Corporate culture refers to a shared set of norms, values, assumptions, and beliefs that govern employees’ organizational behavior in a workplace. This culture defines how employees behave in the organization with one another, and it influences each one in some way or the other. As for organizations that operate in virtual workplaces, employees are connected remotely. Hence, a shared set of values is often missing. Therefore, an increasing need to teach a healthy virtual culture ensures that each remote worker feels a part of the team (sense of belonging).

Why do Virtual Workplaces Require a Corporate Culture?

It is essential to identify why a virtual workplace requires a corporate culture. First, there needs to be sufficient trust among remote employees. Lack of trust among employees connected virtually can lead to work disruptions, such that employees may not be willing to workas a team.

Second, to introduce the leadership model in a virtual workplace, a set of shared beliefs and values becomes inevitable. People who are connected remotely will find it very difficult to accept another remote employee’s leadership. Leadership is not only a requirement for physical workplaces but becomes even more important if geographical locations separate employees.

Employees in a virtual workplace may also feel isolated as their interaction is limited, which obstructs open, informal, and social communication between team members. This hampers employees’ growth aspect in terms of social skills, effective communication skills, and interaction outside of the work environment. Digital interaction does not allow for gestures, body language, and a pat on the back for a job well done. These elements tend to be missing in a virtual workplace, but a common corporate culture could fill in this void to some extent.

How to Build a Corporate Culture in a Virtual Workplace

The following are a few methods that may be used to stimulate a corporate culture in a virtual work setting:

Computer-based chat rooms must be set up for remote employees to discuss and perform work projects. This will enable open communication channels in a virtual workplace.

Moreover, virtual collaborative tools may be used to exchange ideas, share viewpoints and opinions on the various tasks assigned to remote employees, be it for basic bookkeeping.

To cultivate a culture whereby social skills may be enhanced, virtual socialization tools must be set to ensure that remote employees can engage in informal and personal conversations. This is likely to induce social interaction among employees and result in trust among remote employees, something they had been missing due to physical limitations.

Virtual employees lack a sense of engagement. This may be countered using video calls and video conferences to make face-to-face interactions possible. This way, gesturing and body language can be exercised to convey messages to remote employees.

Once in a while, employees may be arranged to meet one another at a conference or annual dinner physically. This is yet another way of ensuring that a corporate culture seeps into the virtual workplace.

These meetings will develop a set of shared values, beliefs, and norms that all remote employees can become accustomed to.

Another method to instill a corporate culture in the virtual workplace is through constant feedback from remote employees. Employees may be asked for their personal views regarding what’s missing in the virtual culture and what needs to be amended. Their valuable insights can be used to make the required alterations because the employees make up a corporate culture, after all.

Virtual employees may be granted full ownership of their projects to allow delegation. This is yet another method for ensuring trust among employees and inseminating a sense of belonging.

Conclusion

Virtual workplaces can make remote employees feel less motivated and alienated, provided the lack of physical interaction. However, corporate culture is necessary for a virtual work setting as they are for a physical workplace. Using the methods above, efforts may be dedicated toward establishing a virtual culture for remote employees.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

The analysis of financial statements is the process in which the company’s financial statements are reviewed and evaluated to understand the financial strength and enable the analyst to make effective decisions. Mainly, the companies’ financial statements are analyzed by the investors, creditors, company management, and the regulatory authorities. One of the standard tools used to analyze financial statements is the ratio analysis, which has been used in the current report.

In order to assess the company’s profitability, activity, and leverage, six ratios will be used and calculated to interpret the organization’s financial and operating performance.

Ratio Analysis

This section of the report involves the calculation, interpretation, and analysis of ratios to evaluate the financial and operational performance of the company. The ratio analysis is made on a comparative basis, either year on year comparison, ratio comparison with the competitor company, or the comparison with the average or benchmark of the industry. The six ratios that are calculated and used to analyze the performance from an investor’s perspective are appended below.

Return on Capital Employed (ROCE)

Return on Capital Employed is a profitability ratio, which compares the earnings and profit of the company based on the capital employed. The capital employed is the investment the company has made. Thus, the ROCE is also known as the return on investments. The return on the capital employed is calculated by dividing the earnings before interest and tax of the company of a year by the capital employed by the company of the same year. The capital employed includes the total equity and the liabilities for the long term of the business; in another way, the capital employed is calculated as total assets minus the company’s short-term liabilities.

Operating Profit Margin

The ratio indicates the percentage of the amount the company generates out of their revenue after deducting the day-to-day expenses. This ratio helps measure the operational effectiveness of the management of the business. The interpretation of operating profit margin varies from business to business or industry to industry. Such as the operating profit margin of the superstore will differ from the operating profit margin of the investment or real estate Company, as the nature of products and services differs.

Asset Turnover Ratio

The company acquires assets in order to do business, and a significant aim of business is to increase revenue. The asset turnover ratio measures the company’s ability to determine how much revenue the company generates from each unit of currency made as investments in assets. The asset turnover ratio helps identify the business’s asset utilization efficiency and effectiveness.

