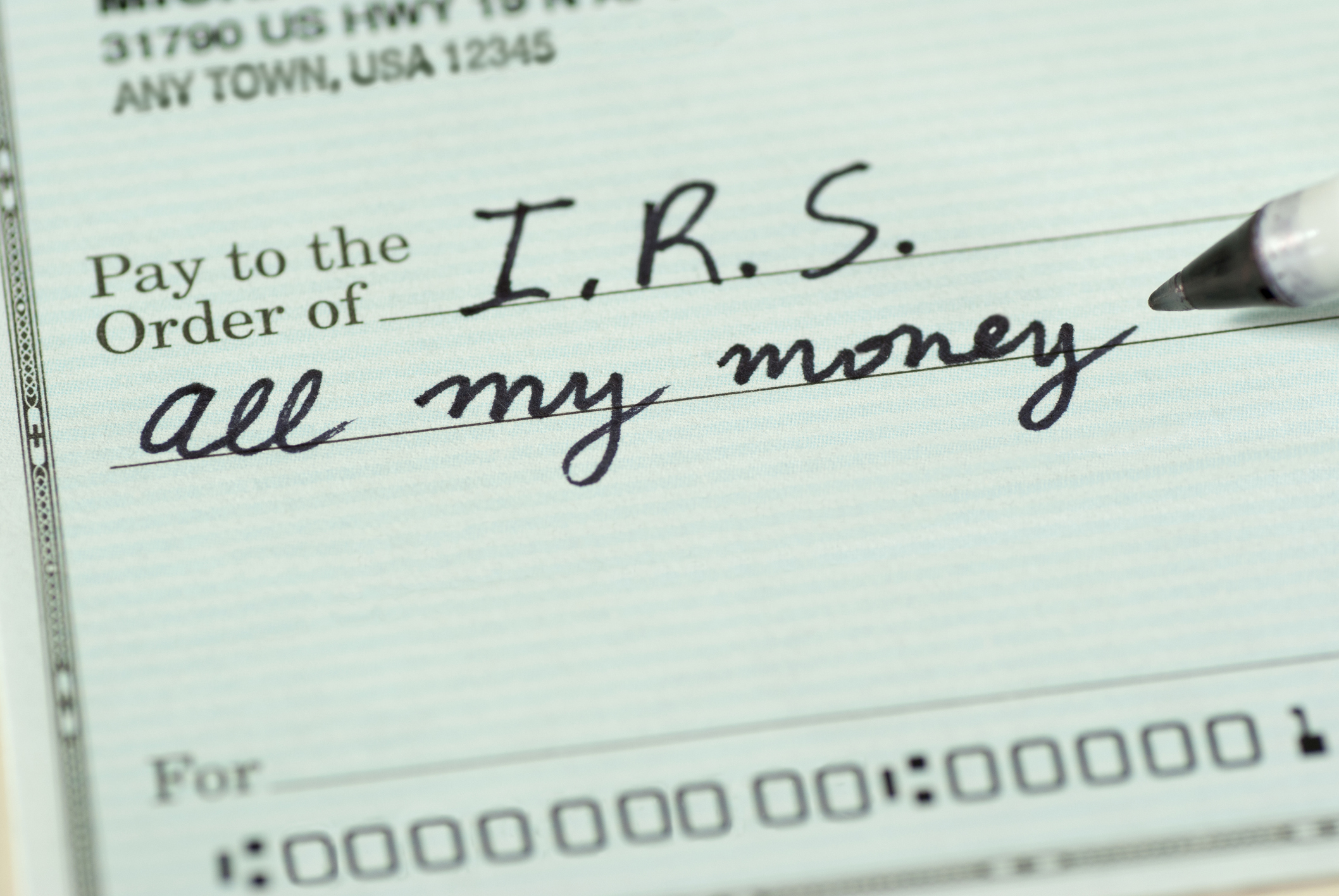

If you cannot pay your taxes, the Internal Revenue Service (IRS) can work with you and provide a payment plan to keep you on track. Any debt you have with the IRS can be paid with a portion of your future reimbursements. Here is information about the types of debts that are collectible or could intersect your tax refund.

The Department of Treasury’s Bureau of the Fiscal Service (BFS), which issues the IRS tax refunds, has been authorized by Congress to execute the Treasury Offset Program (TOP), a Treasury Compensation Program to compensate debts. Through this program, your refund or overpayment could be decreased by the BFS to compensate:

all arrears of child support payments for minor children;

all federal non-tax debt (such as student loans in arrears);

all-state income tax debt; or

certain unemployment compensation debts owed to a state. (Generally, these are debts for (1) compensation that was paid due to fraud or (2) for contributions owed to a state fund that were not paid due to fraud).

You can contact the agency with which you have a debt to determine if the debt was remitted for your tax refund to be applied against it. You can call the BFS TOP call center at the telephone number listed below to obtain a certain agency’s address and telephone number. If your debt was remitted to the BFS for compensation, it would take your refund as much as necessary to settle the debt and send the payment to the agency to which you owe some amount. After being applied against your debt, any remaining part of your refund will be sent to you in a check or deposited directly into your bank account.

The BFS will inform the IRS of the amount it took from your refund. You should contact the agency indicated in the notice if you believe the debt is not due or if you want to dispute the amount of your refund that was applied against a debt. If you do not receive the notification, contact the BFS TOP call center at 800-304-3107 or, for TDD team users, at 866-297-0517. Only call the IRS if the original refund amount indicated on the notice sent to you by the BFS is different from the amount shown on your tax return.

If you filed a joint return and are not responsible for the debt but are entitled to a portion of the refund, you can request that portion of the refund by filing Form 8379, Injured Spouse Allocation, in English. You can file Form 8379 with your original joint return (Form 1040, Form 1040A, or Form 1040EZ), with your amended joint return (Form 1040X), or file it separately after receiving the notice telling you that your refund was applied against an amount owed. If you file Form 8379 with your joint return, write the words “INJURED SPOUSE” in English on the upper left corner of the first page of the joint return. The IRS will process your Form 8379 before your refund is applied against an amount owed. If you file Form 8379 along with your original or amended joint return, processing the electronic return may take up to 11 weeks or, if you file a paper return, it may take up to 14 weeks.

If you file Form 8379 separately, it must show the social security numbers of both spouses in the same order in which they appear on the joint income tax return. You, the “injured” spouse, have to sign the form. Carefully follow the instructions on Form 8379 and attach the necessary forms to avoid delays. Do not attach to Joint Form 8379 the joint income tax return presented above. Send Form 8379 to the Service Center where you filed your original return and wait at least 8 weeks for IRS to file your Form 8379. The IRS will calculate the portion of the joint return that corresponds to the injured spouse and, if you lived during the tax year in a state where the community property law governs, the IRS would divide the joint reimbursement according to state law. Not all debts are subject to compensation from the tax refund. To determine if you have a debt (other than federal tax) and if compensation will occur, call the BFS TOP call center at 800-304-3107 (for help if you use TTY / TDD equipment, call 866- 297-051.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Depending on how old you are, saving for retirement may sound like something very distant, but the reality is that you will be 60 years old and want to have a calm and comfortable retirement before you know it. According to the National Population Council, the average life expectancy is 85 years.

