Total Salary Compensation:

What It Is & How It Works

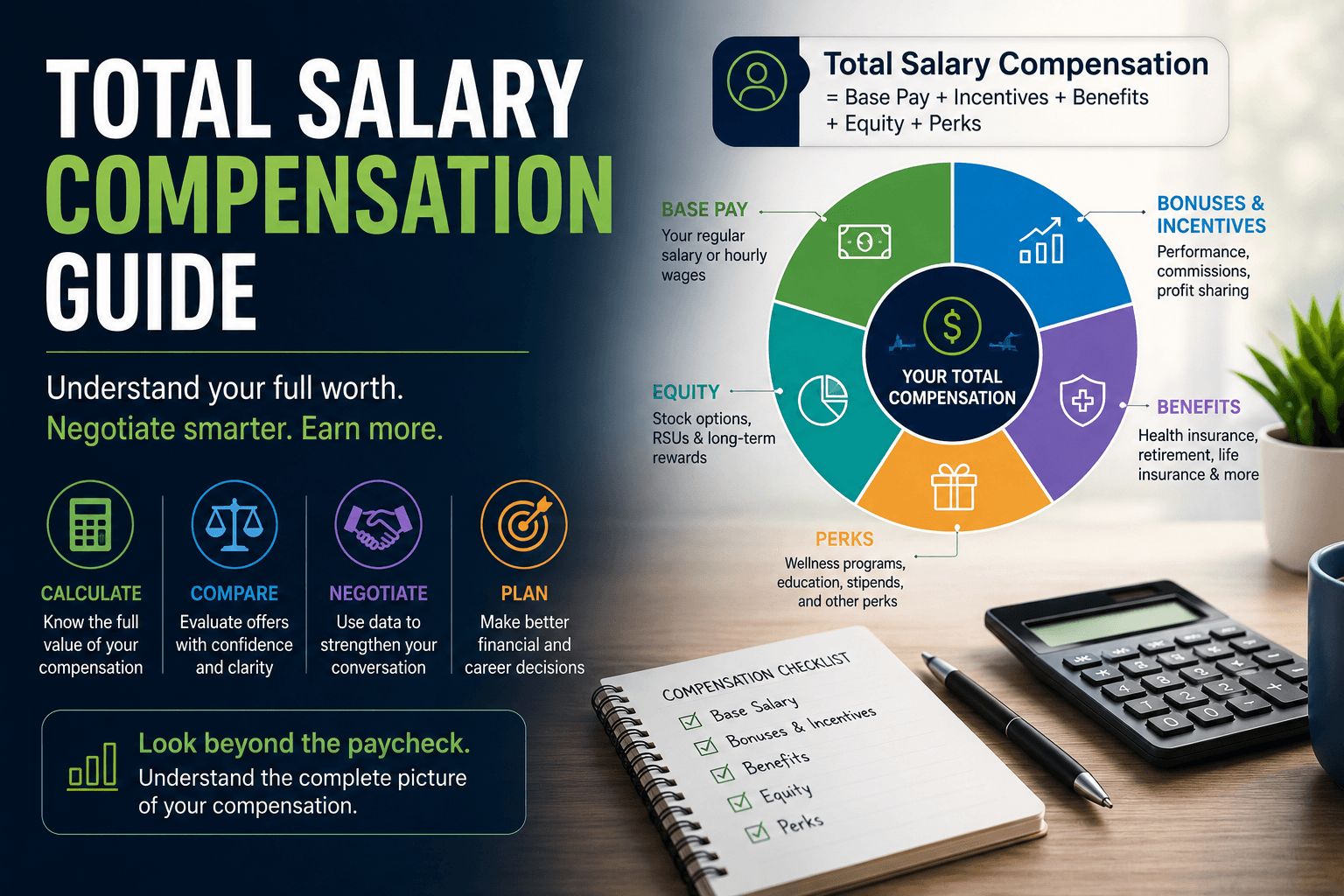

Total salary compensation is the full dollar value of everything you earn for your work your base salary plus bonuses, incentives, employer-paid benefits, equity, and perks—rolled into one annual number so you can compare offers and current pay fairly, not just by the headline salary figure.

Over two decades leading Complete Controller, I’ve watched sharp business owners and talented employees leave thousands of dollars on the table because they only looked at base pay. Once we sat down and mapped their total compensation and benefits line by line—healthcare premiums, retirement matches, PTO, equity, even training budgets—the real picture often shifted dramatically. From advising small business clients across nearly every industry to building my own remote team, I’ve seen firsthand how clarity around payroll compensation transforms hiring, retention, and trust. In this article, I’ll walk you through what total salary compensation includes, how to calculate it, how to use it for fair comparisons, and how to design compensation packages that actually work.

Compensation should feel clear, not confusing. Complete Controller helps businesses build smarter payroll systems, cleaner reporting, and compensation visibility employees actually trust.

What is total salary compensation and how do you get it right?