Gearing Ratio

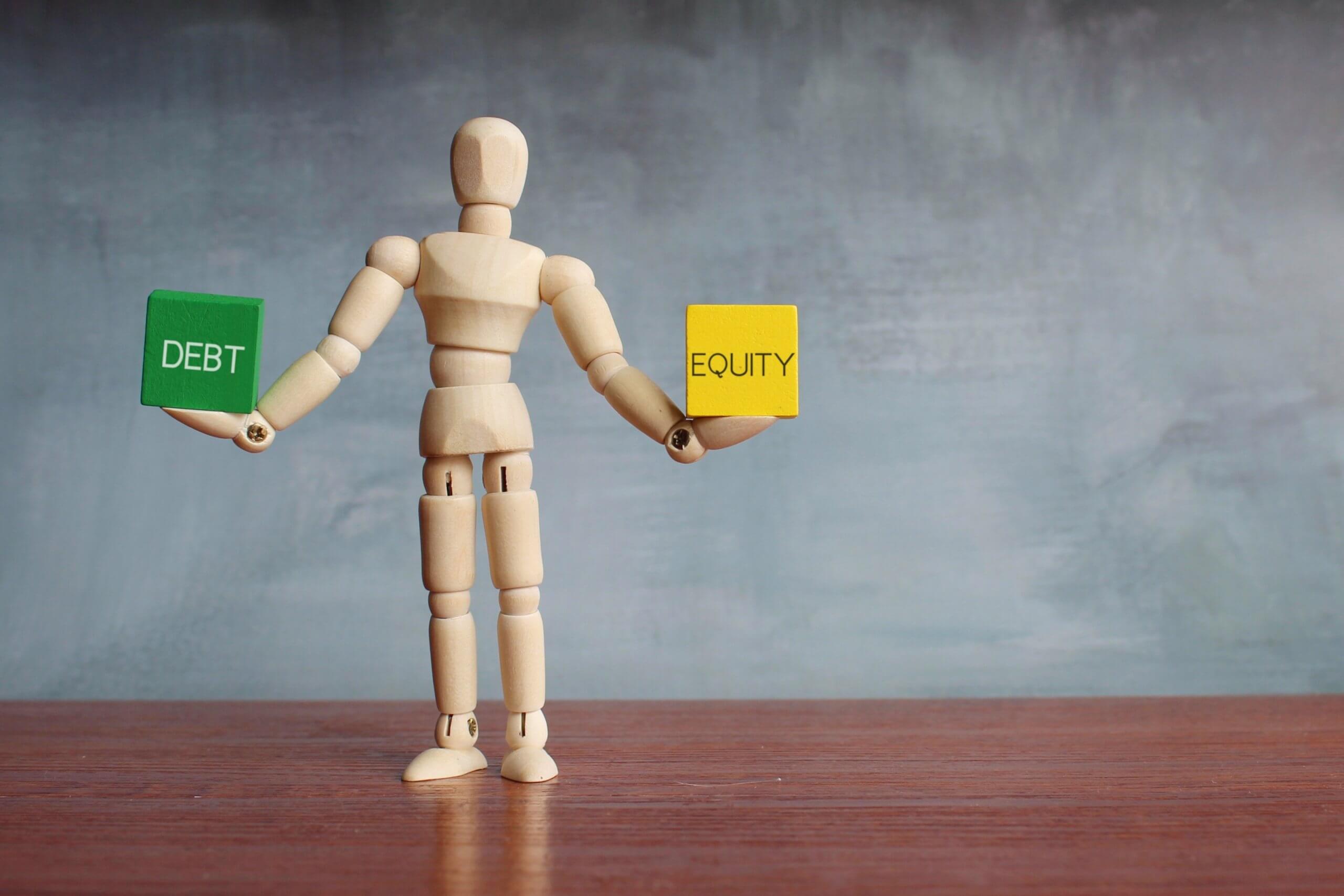

The calculation of the gearing ratio helps identify the characteristic of the company’s capital structure. The gearing ratio is a wide-ranging term used to denote the ratios that are to check the relationship between the firm’s equities and liabilities. There is a different form of gearing ratio available such as Non-current liabilities to equity, Long-term liability to Assets, and Total liability to equity. When comparing two companies or year-to-year comparisons, it is essential to ensure that the same form of gearing ratio is calculated to have accurate judgments. To clarify, the gearing ratio measures the level of debt in a capital structure in contrast to the level of equity of the company. The gearing of the company’s ratio tells the proportion of debts and equities in the company’s capital structure.

Interest Coverage Ratio

The interest coverage ratio is the more relevant for the creditors. The analysis of this ratio determines the capability of the company to pay off its interest expenses for the period. The interest coverage ratio is calculated by dividing the EBIT of the year with the interest charges of the same year, extracted from the company’s statement of profit and loss. This ratio explains to what extent the business can cover their interest payments from their earnings. The interest coverage ratio of less than 1 determines that the company’s EBIT is less than its interest payment. Thus, the company is unable to pay its fixed interest expenses: the higher the interest coverage ratio, the stronger position of the company in the eyes of an investor.

P/E Ratio (Price per Earning Ratio)

The P/E ratio of business is in relation to the company’s sharemarket performance with the comparison of a company’s business performance. This ratio links the association between the price of share and earnings per share in terms of how much it will take to protect the monetary value of a share. The P/E ratio has varying interpretations, such as the decreased P/E ratio implies the decreased market price of the share at the same time it can also imply an increase in earnings per share. Moreover, the higher the P/E ratio indicates the higher growth opportunity for the business in the future.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Intraday liquidity risk is an issue that applies to all banks. As of late, banks raised their capital and liquidity holds nearer to the levels required by controllers. A bank’s inability to meet intraday installments in an auspicious way adversely affects its liquidity position (flagging). Whatever remains of the money-related installment framework could be affected as well. This is due to the high level of interdependency between installment frameworks.

Banks should go along with direction on intraday liquidity risk if the neighborhood controllers embrace the regulator’s suggestions. The direction will oblige banks to effectively oversee, measure, and report intraday money streams under ordinary conditions.

Banks should build up an alternate course of action and demonstrate their flexibility under focused conditions.

The business sector for credit subsidiaries has become huge as of late. Notional measures of credit subordinates came to forty-five trillion dollars as of the middle of 2007, a fifty-fold increment from the level at mid-year 2001. The improvement of these instruments is a vital development, the most recent progression of advancements has significantly affected the nature and operation of credit markets. Like these prior developments, a key property of credit subsidiaries is that they isolate the start of credit, the financing of credit, and hold administration over credit danger. This detachment suggests the dissemination of credit danger over the budgetary framework and, thus, for the supply of credit. Banks that begin credit to corporate borrowers require no more hold the credit risk connected with these advances.

In contrast, other monetary firms can hold credit risk without originating or reserving the fundamental credit. In the conventional model of bank loaning, the bank plays out all parts of the credit procedure: starting the advance, holding it on the accounting report (subsidizing it), and holding and dealing with the related credit risk. Credit market advancements in the 1980s and 1990s changed this model in critical ways. Advancements, for example, advances deals, syndications, and securitizations, isolated the procedure of advance start – building up an association with the borrower, assembling and investigating data about the borrower’s creditworthiness, and setting up the terms of the advance – from subsidizing the advance. These courses of action also evacuated the credit risk connected with the advance. However, the starting bank, much of the time, gives credit ensures or holds a first-misfortune or other response position that has some bit of the credit risk presentation.

The recent system of the banking sector and financial institutions has developed a more efficient and active liquidity management system. The financial innovations have enabled banks to move from the model that used to be originated to hold that implies granting and custody of credits to the originate to distribute. This means relying heavily on the market financing and awarding of the transfer credit.

In any case, without store protection, liquidity shock may happen more unpredictably due to propagation around the soundness of the budgetary segment. This circumstance turns out to be even more trying for managing an accounting framework. Accordingly, these circumstances can test the financial industry’s versatility, against a liquidity shock, for instance, the new Islamic financial system. For banks, a money-related emergency may be especially more shocking because of the less created Islamic currency market, the absence of currency business sector instruments, and, in different purviews, nonattendance of the loan specialist of final resort office by the federal reserve bank. Commercial Banks are presented with the extra weight of store withdrawal risk in light of the fact that they share benefits and misfortune on venture stores.

The risk management department further branches into a novice concept known as Enterprise Risk Management (ERM). This department’s onus to resolve liquidity risk by implementing effective market risk management practices through their treasury department.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Most investors – if not all – are sometimes mistaken. Fortunately, one can learn from one’s mistakes and even others’. Here are ten examples of common mistakes and tips to avoid them.

The first thing about investing is to check if the person and the company offering the investment can sell it to you.

Modeling your investment decisions on those of the neighbor

Remember that an investment that suits one person will not necessarily be right for you. Modeling your investment decisions on those of the neighbor seems like a simple mistake to avoid. Here is an example of a situation that could risk influencing your investment choices. Each investor has its objectives, level of risk tolerance, and investment horizon. If you have a written investment policy that applies to all of your investments, it will help you avoid investing in investments that do not meet your investor profile.