If you consider that the average retirement age is 65 years old, this leaves you between 10 and 20 years in which you will have to live with your pension or what you have saved during your working life. Professor of the Specialization in the Disclosure of the Economy of the Interactive Museum of Economics (MIDE) says that saving for retirement is important. Whether you began saving early or started late, having some savings for retirement will be crucial.

Many people save for retirement through their workplace. There are generally options available outside of social security being collected. However, if you are in business for yourself or your workplace does not offer retirement plans, you may need to think about other savings options. Here are three options to help you save for retirement.

Retirement Fund Administrators

They are financial institutions specializing in retirement savings, where you must consider three things:

a) Net performance of the retirement fund administrator

b) Commissions that they charge for services

c) Services they offer towards retirement

Retirement fund administrators are available through firms and can be a great way to ensure you are set up well for retirement. This option will not be right for everyone.

Investment plans

With an investment plan, the first thing is to define how much you want for your retirement, and depending on that, you will make monthly, annual, or quarterly contributions depending on your profile. These savings will be invested in a portfolio of different assets that may include publicor private debt in national or foreign currency, shares of the country, or foreign companies.

For example, the national currency public debt is a debt with low risk but a lower yield. If we want to have more returns, other assets such as shares in companies in Mexico or abroad are increased. You can request investment fund advice or insurer investment funds specializing in retirement savings, regulated by the National Banking and Securities Commission (CNBV).

Life Insurance

Life insurance, also known as survival insurance, is a great way to save for retirement. This option creates security for you and your economic dependents in case of death or disability. In case of illness and not being able to work, you receive that money. Still, if none of these scenarios happen, in the end, they give you the amount saved. For this service, you can approach the insurers.

You can also check More Funds, an investment company that provides you with more than 140 options of market offers and can guide you so you know what the best option is.

The amount you should save

According to Sketch Guy Columnist Carl Richards, save the amount from your monthly income as much as you can. According to many reliable resources, you should save around 15% of your monthly salary as it is the best benchmark. The exact number for monthly savings depends on the level of your hope to work. It also relies on the type of inheritance you have and a bundle of unknown facts. You can start this campaign if the paycheck is $25 but, you should try to increase this rate every year.

The best time to do this is at the beginning of the year. The early you start saving some amount, the more you can polish this habit. Whatever the income you earn in a month, make sure saving some amount from it should be your second nature.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Insurance agents are, above all else, salespeople who are there to make sales. They will approach you like any other salesperson selling you luxury items. Insurance, whether auto, life, or health, is in some cases mandatory and in other cases needed as determined by the insured.

Because it is the insurance agent’s job to make sales, you should know as much as possible about the insurance you are purchasing, the legality requirements to carry insurance. You should also know everything there is to know about the insurance you need and the costs. The more prepared you are, the less likely you will purchase insurance you don’t need.

Here is some helpful insurance information, so you do not buy anything you don’t need when purchasing a policy.

What is an insurance policy?

The insurance policy is the manifestation of the most important agreement between clients and insurers. In it, the rights and obligations of both parties are regulated. We tell you everything you need to know about this document.

The time has come. You and your insurer have reached an agreement in the application and the proposal, the two main documents of the insurance contract. Therefore, the printing and subscription of the policy are carried out so that the treatment can be maintained over time and adapts to current legislation.

You should know that an insurance policy is not any document. It is the essential agreement between the insured and insurer so that all information we know about it will be especially useful.

A document covered by the legality

If the insurance policy stands out for anything, it is because of the extensive number of rules surrounding it. All these articles integrated into the Insurance Contract Law ensure, mainly, the protection of the client. So that insurers do not take advantage of the ignorance and innocence of the policyholder, the law guarantees a series of rules that all companies must comply with.

On the one hand, according to the law, this document must always be executed in writing, and the insurer must deliver an original copy of it to the new insured. The regulations leave very little room for the parties’ creativity to protect you as a customer when introducing clauses in the policies. Everything that is regulated in this law is what must be established in the document without exceptions.

To further defend the insured’s rights, the law also allows the Public Administration to control and supervise the contractual content of the policies. In this way, the policyholder will not be unprotected at any time.

What does it mean to establish an insurance policy with the insurer?

Conveniently, we know the functions and consequences that the policy of any insurance that we are going to hire will imply. It helps in having a broader view of what this essential document entails.

Birth of the contract

Suppose something indicates an insurance policy that is the birth of the contract between both parties. When the policyholder and insurer sign the document, the insurance is perfected. But this does not end here. In the case of paying the corresponding premium, at that time, the effects thereof will arise.

Irrefutable proof

The policy is proof in writing that the insurance we have contracted exists. In this way, possible frauds that could affect the client are avoided. If we do not know if our contract is still valid or not, we have it very easy: we have to look at the paid receipt of the current annuity.

Normative function

The essential function that we have already commented on the policies is the regulations. Why? Because, in it, the rights and obligations of the insurance we have contracted are detailed. What is written in the policy is so important that they have the force of law for the parties involved in the contract?

Details the pre-existence of the insured objectives

Under the Insurance Contract Law, the policy must state the insurance objectives of the companies. The presumption of pre-existence will favor the insured when more reasonable evidence cannot be provided reasonably.

Policyholder

If the insurance company has the legal form of mutual, the policy grants the mutual policyholder status, as long as they are not reflected otherwise in the document.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Unlike theft and burglary, it is next to impossible to think that cryptocurrency can be snatched. If you are a crypto miner, you can have a sense of calmness and peace that the money in your account will ever be identified or stolen.

Crypto Mining is an integral part of the cryptocurrency industry, but it is equally essential to discover some alternate way to authenticate the transactions taking place. It can be done by diving into a series of complicated mathematical and statistical equations to complete the entire data structure of a blockchain.

Eventually, this made one gigantic setback. It initially started with the scarcity of human resources who had the expertise of solving such types of equations. If this problem were remedied instantly, the entire structure of blockchain would come tumbling down. Therefore, to offer benefits to such people in solving the equations, they are now reimbursed into the same cryptocurrency they are validating. Finally, making crypto mining a profitable venture.

Unlike theft and burglary, it is next to impossible to think that cryptocurrency can be snatched. If you are a crypto miner, you can have a sense of calmness and peace that the money in your account will ever be identified or stolen.

After the person gets a good grip on crypto mining, it is very probable that you start your crypto mining business and be your owner. You earn handsomely, do not need to declare anything to the tax authorities, and enjoy the freedom if it lasts.

The main quarrel regarding cryptocurrency is with the country’s financial regulatory framework. Largely, cryptocurrency is not regulated, while in a few countries, it adheres to the guidelines, with certain parameters because it is reflected as a commodity rather than some digital currency. However, the transactions conducted under the ambit of cryptocurrency continue to remain anonymous and untraceable, therefore providing privacy to the identity of a crypto miner on how much money they are minting and for what purpose they are using. Crypto mining can be a tremendous incentive feature with all the benefits above to sum it all up.