- Total salary compensation is the sum of your base pay, variable incentives, employer-paid benefits, equity, and perks, expressed as an annual dollar amount for apples-to-apples comparisons.

- It includes direct pay (salary, overtime, bonuses, commissions) and indirect rewards (insurance, retirement contributions, paid time off, wellness programs).

- Understanding it helps you evaluate whether your pay is competitive, supports pay equity, and matches your goals.

- A clear total salary compensation calculation gives employers a transparency tool and gives employees real negotiation leverage.

- Reviewing it regularly against salary benchmarks keeps your compensation analysis grounded in current market data.

What Total Salary Compensation Really Means (Beyond Your Paycheck)

Your paycheck tells one small part of a much bigger story. The salary structure of a company defines how pay ranges, bands, and progression work for each role—but total salary compensation captures everything that role is actually worth in a year.

From the employer side, HR and finance teams design a compensation package to attract and keep great people. From the employee side, the gap between base salary and full compensation and benefits is often 25–40% of the headline number. That’s not a rounding error—it’s real money.

Components of a modern compensation package

Here’s what typically makes up the full picture:

- Direct compensation: base salary, hourly wages, overtime, bonuses, commissions, profit sharing

- Indirect compensation: health/dental/vision insurance, retirement plans with employer match, paid time off, life and disability insurance

- Perks and total rewards: wellness programs, education assistance, remote work stipends, commuter benefits, professional development budgets

The salary vs compensation comparison matters because most people anchor emotionally to the base number and undervalue benefits—a habit that quietly costs them at every job change.

How to Calculate Total Salary Compensation Step-by-Step

Here’s the formula I use with clients and walk new hires through:

Total Salary Compensation = Base Pay + Variable Incentives + Employer-Paid Benefits + Equity Value + Perks (annualized)

Most modern benefits administration platforms store every data point you need. You’re just pulling it into one place.

Quantify base pay and your incentive compensation plan

Start with your annual salary or hourly rate multiplied by expected hours. Then layer in target bonuses (typically a percentage of salary), commissions, and any profit-sharing payouts. For executive compensation, factor in deferred bonuses and long-term incentive plans on an annualized basis.

Put a dollar value on employee benefits

This is where most people stop short. Pull the employer cost for your health, dental, and vision premiums, your 401(k) match, and life or disability insurance. Then annualize your PTO: divide your salary by workdays per year, then multiply by your PTO days.

According to the U.S. Bureau of Labor Statistics, U.S. private employers spent an average of $2.96 per hour worked on paid leave alone in March 2024. PTO isn’t fluffy—it’s a measurable line item.

Include equity and long-term rewards

When valuing stock options or RSUs, use the current share price and the vesting schedule, but apply a conservative discount. I’ve seen too many employees count unvested equity at peak valuation and get burned. Treat it as upside, not guaranteed income.

Total salary compensation calculation example

Imagine an $80,000 base, a $6,000 target bonus, $9,000 in employer-paid health premiums, a $4,000 401(k) match, $4,000 in annualized PTO, and $2,000 in perks. Your annual total compensation is $105,000—a 31% jump from base.

Using Total Salary Compensation to Compare Offers Fairly

When you’re weighing two offers, always convert both to annual total compensation. Different PTO levels, bonus payout probabilities, and benefit costs can swing the real value by tens of thousands.

Compensation analysis tools and salary benchmarks

Use salary benchmarks from trusted sources like Indeed, Levels.fyi, BLS data, and industry surveys. Adjust for geography and remote work realities. Compare market median base pay to yours, then market median total compensation to yours. The gap tells you exactly where to push.

Pay equity and pay transparency laws

Pay equity means equal pay for substantially similar work—and it must account for full compensation and benefits, not just salary. With pay transparency laws now requiring range posting in many states, you have more sanity-check data than ever. Use it.

Negotiation strategies grounded in total compensation

When base pay is capped, the smart move is negotiating PTO, remote flexibility, signing bonuses, education funding, or relocation. As an employer, I can tell you there’s almost always more give in benefits and perks than in base salary.

How Employers Design Total Salary Compensation That Actually Works

Strong salary structure starts with job families, pay bands, and clear ranges (min-mid-max). Tie your incentive compensation plan to business outcomes you actually want to drive. For small and mid-sized businesses, the risk is informality—without intentional design, inconsistency and inequity creep in fast.

Cost breakdown: Wages vs. benefits in total rewards

For U.S. private industry workers, employers spent an average of $43.03 per hour worked on total compensation in March 2024. Of that, $30.42 was wages and $12.61 was benefits—about 29% of total compensation (U.S. Bureau of Labor Statistics). That roughly 70/30 split is the baseline every SMB owner should know.

The role of benefits administration and payroll systems

Cloud-based payroll and benefits administration tools make it possible to calculate, audit, and communicate total compensation accurately. At Complete Controller, we build these systems for clients so that owners can show employees the real value of their package—and employees can see it clearly.