Invest in an investment you do not know or do not understand

Here are some examples that may lead to investing in investments that we do not understand.

Investing simply because a financial analyst recommends the purchase

We have heard about society in the media, and it seems a good idea to invest.

Our representative offers us this investment. We trust it without thinking and without asking questions to understand the investment.

If you do not understand the investment that is offered to you, it is better to refine your financial knowledge first. One of your investor responsibilities is understanding the investment in which you invest. This includes understanding liquidity, performance, risk, and fees.

Buy based on information without having verified it

Never invest in investment without informing yourself. All information posted on the Internet is not accurate. For example, if a person predicts that the value of an investment will increase, this will not necessarily be the case. If it is a share of a company, it may be important to know what are the expected profits of that company.

Disregard his risk tolerance

When a representative asks you questions about your risk tolerance, answer as honestly as possible. For example, if you can not stand the value of your investments fluctuating, say so.

Do not admit mistakes

Some investors do not want to sell an investment at a loss, even if the future prospects of this investment deteriorate considerably, simply because they would admit they made a mistake.

Some investors even buy more of the same investment to lower their average acquisition cost. This strategy can sometimes work, but only if the value of the investment rises enough. If the value of the investment continues to fall, the loss will be more significant.

To help you avoid this error, you may want to specify limitations in your investment policy, such as not investing more than a certain percentage of your portfolio in a corporation.

Do not confuse this error with not selling your investments when the stock market goes down.

Falling in love with a stock market

An investment you have had for a long time and has yielded a significant return has been steadily losing value for some time. Recent financial news does not seem positive about the future of business. Assuming it will revalue over time, you buy it back many times, even if it hurts the diversification of your portfolio.

It is risky to “fall in love” with a stock market and lose all objectivity. It is equally important to remember that a stock’s past performance never guarantees its future performance.

When you invest, put aside your emotions and set limits based on your risk tolerance and especially your investment horizon. Do not forget the principles of portfolio diversification.

Adopt confirmation bias

This error consists of listening only to the tips and information that corroborate what you already think. For example, you believe that a title will gain value. Remember all the positives that support your hypothesis, for instance, that the company operates in a promising sector and has little debt.

On the other hand, you are not interested in anything that might affect the future value of the security, for example, whether a major new entrant enters the industry or the company does not clear profits.

Adopt a bias of optimism

This bias consists of thinking of oneself better than one is and seeing the future more positively than reality. This bias can be detrimental to investors, such as investing in seeing only potential earnings and forgetting the risks.

One way to reduce the errors caused by this bias is to ask yourself what is the worst loss you could incur by investing in the targeted investment. To do this, look at the stock market fluctuations of the security. This fluctuation could happen again, even if the past is not a guarantor of the future.

Perform a naive diversification

Naive diversification is meant to equitably distribute its money among all products offered, regardless of whether these products are similar or different. For example, if the representative offers us four equity funds and one bond fund, we invest one-fifth in each fund.

Adopt an employer bias

This mistake consists of investing an inordinate proportion of a company’s assets simply because “it is a good company.” Even if the idea of investing in a known sector is good, it should not hurt the basic principles of investment, such as diversification. Worse: If the company you are working for is in financial difficulty, you could lose both your job and see the value of your securities drop considerably.

One way to limit the consequences of certain behavioral biases is to invest money in a diversified portfolio periodically.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Maximize Your Rental Property Investment with Proven Tips

Rental property investment tips focus on strategic approaches that maximize profitability through market analysis, property improvements, smart financing, and effective management practices. The most successful investors combine thorough local market research with targeted property upgrades, creative financing strategies, and professional property management to generate consistent passive income while building long-term wealth through appreciation.

Over my 20 years as CEO of Complete Controller, I’ve had the privilege of working with real estate investors across every market cycle, watching some build empires while others struggle with cash flow. The difference? Strategic implementation of proven investment principles combined with meticulous financial management. With national rental vacancy rates dropping to just 6.9% in Q4 2024 and single-family rental occupancy hitting 94.6%, the rental market presents exceptional opportunities for prepared investors. This guide reveals the exact strategies our most successful clients use to maximize returns, minimize risks, and create sustainable passive income streams that weather any economic storm.

What are the best rental property investment tips for success?

Conduct comprehensive market analysis, optimize cash flow through strategic improvements, leverage creative financing, maximize tax benefits, and implement professional property management

Market analysis involves studying local rental rates, demographic trends, and economic indicators to identify profitable investment opportunities

Strategic property improvements focus on high-ROI upgrades like kitchens and bathrooms that justify premium rents

Creative financing options include house hacking, HELOCs, and seller financing to minimize upfront capital requirements

Tax optimization through depreciation, expense tracking, and 1031 exchanges significantly improves investment returns

Strategic Market Analysis for Rental Property Success

Smart rental property investment begins with understanding your local market dynamics through comprehensive data analysis. Successful investors examine rental rates for comparable properties, evaluate employment trends, and identify neighborhoods with strong appreciation potential. This process involves analyzing population growth patterns, median income levels, and demographic shifts that directly impact rental demand.

Technology now enables sophisticated market analysis that goes beyond traditional methods. Machine learning algorithms analyze vast datasets to identify emerging rental markets before they become mainstream, while geospatial analysis reveals location-based opportunities that manual research might miss. Sentiment analysis of online reviews and listings provides insights into tenant preferences, helping investors understand which amenities and features command premium rents in specific markets.

Identifying profitable investment properties

The key to selecting winning properties lies in understanding the relationship between purchase price, rental income potential, and local market conditions. While the traditional 2% rule suggests monthly rent should equal 2% of purchase price, today’s markets often require more nuanced analysis. Properties near employment centers, quality schools, and expanding infrastructure typically offer superior long-term appreciation.

Location analysis extends beyond immediate neighborhood characteristics to include future development plans and demographic shifts. Properties in areas experiencing job growth from tech companies or healthcare expansions often see rapid rent appreciation. Evaluating a property’s condition relative to market standards helps identify value-add opportunities where strategic improvements can justify significant rent increases.

Advanced market research techniques

Modern investors utilize predictive modeling and data analytics to gain competitive advantages. These tools analyze historical trends, economic indicators, and demographic data to forecast future rental demand and price movements. Real-time market data from multiple listing services, combined with economic forecasts, enables investors to time acquisitions and identify undervalued opportunities.

Heat mapping technology visualizes rental demand patterns, vacancy rates, and price trends across neighborhoods, revealing micro-markets with exceptional potential. This granular analysis helps investors avoid oversaturated areas while identifying emerging neighborhoods positioned for growth.

Optimizing Rental Income Through Strategic Property Improvements

Property improvements represent direct paths to increased rental income, but success requires focusing on upgrades that deliver maximum return on investment. Since 1980, U.S. rent prices have grown at 3.94% annually, but from 2020 to 2024, growth accelerated to 5.97% yearly, creating opportunities for strategic improvements to capture premium rents.