Cryptocurrency, such as Bitcoins, make their way into the market through the process call Crypto Mining. In this overall activity, a user’s engagement with a computer and internet must always be in place. They are primarily the participants responsible for having technological paraphernalia; secondly, their details can be verified by assigning unique keys or digital wallets and allowing the payments to be stored in a data warehouse for mining Bitcoins the rule of supply and demand and transaction fees.

Sighting Bitcoin as an example, some people voiced their concerns regarding the system’s vulnerability by stating that the application can be hacked. Consequential from a leading group of people, who want to abuse the primary purpose of cryptocurrency, insisted that such a risk could be mitigated through sharing crypto mining.

As crypto miners reduce, the probability of avoiding a monopolistic economy or environment increases, which leaves cryptocurrencies vulnerable to a hostile takeover by fifty percent to a single user or entity. To put it simply one owns more than 50% stake in the cryptocurrency network, it will allow that user to double the volume of the transactions by utilizing more coins. Due to this, the concept of Altcoins came into play by combing the technological framework of Bitcoins and IOTA. By adding a tangle to the cryptocurrency network, ensures PoS, fresh-minted coins are produced based on the resources of the individuals or entities. To put it simply, anyone who holds one percent of the cryptocurrency will only produce one percent of PoS coins. With this small modification, the apprehension of running into the risk of a monopolistic environment will drastically reduce, as the drawback of creating a monopoly will be costly.

The above paragraph can be substantiated with the situation in July 2016, where the Bitcoin mining reward was reduced by 50%, resulting in having the miners switch to Peercoin for better returns and profitability.

While mining a block in the case of Bitcoin, the miner must adhere to certain guidelines, comprising an array of steps in sequential order to motivate the miner to be a part of a competitive environment, with unlimited and unimaginable CPU configuration to deduce a hash that is aligned to the requirements using any of the available algorithmic function.

In deriving a hash, one must follow a predetermined process that essentially is a one-way street. Once you enter the domain of deducing the hash, there is no going back. Almost all the miners are in the probe for a plausible solution the matches the criteria, no matter how many and how much equipment are required. Also, they need to make it difficult and impossible to decipher.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Savings money is something every financially responsible adult should do. However, according to recent research, around 40% of people in the US don’t have a backup to cover an emergency of $400, and nearly 39% have an emergency savings of $1,000.

These statistics allow you to learn how you can save your overall finances. However, having proper personal finances seems impossible for some people. People always wish to have money-savings inspiration or additional assistance. It is beyond your finance’s security level or the amount of money you save.

Automating your savings plan is one of the best savings strategies. You will need to make your savings process a consistent priority and track your savings growth level. The majority of people spend eight years starting their savings plan, and many have empty savings accounts. Here are the steps to help you automate your savings.

Savings is much more complicated than it seems

The world would be different if we all had money saved. But unfortunately, for most, savings is just an idealization of something in the future. With day-to-day expenses, economic crises, and lack of administration, savings are the last priority. And there is the main problem. Many of us know that we should not save what is left over after spending but spend what is left over after savings.

You should not save what is left over after spending but spend what is left over after savings.

But very few people carry it out because manually, we are challenging our discipline every month. The problem is that our willpower can be easily lost when we see an offer, when we pass the cups, when we fall into social pressure, or entirely when we want to satisfy a desire instead of waiting for it later immediately.

The problem is that our willpower can easily be lost.

The easiest way to save is, automatically

Fortunately, we know that an effective way to achieve your goals is to stop trusting you and designing systems to achieve what you want. In the world of personal finance, this is called “automating your savings” or “recurring savings,” and it is increasingly simple to do. The magic is that once you configure the system (be it your bank’s app, through a web portal, or directly in a branch), you will not have to try to save.

The savings will be automatic. The only effort that must be made will be to live with a little less, but the human being knows how to adapt, and in a short time, you will not even notice that you lack what you spend on savings. You will see that it is possible to be happy with less, you will get used to new life habits, and you can gradually increase your savings.

The savings will be automatic. The only effort that must be made will be to live with a little less, but the human being knows how to adapt, and in a short time, you will not even notice that you lack what you spend on savings.

Fortunately, in Dear Money, we have many articles on savings, and we publish ideas daily on our Facebook and Instagram. So, there are no excuses to learn to spend a little less.

Other ways to automate your savings

Use tools for automatic savings

The market offered modern ways to save money by introducing the latest versions of money-savings apps and tools in the past. For example, round-up apps automatically save spare variations by rounding up the daily purchase amount. Your savings account will automatically have a 75% amount on purchase of 5.25 dollars with this app.

Everyone has financial savings goals, and they need solutions, both short- and long-term. Several reliable automated savings apps can help you find savings solutions and types of accounts. You can save $5.60 by using fintech tools such as Stash and Acorns.

Check your savings progress

Don’t forget to track your paid-off debt, as it will keep your savings process organized. For this, you can use reliable tools to track your savings progress without checking your balances. It is better to use personalized savings tools such as a spreadsheet. Suppose you need to note dates, pending contributions, and savings, set up Google sheet or Excel file columns. You will add the saved amount to the savings column from the pending column.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Essential Insights on Workplace Accidents in Texas

Workplace accidents in Texas claimed 557 lives in 2024 and injured over 200,000 workers, making the state the deadliest in the nation for occupational fatalities despite having a smaller population than California. These devastating incidents affect every industry from construction sites to corporate offices, with transportation accidents causing 242 deaths and construction claiming 130 lives last year alone.

As the founder of Complete Controller, I’ve spent two decades helping Texas businesses navigate complex compliance and risk management challenges. I’ve witnessed firsthand how a single overlooked safety protocol can trigger cascading financial disasters—much like unchecked bookkeeping errors that spiral into IRS audits. This guide breaks down the alarming statistics, reveals hidden accident patterns, and provides proven prevention strategies that have saved my clients millions in workers’ compensation claims. You’ll discover how to spot early warning signs, implement cost-effective safety measures, and transform workplace culture to protect both your team and your bottom line.

What are the essential insights on workplace accidents in Texas?

Workplace accidents in Texas resulted in 557 deaths in 2024 and over 200,000 nonfatal injuries, with construction (130 fatalities) and transportation (242 fatalities) leading the statistics

Falls, slips, and trips caused 77 deaths, while struck-by incidents resulted in 91 fatalities, representing the most common accident types across industries

Texas’s non-mandatory workers’ compensation system leaves many employees vulnerable, though OSHA standards still require safety training and hazard reporting

Effective prevention programs yield $4-$6 return for every $1 invested in safety, reducing injury rates by up to 9.4% within four years

Overnight truck crashes between midnight and 6 a.m. account for 26-30% of all fatal trucking accidents in the state, highlighting critical fatigue risks

Texas Leads the Nation: Shocking Statistics on Workplace Accidents

Texas consistently maintains its position as America’s most dangerous state for workers, with workplace accidents in Texas reaching unprecedented levels. The 2024 data from the U.S. Bureau of Labor Statistics reveals 557 fatal occupational injuries—far exceeding any other state despite California’s larger workforce. This represents a fatality rate of 3.5 per 100,000 workers, significantly above the national average.

The human toll extends beyond fatalities. Approximately 200,000 nonfatal workplace injuries occurred in Texas during 2022, disrupting lives and livelihoods across the state. While nonfatal injury rates show slight declines, the death toll continues climbing in high-risk sectors, driven by Texas’s booming infrastructure development and expanding logistics networks.

