attract and retain workers

Training programs: Partnerships with educational institutions develop skilled logistics professionals

Process redesign: Simplified workflows reduce training requirements and improve productivity

Practical Implementation: Your 90-Day Action Plan

Transforming transportation and logistics operations requires systematic approach and sustained execution. This roadmap provides structured path for improvement regardless of company size or current maturity level.

Days 1-30: Assessment and baseline establishment

Begin with comprehensive logistics audit documenting current performance across key metrics including on-time delivery, transportation costs, inventory accuracy, and order cycle times. Map existing processes identifying bottlenecks, redundancies, and improvement opportunities. Survey customers about delivery expectations and pain points. Benchmark performance against industry standards to establish improvement targets.

Days 31-60: Technology selection and process redesign

Evaluate technology platforms for transportation management, warehouse operations, and customer visibility. Prioritize systems providing quick wins through basic automation and visibility improvements. Redesign core processes eliminating identified inefficiencies. Implement pilot programs testing new approaches with limited scope before broader rollout. Train staff on new systems and processes, addressing change management proactively.

Days 61-90: Optimization and continuous improvement

Launch optimization initiatives for routing, load planning, and inventory placement based on collected data. Establish partnerships with technology providers and logistics specialists filling capability gaps. Implement performance dashboards tracking key metrics in real-time. Create feedback loops incorporating customer and employee input into ongoing improvements. Document standard operating procedures sustaining gains achieved.

Final Thoughts

Transportation and logistics excellence demands continuous adaptation to changing market conditions, technology capabilities, and customer expectations. Success requires balancing strategic vision with operational excellence, investing in both technology and people while maintaining focus on sustainable profitability.