Kitchen and bathroom renovations consistently deliver the strongest returns, as these spaces significantly influence tenant perception and rental decisions. Modern finishes, energy-efficient appliances, and quality fixtures can justify rent increases of 15-25% in many markets. Beyond major renovations, simple updates like fresh paint, modern lighting, and updated hardware create immediate visual impact at minimal cost.

High-ROI improvement strategies

Energy efficiency improvements reduce operating costs while attracting quality tenants willing to pay premium rents. LED lighting retrofits, programmable thermostats, and Energy Star appliances appeal to cost-conscious renters while potentially qualifying for utility rebates and tax credits. Smart home features including keyless entry systems and app-controlled thermostats position properties as modern and convenient.

Curb appeal improvements often provide exceptional returns relative to cost. Professional landscaping, updated exterior lighting, and fresh paint create positive first impressions that reduce vacancy periods and attract higher-quality tenant applications. Storage solutions, including built-in shelving and outdoor sheds, address common tenant pain points while differentiating properties from competition.

Revenue-generating amenity additions

Strategic amenity additions create supplemental income streams beyond base rent. On-site laundry facilities generate $50-200 monthly per unit while addressing a critical tenant need. Designated parking spaces command premiums of $50-150 monthly in urban markets, while storage units can add $25-75 per month.

Pet-friendly policies with appropriate fees capture a broader tenant pool while generating additional revenue. Outdoor amenities like grilling areas or garden plots create community atmosphere while justifying higher rents. The key lies in understanding target tenant demographics and providing amenities that solve real problems while generating positive returns.

Creative Financing Strategies for Rental Property Acquisition

Creative financing enables investors to acquire properties with minimal capital while optimizing long-term returns. House hacking has gained tremendous traction, with over 50% of Millennial and Gen Z buyers viewing the ability to rent out part of their home as extremely important, compared to just 39% of all buyers—a nine-percentage-point surge from 2021.

FHA loans enable house hacking with just 3.5% down payment, allowing investors to live in one unit while renting others to cover mortgage payments. VA loans offer zero-down options for eligible veterans, while conventional owner-occupant loans provide better rates than investment property financing. This strategy provides immediate cash flow while building equity through principal reduction and appreciation.

Leveraging home equity and alternative funding

Existing homeowners can tap accumulated equity through HELOCs, home equity loans, or cash-out refinancing to fund rental acquisitions. Each option offers distinct advantages: HELOCs provide flexible access to funds, home equity loans offer fixed rates and predictable payments, while cash-out refinancing potentially provides the lowest rates.

Private money lenders and hard money loans serve investors needing quick funding or facing traditional financing challenges. While interest rates run higher, the speed and flexibility enable investors to secure properties in competitive markets or fund renovations before refinancing into permanent financing.

Seller financing and creative deal structuring

Seller financing creates win-win scenarios when traditional financing proves challenging or when sellers need tax advantages from installment sales. Terms typically include 5-10 year balloons with interest rates slightly above market, providing sellers steady income while giving buyers time to improve properties and refinance.

Subject-to transactions, lease options, and master lease agreements provide additional creative strategies for acquiring properties with minimal capital. These techniques require careful legal structuring but can enable rapid portfolio growth for sophisticated investors willing to master complex strategies.

Tax Optimization Strategies for Rental Property Investors

Tax benefits significantly enhance rental property returns when properly leveraged. Investors can deduct all ordinary and necessary operating expenses including mortgage interest, property taxes, insurance, maintenance, repairs, property management fees, and professional services. These deductions often transform marginally profitable properties into strong cash-flowing investments.

Depreciation provides the most powerful tax benefit, allowing investors to deduct property costs over 27.5 years for residential rentals. This non-cash deduction reduces taxable income while building wealth through appreciation. A $275,000 property generates $10,000 annual depreciation deductions, potentially saving $3,000-4,000 in taxes depending on tax brackets.

Advanced tax planning techniques

Cost segregation studies accelerate depreciation by identifying property components depreciable over 5, 7, or 15 years rather than 27.5 years. This strategy front-loads deductions, improving early-year cash flow critical for portfolio growth. Professional studies typically identify 20-30% of property value for accelerated depreciation.

Section 1031 exchanges defer capital gains taxes and depreciation recapture when reinvesting proceeds into like-kind properties. This powerful strategy enables portfolio growth and geographic diversification while preserving capital. Strict timeline requirements demand professional guidance, but tax deferral can save 25-40% of sale proceeds.

Entity structuring and asset protection

Proper entity structuring optimizes tax efficiency while providing asset protection. LLCs offer pass-through taxation with liability protection, while series LLCs enable multiple property ownership under one entity umbrella. Strategic entity structuring combined with proper insurance creates multiple protection layers.

Real estate professional status unlocks ability to offset W-2 income with rental losses, providing significant tax advantages for qualifying investors. Requirements include 750 hours annual real estate activities and more time in real estate than other businesses, but benefits can save tens of thousands annually.

Property Management Excellence for Maximum Returns

Professional property management directly impacts profitability through reduced vacancies, quality tenant retention, and operational efficiency. Modern property management leverages technology to automate routine tasks while maintaining personal relationships that keep good tenants long-term. With occupancy rates reaching 94.6% for professionally managed properties, effective management strategies prove essential.

Comprehensive tenant screening protects against costly evictions while ensuring fair housing compliance. Effective screening includes credit analysis, employment verification, rental history review, and background checks applied consistently to all applicants. Quality screening reduces turnover costs averaging $3,500 per unit while protecting property condition.

Technology integration and automation

Property management software automates rent collection, maintenance coordination, and financial reporting while reducing administrative burden by 40%. Online payment systems improve collection rates while providing convenient options tenants expect. Automated late fee assessment and reminder systems improve on-time payment rates to over 95%.

Maintenance management platforms streamline vendor coordination, track expenses, and schedule preventive maintenance that extends property life while minimizing emergency repairs. Digital inspection tools document property condition with timestamped photos, protecting against deposit disputes while identifying maintenance needs early.

Retention strategies and tenant satisfaction

Long-term tenant retention dramatically improves profitability by eliminating turnover costs and vacancy losses. Proactive communication, responsive maintenance service, and renewal incentives for quality tenants reduce turnover rates below 25% annually. Regular property upgrades and amenity additions demonstrate commitment to tenant satisfaction.

Building community through tenant events, communication platforms, and shared amenities creates emotional connections that reduce turnover. Birthday cards, holiday gatherings, and referral bonuses cost little but generate significant goodwill. Professional management balances business efficiency with personal touches that make properties feel like homes.

ROI Calculation and Investment Performance Monitoring

Accurate ROI calculation enables informed investment decisions and performance optimization. Real estate consistently outperforms stock markets, with 20-year commercial real estate returns averaging 9.5% versus the S&P 500’s 8.6%. Residential and diversified real estate performs even better at 10.6% annually.

Basic ROI calculations divide annual net profit by total investment, providing simple return percentages. Cash-on-cash returns focus on actual cash invested rather than total property value, revealing leverage efficiency. Cap rates examine property performance independent of financing, enabling comparison across different investment scenarios.