High-risk industries for fatal workplace accidents in Texas

The construction industry bears the heaviest burden with 130 fatalities in 2024, primarily from falls and equipment-related incidents. Dallas’s construction boom particularly amplifies these risks, as rushed timelines and inadequate training create perfect conditions for tragedy.

Transportation and material moving occupations suffered even greater losses with 242 deaths, including a disturbing pattern of overnight truck crashes. Manufacturing facilities recorded 34 fatalities, while healthcare settings—often perceived as safe environments—experienced 8 deaths from overexertion and workplace violence.

Construction: Falls from scaffolding, electrocutions, and equipment strikes

Transportation: Vehicle crashes, loading dock incidents, and forklift accidents

Oil and Gas: Explosions, toxic exposures, and drilling equipment failures

Agriculture: Machinery entanglements, heat stress, and animal-related injuries

Common Causes of Workplace Accidents in Texas and How to Spot Them Early

Understanding accident patterns empowers prevention. Falls, slips, and trips remain the leading cause of workplace accidents in Texas, accounting for approximately 20% of all injuries. Contact with objects or equipment follows closely, representing 26.2 incidents per 10,000 workers. These seemingly mundane hazards hide in plain sight—wet floors without warning signs, cluttered walkways, and improperly stored materials.

Overexertion injuries plague every industry, from warehouse workers lifting heavy packages to nurses transferring patients. The warning signs appear gradually: employees rubbing sore backs, requesting frequent breaks, or modifying their work techniques to avoid certain movements. Smart employers recognize these signals before they escalate into workers’ compensation claims.

Preventing slip, trip, and fall injuries in Texas workplaces

Effective fall prevention requires systematic vigilance. Monthly workplace inspections identify hazards before accidents occur. Installing proper lighting in stairwells, maintaining three-point contact on ladders, and immediately cleaning spills reduce fall risks dramatically.

Non-slip flooring materials and highly visible warning signs create safer environments. Training programs that use hands-on demonstrations—practicing with actual scaffolds rather than watching videos—improve safety compliance by 16 points according to recent studies. Regular equipment maintenance, particularly for ladders and elevated platforms, prevents deterioration that leads to catastrophic failures.

Struck-by hazards: Texas construction and trucking risks

Construction sites and highways present unique struck-by dangers. In 2020 alone, work zones claimed 186 lives across Texas highways. Implementing comprehensive traffic control plans (TCP/ITCP) creates protective barriers between workers and vehicles. Tethering tools prevents dropped objects from becoming deadly projectiles, while designated crane operation zones keep ground workers safe from swinging loads.

High-visibility clothing, properly maintained equipment guards, and clear communication protocols form the foundation of struck-by prevention. Training workers to maintain situational awareness—constantly scanning for overhead work, moving equipment, and unstable materials—transforms passive victims into active safety participants.

Real-World Case Study: Fatigue-Driven Truck Crashes in Texas

The darkness between midnight and 6 a.m. conceals a deadly secret on Texas highways. During these hours in 2025, at least 96 fatal truck crashes killed 103 people and seriously injured over 200 more. This represents a devastating trend—214 overnight fatalities in 2023, 227 in 2022, all occurring when driver alertness reaches its lowest point.

Despite these alarming statistics, the Federal Motor Carrier Safety Administration rated many involved trucking companies as “satisfactory,” exposing dangerous gaps in oversight. TxDOT and NHTSA data reveals overnight crashes jumped from 109 fatalities in 2023 to 115 in 2024, with smaller, under-monitored firms contributing disproportionately to the carnage.

The solution requires both technology and accountability. Mandatory electronic logging devices track hours-of-service compliance, while AI-powered fatigue monitoring systems detect drowsy driving patterns. Companies implementing these technologies alongside strict rest requirements could prevent 30% of overnight crashes. Yet underreporting continues masking the crisis’s true scope, allowing dangerous operators to evade scrutiny while families mourn preventable losses.

One accident can cost more than prevention—get ahead with Complete Controller.

Texas Laws and Workers’ Rights After Workplace Accidents

Texas’s unique non-subscriber workers’ compensation system creates a complex legal landscape for workplace accidents in Texas. Unlike most states, Texas allows employers to opt out of traditional workers’ compensation insurance, leaving approximately 20% of workers without automatic coverage for workplace injuries.

For covered employees, the Texas Department of Insurance Division of Workers’ Compensation (DWC) oversees claims processing, medical care authorization, and dispute resolution. Benefits include full medical treatment, temporary income benefits at 70% of average weekly wage, and permanent disability compensation when applicable. Federal OSHA standards still apply regardless of workers’ comp status, mandating safety training, hazard communication, and personal protective equipment.

Navigating claims for workplace injuries in Texas

Time sensitivity defines successful claims. Report injuries immediately to supervisors—Texas law requires notification within 30 days. Document everything: photograph hazards, collect witness statements, and maintain copies of all medical records. File DWC claims promptly through your employer’s insurance carrier or directly if they’re a non-subscriber.

Non-subscriber employees retain the right to sue employers for negligence, potentially recovering full damages including pain and suffering. However, they must prove employer fault—a higher bar than workers’ comp claims. Safety-conscious companies like those following Chambers County’s progressive discipline model experience fewer violations and claims, protecting both workers and business interests through proactive prevention rather than reactive litigation.

Prevention Strategies: Building a Safer Texas Workplace

Proactive safety management transforms workplace culture and dramatically reduces accidents. Texas Department of Insurance guides emphasize management commitment as the cornerstone—when leadership models safety behaviors, employees follow. Successful programs integrate safety into daily operations rather than treating it as an add-on compliance burden.

Job Safety Analyses (JSAs) break down tasks to identify hazards before work begins. Monthly inspections catch deteriorating conditions early. Even office environments benefit from attention to detail: mirrors at hallway corners prevent collisions, ergonomic assessments reduce repetitive strain injuries, and clear evacuation routes save lives during emergencies.

The financial argument proves compelling—OSHA research demonstrates $4-$6 returns for every dollar invested in safety programs. A Central Texas construction company avoided $50,000+ in potential OSHA fines through comprehensive training and monthly inspections, while simultaneously improving employee morale and productivity.

Step-by-step injury and illness prevention plan for Texas businesses

Establish Leadership Commitment

Create a written safety policy signed by top management. Allocate budget for safety equipment, training, and program administration. Designate safety coordinators with clear authority to halt unsafe work.

Conduct Comprehensive Training

Develop role-specific safety curricula covering equipment operation, hazard recognition, and emergency procedures. Use hands-on training methods—studies show practical demonstrations improve retention by 7.7 points over classroom-only instruction. Schedule refresher training quarterly and immediately after incidents.

Implement Systematic Inspections

Create detailed inspection checklists tailored to your workplace hazards. Conduct monthly walkthroughs with rotating team members to maintain fresh perspectives. Document findings, assign corrective actions with deadlines, and track completion rates.

Investigate All Incidents

Analyze near-misses alongside actual injuries—they’re free lessons in prevention. Use root cause analysis to identify systemic issues beyond immediate causes. Share findings transparently to prevent recurrence.