Case Study: Salesforce and Total Compensation Transparency

Salesforce publicly committed to closing its gender pay gap and spent $3 million after its first review of compensation for employees doing similar work. The company framed it as ongoing—spending millions more in later reviews to maintain pay equity (Fortune).

What changed? Leadership conducted compensation benchmarking, ran a pay equity analysis, and built personalized total compensation statements. Managers were trained to discuss total compensation and benefits during reviews. The results: higher employee understanding, improved retention, and stronger trust.

Lessons for small and mid-sized businesses

You don’t need Salesforce’s budget to do this. A simple spreadsheet, an annual review cycle, and a one-page total compensation statement per employee will get you 80% of the value. I’ve implemented this for my own team and for client companies through our bookkeeping and accounting services, and the trust dividend is real.

A Simple Roadmap for Employees and Business Owners

5 Steps Employees Can Take This Week:

- Inventory every piece of your compensation using pay stubs and your benefits portal.

- Estimate annual values for each benefit, including PTO.

- Compare your annual total compensation to salary benchmarks for your role and city.

- Identify gaps—is your base low but benefits generous, or the reverse?

- Plan your next conversation with a specific ask.

5 Steps Business Owners Can Take This Quarter:

- Map your current compensation package for each role.

- Run compensation benchmarking against industry and region.

- Check for pay equity within similar roles.

- Create total compensation statements—even basic ones.

- Set a recurring compensation analysis cycle tied to performance reviews.

Conclusion: Turning Total Salary Compensation Into a Fairness Tool

Total salary compensation is base pay plus incentives, benefits, equity, and perks—and understanding it is essential for fair comparisons, smart negotiations, and real pay equity. Both sides of the table need structured compensation analysis and honest communication.

In my years at Complete Controller, I’ve watched the conversation around pay completely transform when people see the full picture. Trust goes up, turnover goes down, and employees become advocates instead of skeptics. Whether you’re an employee evaluating an offer or an owner building a team, the math is worth doing—and the conversation is worth having. If you want help building compensation structures, payroll systems, and financial reporting that make total salary compensation clear, accurate, and fair, the team at Complete Controller is ready when you are.

Frequently Asked Questions About Total Salary Compensation

What is total salary compensation?

Total salary compensation is the full annual dollar value of your pay package—base salary plus bonuses, incentives, employer-paid benefits, equity, and perks combined.

How is total compensation different from base salary?

Base salary is only your headline pay before any bonuses or benefits. Total compensation adds the dollar value of insurance, retirement matches, PTO, equity, and perks—often 25–40% more than base.

What is included in a total compensation package?

Direct pay (salary, overtime, bonuses, commissions), indirect benefits (health insurance, retirement contributions, PTO, disability/life insurance), equity, and perks like wellness stipends or education assistance.

How do I calculate my total compensation from a job offer?

Add base pay, target bonus, annualized PTO value, employer-paid benefit costs, retirement match, and any equity or perks. The sum is your annual total compensation.

Is a lower salary with better benefits ever a better total compensation deal?

Yes. A role with lower base but generous health coverage, strong retirement match, and ample PTO can easily out-earn a higher salary with weaker benefits once you run the full calculation.

Sources

- Paychex. “How To Calculate Total Compensation for Employees.” www.paychex.com/articles/human-resources/total-compensation-calculator

- AIHR. “Total Compensation: Definition & How To Calculate It.” www.aihr.com/hr-glossary/total-compensation/

- Paycom. “What Is Total Compensation? A Complete Guide.” www.paycom.com/resources/blog/total-compensation/

- Salesforce. “What Is Total Compensation? How to Calculate + Guide.” www.salesforce.com/sales/performance-management/total-compensation/

- University of Wisconsin–Madison Division of Extension. “Understanding the Total Compensation Statement Benefits Everyone.” farms.extension.wisc.edu/articles/understanding-the-total-compensation-statement-benefits-everyone/

- Indeed Career Guide. “Salary vs. Total Compensation: What’s the Difference?” www.indeed.com/career-advice/pay-salary/salary-vs-total-compensation

- U.S. Bureau of Labor Statistics. (June 18, 2024). “Employer Costs for Employee Compensation — March 2024.” https://www.bls.gov/news.release/ecec.nr0.htm

- Entis, Laura. (March 31, 2016). “Salesforce Spent $3 Million to Close Its Gender Pay Gap.” Fortune. https://fortune.com/2016/03/31/salesforce-gender-pay-gap/

- U.S. Bureau of Labor Statistics. “Employer Costs for Employee Compensation — Tables.” https://www.bls.gov/news.release/ecec.toc.htm

- U.S. Bureau of Labor Statistics. “Employee Benefits Survey.” https://www.bls.gov/ncs/ebs/benefits.htm

- U.S. Department of Labor. “Wages.” https://www.dol.gov/general/topic/wages

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Brittany McMillen

Brittany McMillen

Brittany McMillen

Brittany McMillen