Comprehensive performance analysis

Net Operating Income (NOI) isolates property performance from financing decisions, examining rental income minus operating expenses. This metric proves invaluable for refinancing decisions and property comparisons. Internal Rate of Return (IRR) calculations incorporate time value of money, providing sophisticated analysis for long-term holdings.

A Jacksonville case study demonstrates real-world returns: purchased for $143,000 in 2015, the property sold for $352,000 in 2024, generating $164,000 total profits. Returns included $13,000 net rental income, $4,000 tax savings, and $173,000 appreciation—showing how appreciation drives 91% of long-term returns.

Performance optimization through analysis

Regular performance monitoring identifies optimization opportunities through rent adjustments, expense reduction, or strategic improvements. Benchmarking against market performance reveals underperforming assets requiring attention. Monthly financial reviews track key metrics including occupancy rates, average rents, operating expense ratios, and maintenance costs.

Portfolio analysis examines performance across properties, identifying top performers for replication and underperformers for improvement or disposition. Cash flow projections inform refinancing timing, improvement budgets, and acquisition strategies. Data-driven decision making consistently outperforms intuition-based management.

Conclusion

Successful rental property investment requires integrating market analysis, strategic financing, property optimization, and professional management into a comprehensive strategy. The proven tips outlined here provide the roadmap for building substantial passive income while creating long-term wealth through real estate.

Through my work with Complete Controller’s real estate investor clients, I’ve witnessed the transformation that occurs when investors implement these strategies systematically. The difference between average and exceptional returns often comes down to attention to detail: thorough market analysis, strategic improvements, tax optimization, and professional financial management.

Your rental property success depends on taking action with the right knowledge and support systems. Whether you’re acquiring your first rental or optimizing an existing portfolio, professional financial management makes the difference. Visit Complete Controller to discover how our specialized bookkeeping, tax planning, and financial analysis services help real estate investors maximize returns while minimizing tax burden. Our team understands the unique challenges of rental property investment and provides the financial expertise you need to build lasting wealth through real estate.

Frequently Asked Questions About Rental Property Investment Tips

What is the minimum down payment needed for rental property investment?

House hacking with FHA financing requires just 3.5% down payment, while conventional investment property loans typically need 20-25% down. Creative financing options like seller financing or partnerships can reduce upfront capital requirements even further.

How much cash flow should I expect from a rental property?

Successful rental properties typically generate $200-400 monthly cash flow after all expenses, though this varies by market and property type. Focus on properties where rent exceeds all expenses by at least 20% to account for vacancies and maintenance.

What are the best markets for rental property investment in 2024?

Markets with job growth, population increases, and landlord-friendly regulations offer the best opportunities. Secondary cities near major metros often provide better cash flow than expensive coastal markets while maintaining appreciation potential.

How can I reduce rental property taxes legally?

Maximize deductions for operating expenses, utilize depreciation benefits, consider cost segregation studies for accelerated depreciation, and explore 1031 exchanges for property sales. Real estate professional status can unlock additional tax advantages for qualifying investors.

Should I manage rental properties myself or hire professional management?

Self-management saves 8-10% of rental income but requires significant time and expertise. Professional management makes sense for investors with multiple properties, limited time, or properties located far from their residence, as quality management often pays for itself through reduced vacancies and better tenant retention.

SmartAsset. “12 Creative Financing Strategies for Real Estate Investing.” 2024.

Zillow. “Rising Interest in House Hacking Among Young Home Buyers.” 2023.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Crypto Mining is an integral part of the cryptocurrency industry, but it is equally essential to discover some alternate way to authenticate the transactions taking place. This can be done by diving into a series of complicated mathematical and statistical equations in order to complete the entire data structure of a blockchain.

Eventually, this made one gigantic setback. It initially started with the scarcity of human resources who had the expertise of solving such types of equations. If this problem were remedied, the entire blockchain structure would instantly come tumbling down. Therefore, to offer benefits to such people in solving the equations, they are now reimbursed into the same cryptocurrency that they are validating. Finally, making crypto mining a profitable venture.

It is next to impossible to think that cryptocurrency can be snatched, unlike theft and burglary. Your account will never be identified or stolen if you are a crypto miner.

The main quarrel regarding cryptocurrency is with the country’s financial regulatory framework. To a large extent, cryptocurrency is not regulated. At the same time, in a few countries, it adheres to the guidelines, with specific parameters, because it is reflected as a commodity rather than some digital currency. But eventually, the transactions conducted under the ambit of cryptocurrency continue to remain anonymous and untraceable, therefore providing privacy to the identity of a crypto miner on how much money they are minting and for what purpose they are using.

To sum it all up, crypto mining can be a tremendous incentive feature with all of the benefits above.

Cryptocurrency, such as Bitcoins, makes its way into the market through Crypto Mining. In this overall activity, a user’s engagement with a computer and the internet must be in place at all times. They are primarily the participants who are responsible for having technological paraphernalia; secondly, their details can be verified by assigning unique keys or digital wallets and allowing the payments to be stored into a data warehouse for mining Bitcoins, as per the rule of supply and demand and transaction fees.

Sighting Bitcoin as an example, some people voiced their concerns regarding the system’s vulnerability by stating that the application can be hacked or is susceptible to cyber-attacks, consequential from a leading group of people who want to abuse the primary purpose of cryptocurrency and insisted that such a risk could be mitigated through sharing crypto mining.

This is because blockchain management alluded from crypto mining is predicted to decline to a large extent, which may lower the benefits of mining the data. Crypto miners reduce the probability of avoiding a monopolistic economy or environment increase, which leaves the cryptocurrency vulnerable to a hostile takeover by fifty percent to a single user or entity. To put it simply, one owns more than fifty percent stake in the cryptocurrency network. It will allow that particular user to double the volume of the transactions by utilizing more coins. Due to this, the concept of Altcoins came into play by combing the technological framework of Bitcoins and IOTA. By adding a tangle to the cryptocurrency network, ensures PoS, fresh-minted coins are produced based on the resources of the individuals or entities. To put it simply, anyone who holds one percent of the cryptocurrency will only produce one percent of PoS coins. With this minor modification, the apprehension of running into the risk of a monopolistic environment will drastically reduce as the drawback of creating a monopoly will be costly.

While mining a block in the case of Bitcoin, the miner has to adhere to specific guidelines. It comprises an array of steps in sequential order to motivate the miner to be a part of a competitive environment, with unlimited and unimaginable CPU configuration to deduce a hash aligned to the requirements using any available algorithmic functions.

In deriving a hash, one has to follow a predetermined process that essentially is a one-way street. Once you enter the domain of deducing the hash, there is no going back. In addition, they need to make it difficult and impossible to decipher, which in other words, is also called proof of work.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Effective Strategies to Prevent Employee Theft in Your Organization

Prevent employee theft through layered defenses including robust hiring screens, clear anti-theft policies, surveillance systems, regular audits, and a culture of accountability that together reduce theft risks by 80-90%. These comprehensive measures create multiple barriers against theft, deter potential offenders before they act, and enable early detection of any incidents that do occur.