Measure and Improve

Track injury rates, lost workdays, and workers’ comp costs monthly. Celebrate safety milestones publicly. Adjust programs based on data trends and employee feedback. Regular reviews keep safety initiatives relevant and effective.

From my experience at Complete Controller, integrating safety metrics into financial dashboards creates accountability. When executives see safety performance alongside revenue figures, prevention becomes a business priority rather than a compliance checkbox.

The Financial and Human Cost of Workplace Accidents in Texas

Workplace accidents in Texas drain billions from the state economy through medical expenses, lost productivity, and legal costs. Construction firms face the steepest burden, with workplace injuries projected to affect 2.6 million U.S. workers in 2026. Each serious injury averages $42,000 in direct costs, while fatalities exceed $1.2 million when including indirect expenses like hiring, training replacements, and reputation damage.

Beyond dollars, families endure immeasurable suffering. Permanent disabilities alter life trajectories, forcing career changes and straining relationships. Children lose parents, spouses become caregivers, and communities lose valuable contributors. OSHA violations compound financial pain with fines reaching $15,000 per citation for serious violations.

Cost breakdown and ROI of safety investments

Smart safety spending generates remarkable returns. Harvard Business School research reveals companies undergoing OSHA inspections experienced 9.4% fewer injuries over four years, saving an average of $355,000 in claims and compensation costs. My firm’s clients consistently see 25% workers’ comp premium reductions after implementing comprehensive safety audits.

Prevention costs pale compared to accident expenses:

Basic PPE: $100-300 per worker annually

Safety training: $500-1,000 per employee

Monthly inspections: 2-4 management hours

Accident aftermath: $42,000+ direct costs, immeasurable human suffering

Conclusion

Workplace accidents in Texas demand immediate action from every employer and worker. With 557 deaths in 2024 and rising overnight trucking fatalities, the status quo kills. Yet proven solutions exist—from fall prevention training that measurably improves behavior to inspection programs that slash injury rates by nearly 10%.

As Complete Controller’s founder, I’ve guided hundreds of Texas businesses through risk management transformations. Just as proper bookkeeping prevents tax disasters, systematic safety management prevents human tragedies while boosting profitability. The companies thriving tomorrow will be those investing in comprehensive prevention today.

Your team’s safety and your business’s future depend on the decisions you make now. Ready to protect both? Contact the experts at Complete Controller for integrated financial and risk management guidance that safeguards your most valuable assets—your people.

Frequently Asked Questions About Workplace Accidents in Texas

Which industry has the highest rate of workplace injuries in Texas?

Transportation and material moving leads Texas workplace fatalities with 242 deaths in 2024, while construction follows with 130 fatalities, primarily from falls and equipment-related incidents.

How many workplace accidents happen in Texas each year?

Texas experienced over 200,000 nonfatal workplace injuries in 2022, plus 557 workplace fatalities in 2024—maintaining the highest death toll of any U.S. state.

What are common causes of workplace accidents in Texas?

Falls, slips, and trips cause approximately 20% of injuries, overexertion affects 26.2 per 10,000 workers, struck-by incidents claim 91 lives annually, and overnight truck driver fatigue contributes to 26-30% of fatal trucking crashes.

What should I do after a workplace injury in Texas?

Report the injury to your supervisor immediately (within 30 days required), seek medical treatment, document the incident with photos and witness statements, and file a workers’ compensation claim through DWC if covered or consult an attorney if your employer is a non-subscriber.

How can Texas employers prevent workplace accidents?

Implement monthly safety inspections, provide hands-on safety training, enforce PPE requirements, conduct Job Safety Analyses before tasks, maintain equipment properly, and build comprehensive injury prevention programs following TDI and OSHA guidelines.

U.S. Department of Labor. (2024). Business Case for Safety and Health – Benefits. Occupational Safety and Health Administration (OSHA). https://www.osha.gov/businesscase/benefits

Harvard Business School. (May 18, 2012). Randomized Government Safety Inspections Reduce Worker Injuries with No Detectable Job Loss. Levine, D. I., Toffel, M. W., & Johnson, M. S. Science, Vol. 336, No. 6083, pp. 907-911. https://www.hbs.edu/news/releases/Pages/toffelscience051712.aspx

Unlocking Digital Transformation Integration for Success

Digital transformation integration is the disciplined process of weaving digital technologies, data, and workflows into every part of your business so systems talk to each other, teams work from one source of truth, and you unlock measurable gains in efficiency, customer experience, and growth. This comprehensive approach goes beyond simply adopting new tools—it requires redesigning how your organization operates end-to-end so cloud platforms, automation, AI, and analytics become embedded into daily work rather than existing as disconnected projects.

As the founder of Complete Controller, I’ve spent two decades moving companies from paper, spreadsheets, and disconnected apps into integrated, cloud-based operations. The hard part is never the technology—it’s aligning processes, people, and platforms so the finance stack, operations, and customer experience transform together. When done right, organizations with strong integration achieve 10.3 times higher ROI compared to only 3.7 times for those with poor integration. This article will show you how to build a practical integration roadmap that works in the real world, for real teams and budgets, helping you avoid the $2.3 trillion annually wasted on failed transformations globally.

What is digital transformation integration and how do you get it right?

Digital transformation integration is the end-to-end alignment of technologies, data, processes, and people so your business operates as a unified digital system, consistently delivering better efficiency, decisions, and customer value.

It goes beyond one-off automation projects to rewire how value is created, using cloud, AI, analytics, and connected platforms across the organization.

Getting it right requires a clear strategy tied to business outcomes, an integration architecture (APIs, data, workflows), and strong change management so people actually adopt new ways of working.

Mid-market and SMB leaders must prioritize use cases with visible ROI, start small with high-impact pilots, and scale only after processes and governance are proven.

The most successful transformations combine people-first change practices with disciplined technology integration, building internal capability instead of one-time projects.

Defining Digital Transformation Integration for Today’s Business Reality

Digital transformation integration represents the deliberate integration of digital technologies into existing business models and processes so organizations can continuously create value, not just modernize legacy systems. With global spending on digital transformation set to reach nearly $4 trillion by 2027, growing at 16.2% annually, the scale and urgency of integration have never been clearer.

The COVID-19 pandemic accelerated digital transformation timelines by an average of six years, compressing what companies had planned over half a decade into mere months. Today, over 90% of organizations have adopted cloud technologies—the highest adoption rate of any emerging technology—making integration around these platforms the central challenge.

Core components of integrated digital transformation strategy

Strategy and business model alignment means transforming how you create and capture value, not just digitizing existing workflows. This fundamental shift separates true transformation from surface-level changes.

Technology stack and architecture brings cloud, SaaS, APIs, data platforms, and automation tools together as a coherent ecosystem. The goal is seamless data flow across all business functions.

Data and analytics integration centralizes and standardizes information so decision-makers use real-time, reliable insights. Organizations that break down data silos save an average of $7.8 million annually in lost productivity.

People, culture, and change enablement embeds new behaviors, skills, and governance so change sticks. Organizations investing heavily in culture change see 5.3 times higher success rates than those focusing only on technology.