As the founder of Complete Controller, I’ve witnessed employee theft devastate small businesses over my 20 years serving thousands of clients across every industry. One painful case involved a trusted bookkeeper who skimmed $50,000 over 18 months before our audit protocols caught the discrepancies. The good news? With the right controls in place, 75% of employees who admit to workplace theft can be deterred before they ever act, and organizations with high engagement see 28% less internal theft. This guide shares battle-tested strategies that have saved my clients millions in prevented losses.

What are effective strategies to prevent employee theft in your organization?

Prevent employee theft through layered defenses: strong hiring, policies, tech, audits, training, and culture that deter 80-90% of risks before they occur

Background checks and integrity screening identify high-risk hires early, reducing theft by spotting past fraud patterns

Surveillance, access controls, and regular audits catch discrepancies in real-time—CCTV alone can reduce incidents by 40% within three months

Training programs and anonymous reporting channels build ethical awareness, turning employees into allies against theft

Fair pay and employee perks address financial motivations, with every $1 wage increase preventing $0.39 in theft losses

Put Theft Prevention in Hiring: Screen Smarter from Day One

To effectively prevent employee theft, start your defense at recruitment with comprehensive background checks that include criminal records, credit reviews where legally permitted, and thorough reference verification. At Complete Controller, implementing mandatory screening for all finance positions has caught two potential fraud risks among our last 50 hires—saving us from potentially catastrophic losses.

The statistics support this approach: 75% of employees admit to stealing at least once from their employer, with losses reaching $112.1 billion annually in retail alone. By screening candidates thoroughly, you filter out the highest-risk individuals before they gain access to your assets.

Background checks and integrity assessments

Run comprehensive checks that comply with FTC guidelines and the Fair Credit Reporting Act. Modern ethical AI tools can flag behavioral red flags during pre-hire assessments without introducing bias, giving you deeper insight into candidate integrity.

Reference verification for theft risks

Ask previous employers directly about integrity concerns—this step reveals patterns that public records miss. Frame questions around handling of company property, cash management experience, and any concerns about trustworthiness.

Clear, written policies that define theft broadly—including cash, inventory, time, and data—with zero-tolerance consequences deter 70% of opportunistic acts when properly communicated. Your policy should spell out that violations result in immediate termination and potential prosecution, then make these policies accessible through employee handbooks, your intranet, and annual reviews.

According to the Association of Certified Fraud Examiners, 43% of fraud cases are discovered through employee tips. This means your honest employees are your best defense—but only if they know what to watch for and feel safe reporting it.

Consequences and progressive discipline

Outline escalating penalties for policy violations and train supervisors on consistent application. Document every incident, no matter how minor, to establish patterns and protect against wrongful termination claims.

Anonymous reporting channels

Provide retaliation-free hotlines or digital reporting apps that protect whistleblowers. When employees trust the system, they become your most effective fraud detection tool—catching problems 50% faster than traditional audits according to recent studies.

Install Security Tech That Deters Without Alienating

Visible CCTV cameras, access controls, smart locks, and AI monitoring systems dramatically reduce theft by limiting opportunities. Real-world results prove the investment: a Midwest convenience store chain saw theft drop 40% within three months of installing remote monitoring, while a California electronics retailer reduced losses by 37% in one quarter through AI-powered cameras that caught an organized retail crime ring.

Position cameras strategically at cash registers, stockrooms, and high-value areas while respecting privacy in break rooms and restrooms. Pair visual surveillance with mobile alerts that notify managers of after-hours access or suspicious patterns.

Access controls and smart locks

Restrict stockrooms and cash handling areas to authorized staff using keypads, key cards, or biometric systems that track every entry. When employees know their access is logged and monitored, opportunity-based theft plummets.

Case Study: Technology Integration Success

A major retailer combining InVue’s Smart Locks with transaction pattern analysis reduced employee theft by 40% in one year. Their loss prevention team identified anomalies in real-time while staff training reinforced proper procedures. Result: $200,000 saved annually with full ROI achieved in four months.

Run Regular Audits and Segregate Duties to Catch Issues Early

Conduct surprise audits of inventory counts, transaction records, and cash deposits while rotating duties to prevent any single employee from controlling an entire financial process. One person shouldn’t handle receiving payments, recording transactions, and making deposits—this segregation stops 90% of embezzlement schemes before they start.

At Complete Controller, our monthly reconciliation protocols flagged a $10,000 discrepancy in a client’s books that traced back to an accounts receivable clerk creating false credit memos. Without segregated duties and regular reviews, this theft could have continued indefinitely.

Transaction pattern analysis

Review sales data for red flags like excessive voids, suspicious refunds, or transactions processed after hours. Modern Complete Controller accounting software automates this analysis, flagging outliers for investigation.

Inventory and cash handling checks

Implement daily cash counts with manager oversight and surprise inventory audits. Document variances immediately and investigate patterns—consistent small shortages often indicate ongoing theft.

Train and Build a Culture That Prevents Employee Theft

Organizations with highly engaged employees experience 28% less internal theft, proving that culture directly impacts your bottom line. Ethics workshops, scenario-based training, and regular policy reviews reinforce integrity standards while building team cohesion. When you reward honesty and create genuine connections, valued employees become theft prevention allies.

Foster transparency with open-door policies and regular check-ins. Employees who feel heard and appreciated rarely risk their positions through theft, especially when they see leadership modeling ethical behavior consistently.

Ongoing ethics and awareness training

Cover real scenarios your employees might face: pressure to let friends slide on payments, temptation to take home supplies, or requests to falsify time records. Our firm saw policy compliance rise 25% after implementing quarterly ethics refreshers that included role-playing exercises.

Pay Fairly and Offer Perks: Address Financial Motives

Harvard Business School research proves that competitive wages directly prevent employee theft—a $1 hourly raise costs $16,285 annually but prevents $6,362 in theft, recovering 39% of the investment through loss prevention alone. Higher pay also creates positive spillover effects: well-compensated team members monitor each other and establish workplace norms against stealing.

Beyond wages, provide mental health resources, flexible scheduling, and small perks like free snacks or parking. These benefits address the desperation that drives 15% of employee theft cases while building loyalty that makes theft unthinkable.

The Human Side of Theft Prevention: Schedule regular one-on-ones to catch financial stress early. An employee struggling with medical bills needs support, not surveillance. Proactive assistance prevents desperate choices.

Final Thoughts

Implementing these layered strategies—smart hiring, clear policies, strategic technology, regular audits, cultural investment, and fair compensation—creates comprehensive defense against the 75% of employees who might otherwise steal. These aren’t just theories; I’ve applied them across hundreds of Complete Controller client businesses, transforming vulnerable operations into secure, profitable enterprises.

Start today with a policy audit, then layer in technology and training for measurable results within 90 days. Your investment in prevention pays dividends through protected assets, improved morale, and sustainable growth. Ready to implement bulletproof financial controls? The experts at Complete Controller can design custom theft prevention protocols tailored to your business needs.

Frequently Asked Questions About Prevent Employee Theft

How common is employee theft in small businesses?

Employee theft affects 95% of all businesses, accounting for $50 billion in annual losses. Small businesses suffer disproportionately, with 68% of prosecuted cases occurring in organizations under 500 employees.

What are the most common warning signs of employee theft?

Watch for unexplained inventory shortages, excessive transaction voids or refunds, employees who never take vacation, lifestyle changes beyond their salary level, and resistance to new controls or audit procedures.

Should I immediately confront an employee I suspect of stealing?

No, investigate discreetly first through audits and documentation review. Premature confrontation risks legal issues and evidence destruction. Consult legal counsel before taking action.

Is employee video surveillance legal?

Yes, workplace surveillance is legal when disclosed in company policy and limited to work areas. Follow SHRM guidelines and avoid cameras in private spaces like restrooms or changing areas.

How much should I invest in theft prevention technology?

Most businesses recover their theft prevention technology investment within 6-12 months. Start with high-risk areas and expect 30-40% reduction in losses from properly implemented systems.

Case IQ. “Detecting and Preventing Employee Theft: The Ultimate Guide.” CaseIQ.com, n.d.[7].

U.S. Chamber of Commerce. “How to Prevent Employee Theft.” USChamber.com, n.d.[9].

Accounting Department. “How to Deter Employee Theft When You Run a Cash Business.” AccountingDepartment.com, n.d.[11].

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

The Complete Process of Recruitment in an Organization

Recruitment transforms your business needs into a systematic process for finding, evaluating, and integrating the right talent into your organization. This comprehensive approach encompasses everything from identifying staffing requirements through workforce planning to implementing effective onboarding programs that convert new hires into productive team members.

Over my 20 years as CEO of Complete Controller, I’ve witnessed firsthand how strategic recruitment practices can make or break a company’s growth trajectory. The average business loses $4,683 per bad hire, yet companies using structured recruitment processes see 82% higher retention rates. This article reveals the exact recruitment framework we’ve refined through working with thousands of businesses, giving you the tools to build a hiring system that attracts top talent while reducing costs and time-to-hire by up to 40%.

Workforce Planning: Analyzing current skills against future business needs to identify hiring priorities

Talent Acquisition: Sourcing candidates through multiple channelsincluding job boards, referrals, and social media

Candidate Evaluation: Screening resumes, conducting interviews, and assessing cultural fit

Hiring Decisions: Making offers based on skills, experience, and organizational alignment

Employee Onboarding: Integrating new hires through structured training and mentorship programs

Strategic Workforce Planning Sets the Foundation

Strategic planning forms the bedrock of successful recruitment by aligning your hiring needs with broader business objectives. Organizations that implementeffective workforce planning strategies reduce their hiring costs by an average of 22% while improving the quality of their hires.

The process begins with a thorough demand analysis that examines your current team’s capabilities against projected business goals. This involves mapping existing skills, identifying gaps, and forecasting future requirements based on market trends and growth projections. For instance, Complete Controller’s quarterly skills audit revealed that 35% of our technical positions could be filled through internal promotions, saving over $150,000 annually in external hiring costs.

Key components of workforce planning

Skill gap identification through team assessments

Future-proofing by anticipating emerging role requirements

Budget allocation based on role priorities and market rates

Internal mobility evaluation to reduce external hiring needs

Timeline development for phased hiring initiatives

The data speaks volumes about planning’simpact. According to AMS & Josh Bersin Co., companies without structured workforce planning experience an average time-to-hire of 67 days for specialized roles, compared to just 44 days for organizations with defined processes. This 23-day difference translates to thousands in lost productivity and increased recruitment costs.

Creating Job Descriptions That Attract Quality Candidates

Your job description serves as the first touchpoint between your organization and potential talent. A well-crafted posting does more than list responsibilities – it sells your company culture and growth opportunities while clearly defining expectations.

Start with a compelling job title that accurately reflects the role while incorporating searchable keywords. Instead of “Marketing Ninja,” use “Digital Marketing Manager” to improve visibility in job searches. Your opening paragraph should immediately convey what makes this opportunity unique, whether it’s innovative projects, career advancement paths, or exceptional company culture.

Essential elements of effective job descriptions

Clear role title with industry-standard terminology

Compelling company overview highlighting culture and values

Specific responsibilities broken into primary and secondary duties

Required skills separated from preferred qualifications

Salary range and benefits overview

Growth opportunities and career development paths

Application instructions with expected timeline

When writing requirements, distinguish between must-haves and nice-to-haves. This prevents qualified candidates from self-selecting out due to overly restrictive criteria. Research shows that women typically apply only when meeting 100% of qualifications, while men apply when meeting just 60%.

Multi-Channel Sourcing Maximizes Candidate Reach

Modern recruitment demands a diversified approach to candidate sourcing. Relying solely on job boards limits your talent pool and increases competition for the same candidates that every other company is pursuing.

Employee referral programs consistently deliver the highest-quality candidates with 45% better retention rates than traditional sourcing methods. Complete Controller’s referral program, which offers tiered bonuses based on role difficulty, generates 30% of our hires while costing 50% less than external recruiting.

Proven sourcing channels and their effectiveness

Employee Referrals (30% of hires): Higher retention, faster onboarding, cultural fit

LinkedIn and Professional Networks (25% of hires): Direct access to passive candidates

Niche Job Boards (20% of hires): Industry-specific talent with relevant experience

University Partnerships (15% of hires): Entry-level talent with fresh perspectives

Internal Promotions (10% of hires): Cost-effective with minimal training requirements

Passive candidate outreach requires a different strategythan active job seekers. These professionals aren’t browsing job boards but might consider the right opportunity. Craft personalized messages highlighting specific achievements from their profile and explaining why they’d excel in your role. Response rates jump from 3% with generic messages to 27% with personalized outreach.

Screening and Assessment Strategies That Work

Efficient screening separates viable candidates from the overwhelming volume of applications modern postings generate. The average corporate job posting receives 250 resumes, yet only 4-6 candidates typically receive interviews.

Applicant Tracking Systems (ATS) provide the first filter, scanning resumes for keywords and qualifications. However, over-reliance on automation can eliminate qualified candidates who format their resumes differently. Balance automated screening with manual review of promising applications that may not perfectly match ATS criteria.

Three-stage screening process

Initial ATS Screening (250 → 50 candidates)

Keyword matching for essential skills

Education and experience verification

Location and availability confirmation

Manual Resume Review (50 → 15 candidates)

Context evaluation beyond keywords

Career progression analysis

Red flag identification (unexplained gaps, job hopping)

Phone Screening (15 → 6 candidates)

Salary expectation alignment

Cultural fit assessment

Communication skills evaluation

Phone screens save significant time by identifying misalignments before investing in lengthy interviews. Keep these conversations to 20-30 minutes, focusing on deal-breakers like salary requirements, relocation willingness, and basic qualifications.

Interview Design for Comprehensive Evaluation

Structured interviews improve hiring accuracy by 26% compared to unstructured conversations. This systematic approach ensures every candidate faces similar questions, enabling fair comparisons while reducing unconscious bias.

The behavioral interview method, particularly the STAR framework (Situation, Task, Action, Result), revealshow candidates handled real workplace challenges. Instead of hypothetical scenarios, ask about specific past experiences that demonstrate required competencies.