Digital transformation vs. digitization vs. digitalization

Digitization converts analog information into digital form—think paper documents becoming PDFs. This basic step forms the foundation but delivers minimal strategic value alone.

Digitalization uses digitized data to improve specific processes through e-signatures, online forms, or automated workflows. These improvements streamline individual tasks but often create new silos.

Digital transformation integration reimagines and integrates entire value chains using digital capabilities across the organization. This holistic approach creates competitive advantages that individual improvements cannot match.

Why Integrated Digital Transformation Drives Competitive Advantage

When executed as an integrated effort, digital transformation significantly improves productivity, profitability, and long-term enterprise value. Digital leaders consistently outpace laggards in both shareholder returns and revenue growth by double-digit margins.

Proven business benefits from integrated initiatives

Higher growth and returns materialize when systems work together seamlessly. Companies achieving true integration report 10.3 times ROI versus 3.7 times for those with fragmented approaches.

Operational efficiency and cost reduction come from automation, cloud services, and optimized workflows that reduce overhead while increasing throughput. Manufacturing and financial services lead this investment wave.

Customer experience and loyalty improve through omnichannel, personalized, 24/7 experiences that drive satisfaction and retention. Nike’s digital transformation demonstrates this perfectly—their shift to direct-to-consumer integrated e-commerce, mobile apps, and physical stores, resulting in 14% sales growth.

Agility and resilience allow integrated digital operations to respond faster to market shifts, supply chain shocks, and new competitors. Real-time data visibility enables proactive rather than reactive decisions.

The cost of fragmented or siloed digital efforts

Disconnected tools create data silos, duplicate work, and inconsistent reporting, often worsening complexity instead of reducing it. Employees waste 12 hours per week searching for information across disconnected systems, while customer service response times increase by 43%.

Point solutions without integration lead to shadow IT, security gaps, and staff fatigue from constant context-switching. From my own client work at Complete Controller, these “random acts of digital” consume budgets without moving the metrics CEOs and CFOs actually care about—margin, cash flow, and customer lifetime value.

Struggling with disconnected systems? See how Complete Controller helps integrate your operations.

Where Most Digital Transformation Integrations Fail (and How to Avoid It)

Despite massive investments, 70% of digital transformation projects fail to meet their goals. Failed efforts cost organizations $2.3 trillion annually worldwide—a staggering figure reflecting wasted budgets, lost productivity, and missed growth opportunities.

Common failure patterns in digital transformation projects

Tech-first, strategy-second approaches implement tools without clear use cases or success metrics. Organizations get excited about AI or automation without defining what business problems these technologies will solve.

Underestimating people and change assumes training alone suffices, ignoring adoption incentives and culture shifts. Even the best technology fails when people resist using it.

Lack of integration architecture creates environments with no API strategy, inconsistent data models, and manual “swivel-chair” integration between systems. Nearly 77% of organizations rate their data quality as average or worse—an 11-point decline from 2023.

Trying to “do it all at once” leads to over-scoped programs that overwhelm teams and stall before value is realized. Budget overruns affect 47% of ERP implementations, showing how complexity creates financial pressure.

People-first integration: lessons from transformation case studies

Successful organizations like Mateco and UKG achieved scale by combining project management with structured change management using the ADKAR model and champions programs. Their outcomes included 85% global alignment, 30% less admin time, and thousands of users successfully onboarded.

The key takeaway: successful integrations treat change management as part of the work, not a side activity. Leadership changes during transformation affect nearly 70% of organizations, making stable change practices even more critical.

A Practical Roadmap for Digital Transformation Integration (Built for SMBs and Mid-Market)

This roadmap provides actionable steps for leaders who cannot afford multi-year, multimillion-dollar experiments. Small wins build momentum while reducing risk.

Step 1 – Clarify business outcomes before choosing tools

Define three to five measurable goals such as reducing month-end close time by 40%, cutting order cycle time by 25%, or increasing NPS by 10 points. Map how these outcomes connect to revenue, cost, and risk—the metrics executives prioritize.

From my experience at Complete Controller, transformations starting with “we need AI” fail, while those beginning with “we need faster, more accurate visibility into cash and customers” succeed. Business bookkeeping essentials often reveal the specific pain points worth addressing first.

Step 2 – Map current processes, systems, and data flows

Document how work really happens today across finance, operations, sales, and customer service. Identify integration choke points: duplicate data entry, spreadsheets bridging systems, and manual reconciliations.

Create a simple systems and data map to visualize where APIs or middleware will create the most leverage. Moving from spreadsheets to CRMs often represents a crucial first integration point for growing businesses.

Step 3 – Design your integration architecture

Choose a cloud-first core (ERP, CRM, financials, HR) that becomes the “source of truth.” Define how supporting tools (billing, support desk, e-commerce, marketing, payroll) will connect through APIs or iPaaS platforms.

Standardize common data definitions (customer, invoice, project, item) to avoid inconsistent reporting. McKinsey’s digital transformation strategy framework emphasizes this architectural foundation as critical for long-term success.

Step 4 – Pilot, then scale in 90-day waves

Start with one high-impact, cross-functional use case—integrating CRM, billing, and bookkeeping to eliminate revenue leakage works well. Run a 90-day cycle: configure, test, train, measure impact, fix issues, then scale.

Use each wave to build internal capability—process owners, power users, and basic analytics skills. This iterative approach reduces risk while building confidence and competence across your team.

Step 5 – Govern, measure, and continuously improve

Establish a small digital steering group (CFO, COO, IT/ops, a front-line leader) to own priorities and tradeoffs. Track a slim set of KPIs: cycle times, error rates, customer satisfaction, employee adoption, and ROI.

Embed continuous improvement through quarterly reviews to retire obsolete tools, refine automations, and realign with strategy. Following the NIST Cybersecurity Framework helps maintain security standards throughout this evolution.

How Integrated Transformation Changes Finance, Operations, and Customer Experience

Integrated transformation becomes real when concrete changes appear in daily team operations. The impact spans every business function when properly executed.

Finance and bookkeeping: from reactive to real-time

Cloud financial systems plus integrated bank feeds plus automated workflows deliver near real-time books instead of month-old reports. Integration with CRM, billing, and inventory creates end-to-end visibility into revenue, margin, and cash flow—a core promise of Complete Controller’s model.

In my own practice, integrating client systems typically reduces manual bookkeeping labor by 30-50% and dramatically cuts error risk, freeing time for advisory work. This shift transforms finance from backward-looking reporting to forward-looking strategic partnership.

Operations and supply chain: connected, data-driven decisions

Manufacturers and distributors use IoT, ERP, and analytics integrations to cut downtime, improve forecasting, and optimize inventory. GE Power’s transformation exemplifies this approach—they integrated IoT sensors from 900+ global sites, streaming 500,000 data records per second to AWS cloud platforms.

Processing 20 billion machine-data records daily through predictive analytics, GE reduced problem resolution from days to same-day fixes. They helped customers avoid 80% of unplanned downtime, saving millions per incident while opening new software revenue streams.

Customer and employee experience: seamless, omnichannel journeys

Digital transformation enables engagement across channels (web, mobile, social, chatbots) while pulling data into unified profiles. DBS Bank, Nike, and IKEA reimagined their models around digital channels, cloud data, and APIs to deliver frictionless experiences.

These companies demonstrate how integration creates consistency—customers enjoy the same personalized experience whether shopping online, using mobile apps, or visiting physical locations. Employee productivity soars when systems work together seamlessly.

Building Trust, Compliance, and Risk Management into Digital Integration

Integrated digital systems must be secure, compliant, and resilient from the start—especially when financial and customer data are involved. Remote work security post-COVID has made this even more critical.

Security, privacy, and regulatory considerations

New regulations and customer expectations make data protection and privacy central to digital strategies. Cloud platforms and SaaS tools offer strong security capabilities, but integration points (APIs, data exports) introduce risk if not governed properly.

Finance-related transformations must consider tax, audit, and industry-specific regulations when redesigning workflows. The complexity increases with multi-jurisdiction operations, making expert guidance essential.

Governance structures that keep integrated systems safe and reliable

Define who owns which data, which systems are “systems of record,” and how changes get approved. Implement role-based access, audit trails, and standardized backup and recovery policies across integrated platforms.

From my own practice, clear governance prevents “tool sprawl” and protects clients from well-intentioned but risky shortcuts like unsanctioned spreadsheets or exports. Regular security audits and compliance reviews become non-negotiable.

The Human Side of Digital Transformation Integration

Technology only delivers value when people adopt and embrace new ways of working. Culture change multiplies success rates by 5.3 times compared to technology-only approaches.

Change management and culture as success multipliers

Activating sponsors, training leaders, and building change champions dramatically increases adoption and project success rates. Organizations that integrate project and change management report higher satisfaction and more sustainable transformation outcomes.

Leadership stability matters—nearly 70% of organizations experience top team changes during transformation. Supporting leaders through this transition prevents momentum loss and maintains vision alignment.

Practical tactics I use with clients to drive adoption

Involve end-users in process mapping and tool selection to reduce resistance

Pilot with high-credibility teams, gather feedback, and showcase their wins to build momentum

Align incentives by rewarding teams for using dashboards and integrated data in decision-making, not just hitting output targets

Create “super users” who become internal champions and trainers

Celebrate small wins publicly to maintain enthusiasm and demonstrate progress

Turning Integration into a Strategic Advantage

Digital transformation integration rewires how your business creates value—connecting systems, data, and teams so you can move faster, decide smarter, and serve customers better. When you align a clear strategy, thoughtful integration architecture, and people-first approach to change, transformation becomes less about technology projects and more about building a stronger, more resilient company.

As the founder of Complete Controller, I’ve watched businesses stall for years because their data and systems stayed fragmented. I’ve also seen those same businesses unlock growth and peace of mind once their financial and operational stacks were properly integrated. The difference between the 70% that fail and the 30% that succeed comes down to treating integration as the heart of transformation, not an afterthought. If you’re ready to move from scattered tools to a truly integrated digital backbone, visit Complete Controller to explore how our team can help design and operate that transformation with you.

Frequently Asked Questions About Digital Transformation Integration

What is digital transformation integration?

Digital transformation integration is the coordinated process of integrating digital technologies, data, and workflows across all areas of a business to improve operations, customer experience, and value creation—not just implementing isolated tools. It creates a unified system where all parts work together seamlessly.

Why is digital transformation important for businesses today?

Digital transformation helps organizations keep up with changing customer expectations, competitive pressures, and technological advances by modernizing operations, enabling innovation, and improving efficiency and resilience. With $4 trillion in global spending by 2027, companies that don’t transform risk becoming obsolete.

What are some examples of successful digital transformation?

Examples include GE’s industrial IoT platform reducing equipment downtime by 80%, DBS Bank’s cloud-based digital banking winning global awards, and Nike’s integrated e-commerce and mobile app strategy driving 14% sales growth through personalized customer experiences.

What are the key benefits of digital transformation initiatives?

Benefits include reduced operational costs (saving millions in productivity), improved efficiency (30-50% reduction in manual work), better customer experiences (43% faster response times), new revenue streams, data-driven decision-making, and 10.3x higher ROI for well-integrated transformations.

How can small and mid-sized businesses get started with digital transformation integration?

SMBs should begin by defining clear business outcomes, mapping current processes and systems, choosing a cloud-first core platform, piloting one high-impact integrated use case, and building internal capabilities and governance as they scale. Starting small with 90-day pilots reduces risk while proving value.

Thales. “The Benefits of Digital Transformation.” Thales Group, 2023.

Whatfix. “21 Examples of Digital Transformation Case Studies (2025).” Whatfix Blog, 2025.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

New trends are rolled out in marketing every year as technology and innovation growth and the audiences for products and services change. Those in the marketing industry need to know the trends for the current year and the next year. These marketing professionals also have to keep their fingers on the pulse of the here and now. Here are six marketing trends currently dominating the marketing industry.

Conversational marketing

Across the digital marketing spectrum, conversational marketing may become an industry standard in the current year and be here to stay for years to come. In real-time, such marketing is the best way to attract clients rather than wait for a reply from the targeted audience. You can also experience all this in the live chat support and phone as experts predict conventional marketing will be AI-powered this year.

Advertisement over-the-top (OTT)

According to the major brands, hyper-targeting and integrating associated TV into digital techniques can replace traditional ad purchases. You will have much more return on investment due to traditional TV versus OTT campaign attribution. That’s why experts consider this year the start of a dramatic shift in using this marketing strategy.

Marketing via voice search

Smart speakers or digital home assistance are becoming more and more commonplace. The market is flooded with voice search devices such as Apple’s Homepod, Alexa, Amazon, Echo, Google Dot, etc. These smart devices have made searching far easier and hands-free.

In 2016, around 40% of adults used voice search on a daily average. With time, this technology usage is increasing fast over time and is becoming more intuitive and reliable. Various brands are increasing their sales by incorporating voice search.

On-go searching ability and voice search have made online search queries have become more specific to a great extent. That’s why people consider targeting long-tail queries as the tip of the iceberg. Natural-language searching for ages as Google has been making its algorithm for the latest search engine page result’s report. Keep an eye on the Hummingbird update and Rankbin announcement to get clues on Google’s work.

Customized marketing

In customized marketing, marketers provide an individualized user experience by targeting each web user or email list subscribers. According to the research of the Salesforce report, around 96% of customers prefer customized marketing relationships for branding. According to Broadridge, Around 80% of people shop more for a product due to customized service or experience. Digitalization transforms marketing trends to boost businesses.

All consumers don’t hesitate to receive a customized experience and submitting their personalized data in return as it increases their privacy and security concerns. Consumer data sharing helps them in gaining customized experience and benefits, including the younger generation.

Various online platforms use customized marketing campaigns such as Netflix, Amazon, Pinterest without mentioning Facebook and Google. In this way, they identify what their clients like or dislike and their search history. Also, customers get suggestions for similar products that you even think to purchase.

Influencer and video marketing

When people talk about video marketing, the first thinking comes in their mind is about YouTube. But multiple social media platforms use video marketing like Instagram, Facebook, LinkedIn, and Snapchat. Keep your videos on such channels precise, concise, and short.