Sample STAR questions by competency

Leadership: “Describe a time you motivated an underperforming team member“

Problem-Solving: “Walk me through resolving a major customercomplaint“

Adaptability: “Share an example of adjusting your approach mid-project“

Collaboration: “Explain how you resolved conflict with a colleague“

Technical assessments complement behavioral interviews by validating claimed skills. Tailor these evaluations to mirror actual job tasks rather than abstract problems.A content writer might draft a blog post, while a programmer could debug existing code. These tips for successful job interviews help both interviewers and candidates prepare effectively.

Panel interviews involving future teammates provide multiple perspectives while allowing candidates to meet potential colleagues. Rotate panel members to prevent groupthink and assign specific evaluation criteria to each interviewer. This approach reduced our hiring mistakes by 35% while improving new hire satisfaction scores.

Making Data-Driven Hiring Decisions

The hiring decision extends beyond selecting the most qualified candidate. Consider cultural fit, growth potential, and team dynamics alongside technical skills. Research indicates that 89% of hiring failures result from poor cultural fit rather than skill deficiencies.

Create a standardized evaluation matrix weighing different factors according to role requirements. Technical positions might emphasize skills (40%), problem-solving (30%), cultural fit (20%), and growth potential (10%). Leadership roles could prioritize differently: leadership experience (35%), cultural fit (30%), strategic thinking (25%), and technical knowledge (10%).

Decision framework components

Skill assessment scores from technical evaluations

Behavioral interview ratings from multiple interviewers

Reference check insights validating past performance

Cultural fit indicators from team interactions

Compensation alignment with budget and market rates

Growth trajectory matching organizational needs

Reference checks remain crucial despite many companies providing only employment verification. Ask specific questions about the candidate’s performance, work style, and areas for development. Former colleagues often provide more candid feedback than supervisors bound by company policies.

Crafting Competitive Offers That Close Deals

Your offer package competes not just on salary but on total value proposition. Top candidates often evaluate multiple opportunities simultaneously, making your offer presentation crucial for securing acceptance.

Market research ensures competitive compensation. Use multiple salary surveys and adjust for location, industry, and company size. Offering below-market rates might save money initially but increases turnover costs long-term. Remember that replacing an employee costs 50-200% of their annual salary.

Comprehensive offer components

Base salary aligned with market rates and internal equity

Performance bonuses or commission structures

Equity compensation for key positions

Health insurance with multiple plan options

Retirement contributions with company matching

Professional development budgets

Flexible work arrangements

Paid time off and holiday schedules

Present offers verbally first to gauge reactions and address concerns immediately. This conversation allows negotiation without formal counter-offers that can complicate the process. Follow up with written offers detailing all components, start dates, and response deadlines.

Scaling your team? Make sure your systems can scale with you. Complete Controller can help.

Background Verification and Compliance

Background checks protect your organization from negligent hiring lawsuits while verifying candidate claims. However, compliance with federal, state, and local regulations requires careful attention to avoid discrimination claims.

The Fair Credit Reporting Act (FCRA) mandates specific procedures for background checks, including written consent and adverse action notices. State laws may impose additional requirements, such as “ban the box” regulations delaying criminal history inquiries until conditional offers.

Standard background check components

Employment verification confirming roles and dates

Education credential validation

Criminal record searches at county, state, and federal levels

Credit checks for financially sensitive positions

Professional license verification

Motor vehicle records for driving positions

Partner with reputable background check providers familiar with compliance requirements. Establish clear policies about which findings disqualify candidates, considering the role’s requirements and time elapsed since incidents. Document all decisions to demonstrate consistent, non-discriminatory practices.

Onboarding Programs That Drive Retention

Effective onboarding extends far beyond paperwork and policy reviews. Organizations with structured employee onboarding best practices see 82% higher retention and 70% productivity improvement within the first year.

Your onboarding program should blend administrative tasks with cultural integration and role-specific training. New hires form lasting impressions during their first weeks, making this period critical for long-term success.

First day essentials

Prepared workspace with necessaryequipment

Welcome package including company swag and resources

IT setup with system access and training scheduled

Team introductions and organizational chart review

Lunch with immediate team members

Clear first-week schedule and expectations

The first 90 days establish performance patterns and cultural integration. Create milestone checkpoints at 30, 60, and 90 days to assess progress and address concerns. Assign mentors who guide new hires through unwritten cultural norms and provide safe spaces for questions.

Structured 90-day onboarding timeline

Days 1-30: Foundation Building

Complete administrative requirements

Understand role responsibilities and expectations

Meet key stakeholders and team members

Begin basic job functions with close supervision

Days 31-60: Skill Development

Take ownership of initial projects

Receive targeted training for role-specific skills

Establish working relationships across departments

Provide feedback on onboarding experience

Days 61-90: Integration Completion

Operate independently on core responsibilities

Contribute ideas in team meetings

Receive performance feedback and goal setting

Plan professional development path

Measuring Recruitment Success and ROI

Recruitment metrics reveal process effectiveness and improvement opportunities. Track both efficiency measures (time and cost) and quality indicators (performance and retention) for comprehensive insights.

Time-to-hire averages 44 days globally but varies significantly by role complexity and industry. Monitor your timeline from requisition approval through accepted offer, identifying bottlenecks for improvement. Reducing time-to-hire by just one week can save thousands in lost productivity.

Key performance indicators for recruitment

Time-to-Fill: Days from job posting to accepted offer

Cost-per-Hire: Total recruitment expenses divided by hires

Quality-of-Hire: New hire performance ratings after 6-12 months

Offer Acceptance Rate: Percentage of offers accepted

Source Effectiveness: Hire quality by sourcing channel

Retention Rate: Percentage remaining after one year

Hiring Manager Satisfaction: Feedback on candidate quality

Candidate Experience: Applicant ratings of your process

Regular analysis identifies trends requiring attention. If offer acceptance rates drop below 80%, examine your compensation competitiveness or candidate experience. High early turnover suggests onboarding improvements or hiring criteria adjustments.

Technology and Automation in Modern Recruitment

Artificial intelligence transforms recruitment efficiency while maintaining the human touch essential for candidate experience. AI tools now handle 94% of initial resume screening, reducing time-to-hire by up to 75% for high-volume positions.

Unilever’s pioneering AI implementation processed 45,000 entry-level candidates through gamified assessments and automated video interviews. This workforce planning and talent acquisition insights approach saved over $1 million annually while improving diversity by removing unconscious bias from initial screenings.

AI applications across recruitment stages

Job Description Optimization: AI analyzes top-performing posts to suggest improvements

Resume Screening: Natural language processing evaluates experience beyond keywords

Interview Scheduling: Chatbots coordinate availability without manual back-and-forth

Predictive Analytics: Machine learning predicts candidate success and retention probability

Bias Reduction: Blind screening removes identifying information from initial reviews

However, technology supplements rather than replaces human judgment. AI excels at processing volume and identifying patterns but cannot assess cultural fit or soft skills requiring interpersonal evaluation. Balance automation with personal touches throughout the candidate journey.

Adapting Recruitment for Different Business Sizes