People love to share, like, and comment on such videos on other social media websites. If your platform’s influencer is famous and their hats in the ring, audience interest in your videos will be more substantial. Industry leaders help your brand name in making progress fast. If you want to know your targeted audience, find their location, and get to work.

Conclusion

This year, there is an excessive demand for information and items, including AI-powered customization, new content kinds, and advanced segmentation. There are other latest technologies that marketers are going to incorporate into their businesses.

In the marketing sector, new technological advances have remarkable potential. Only you must know the correct way to use them for your benefit. There is fierce competition across your industry, as many businesses are fighting. You will need to learn the latest techniques to win the competition and make your business more competitive.

Revise your current marketing strategy and change it as per the requirement of your audience if your branding relies on video and customized marketing. Keep an eye on the latest digital marketing trends to know how to keep your business ahead of the game.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Workplace burnout and stress are modern ailments that many people face despite having support systems and positive work environments. With the fast pace of modern life and the increasing demand for task efficiency and a healthy work-life balance, it can be a real struggle for people to keep their heads above water at times.

Burnout is defined “as a long-term consequence of adverse working conditions characterized by the simultaneous experience of the symptoms of exhaustion and disengagement from one’s job.” It is especially important to deal with workplace burnout as early as possible if one works in caregiving or other intense medical professions, such as psychiatry. Here are four ways to avoid workplace burnout and stress.

Identify the Sources of Burnout or Stress

Burnout may result from unrelenting stress and cause individuals to be disengaged with their work and deplete motivation, leading to depression. On the other hand, stress can lead to hypertension, emotional distress, and, if left untreated for longer periods, detrimental to a person’s confidence, contentment, and even physical well-being.

Identifying stress can be challenging. It is an abnormal amount of pressure exerted on you that can trigger a response from your body. An example of something that can trigger this is perhaps an increased workload, inability to meet deadline expectations, or simply having a perfectionist attitude about your work.

Take a Break from the Workplace

It’s okay to be out of your comfort zone every once in a while and absolutely to feel some levels of stress sometimes, but when it becomes consistent and is affecting you physically, there might be signs of serious trouble. Physical signs of stress include having chest pain, nausea, muscle tension, excessive breathing, loss of appetite, breathing problems, and fatigue.

These physical issues can lead to psychological and emotional issues, affecting both your personal and professional life. You must detach yourself from work from time to time and have an honest conversation with yourself. If you feel any of these symptoms, regardless of their severity, you should seek professional help and reach out to friends and family to help heal.

Practice Self-Care

The rapid development of technology has helped create awareness about mental health and led to new approaches to fighting burnout and stress. These approaches put the responsibility squarely on the individual and encourage them to be more mindful of their own resources and environment and take care of themselves. One of the core strategies to fight and prevent stress is self-care.

Self-care varies from person to person and can be as simple as having a cup of your favorite herbal tea to something more structured such as joining a weekly yoga or Pilates class.

The purpose of self-care is to mitigate the effects of workplace negativity, exhaustion, and stress to carve out a niche of time where one prioritizes oneself, as put forward by a November 2020 VeryWellMind article, ‘Why self-care can help you manage Stress.’

One should treat themselves to spa-like experiences to jog their senses and give them relief from a high-stress environment. All of these strategies can come together to allow individuals some time to self-reflect in a comfortable situation. These minor activities can go a long way in mitigating the damaging effects of workplace burnout and stress in the long run.

Address Workplace Issues and the Environment

It’s also important to address the issues you face at work and confront your problems at the source. If it’s an individual causing the stress, whether it be your supervisor or a colleague, then try approaching them and having an open conversation where you voice your concerns or issues.

Admitting you have problems is not a sign of weakness. Having an open and healthy conversation with members of your company can go a long way toward helping you manage your stress and developing your communication and soft skills.

If a particular assignment or client affects your work experience, try raising your concerns with upper management and letting them know how you feel. See if there is any way to help resolve your issues without having a confrontation.

Your workplace directly impacts your mental and physical health. It would help if you were situated in an environment where you can have an open relationship with your colleagues and supervisors and are treated with dignity and respect.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud-hosted desktop where their entire team and tax accountant may access the QuickBooks™️ file, critical financial documents, and back-office tools in an efficient and secure environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

The publishing world has massively changed over the last decade since companies will allow any author to self-publish for free or for a nominal fee. This ability to self-publish offers authors a unique opportunity to be published and make a career of writing what they want to write.

Self-publishing isn’t putting traditional publishing companies out of business, but it gives them a run for their money. If you are a great writer and social media savvy, you can get yourself published in a short time.

Many authors looking to publish independently are concerned with the costs. If you publish, edit, format, and design the book cover yourself. You can do it for free on platforms like Amazon or other published on-demand sites.

The cost of self-publishing a book depends on a few things:

How much of the publishing process you are going to do yourself

The length of the book and content

The prerequisites of the publishing company you are using

Most writers can count on spending between $2,000 – $4,000 on self-publishing their book, including marketing services, cover design, formatting, and editing. This cost will be cut significantly if you do all of these services yourself. However, it is suggested that you should at least hire an outside editor for the best quality.

Therefore, if you only want to get your book out there, you can always format it for free and make it available within 72 hours on Amazon, Kindle self-publishing sites, or other publish-on-demand sites. However, if you want to compete with traditionally published books, you will need to pay for editing, marketing, and design.

Editing

It would be best if you got a few different kinds of technical editing done before publishing, including proofreading, developmental editing, and copy editing. You should have an editorial assessment and work out to make critical changes to publish the best product possible.

Book Cover Design

Unless you are an artist or have skills as a graphic designer, it is suggested that you hire a professional book cover designer. Though there is the saying, “Never judge a book by its cover,” most people will explore a book further for potential purchase because of the book cover design.

The cost of having a professional cover designed can range widely with the cost depending upon the designer’s skill level.

Formatting

Depending on where you are publishing, you will need to format the book for a book and an eBook. Each format is different depending on where you are publishing the book. You can format the book yourself if you know how to do it properly.

Hiring a professional to format your book is a great idea because it can be tedious and requires knowledge and skills, so it looks right when the book is published. While formatting can be tricky, there are many videos online that show how to do it.

Marketing

One of the major disadvantages to self-publishing instead of going through a traditional publisher is that the publisher will heavily market your book. They will also set up any book signings or other promotional events and handle all websites and social media associated with you or the book.

Other Costs

Depending on your chosen path, there can be costs associated with the delivery and converting your book to an audiobook. There can also be fees that you pay to use a website to publish for you, such as a flat fee or a percentage of your royalties.

In some cases, an author will hire a ghostwriter to help them develop, edit, and publish their book. Some ghostwriters will charge by the hour, while others will charge by the project. While it can be expensive to hire a ghostwriter, it can also help you get your ideas out quickly and professionally if you aren’t a strong writer.

Conclusion

The more you invest in the development and publishing of your book, the better it will do in the market. Do the research and plan what you will do yourself and what you will hire another person to do for you in the process.

The cost to self-publish can cost anywhere between $0 to $20,000, depending on the skill level of those involved in the publishing process. If you are contemplating self-publishing, you need first to assess your budget then analyze how much work you will do yourself in the publishing process.