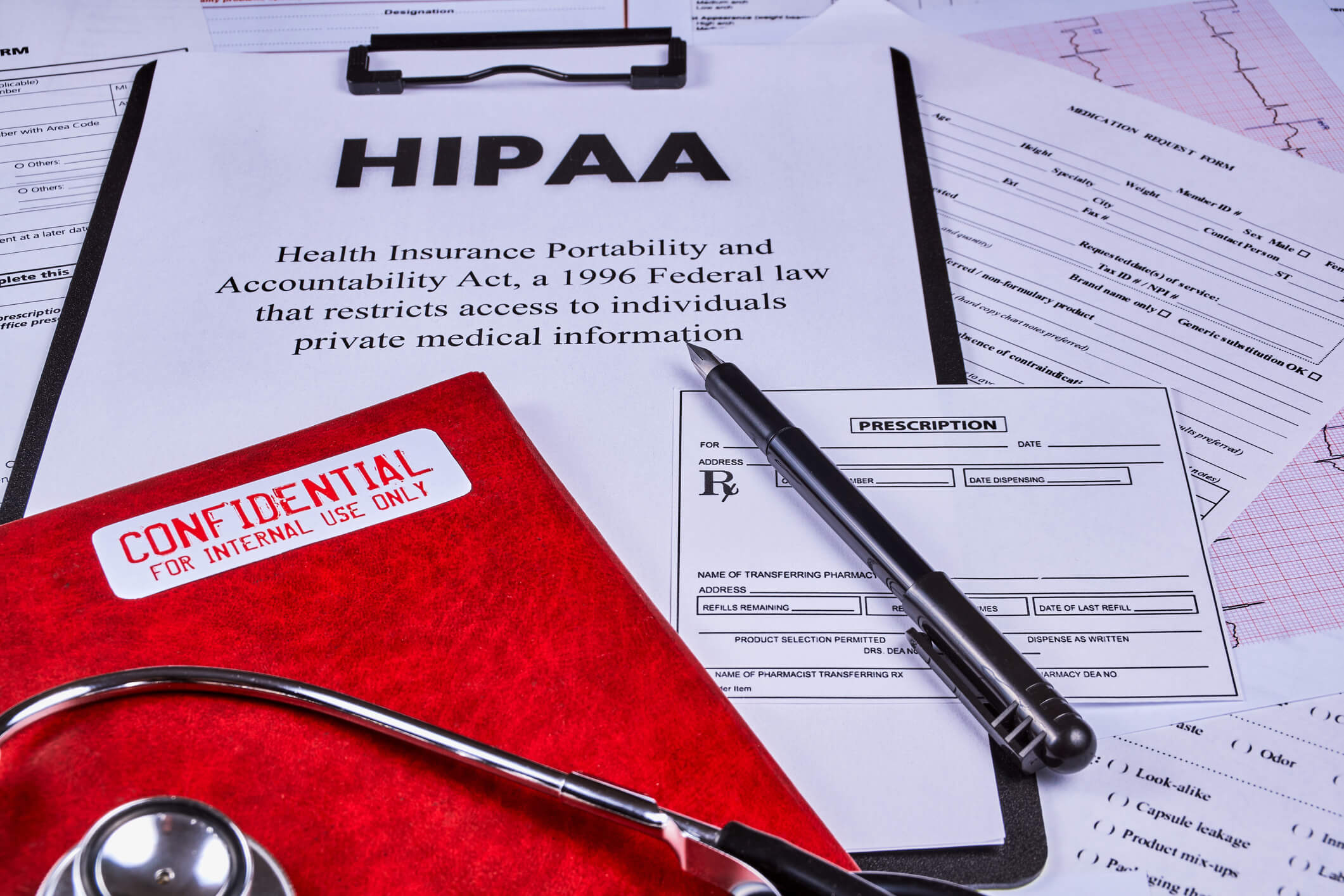

The Health Insurance Portability and Accountability Act of 1996 (HIPAA) is a legislation of the United States that ensures data security of all medical information for individuals. Today, the top healthcare organizations’ concern is compliance with HIPAA (Healthcare Insurance Portability and Accountability Act of 1996).

HIPAA rules are meant to secure protected health information (PHI), whether electronic or manual. To achieve HIPAA compliance, healthcare institutes and professionals must follow guidelines that will ensure the security and protection of their patients. If you need clarification on the rules, engage the Chief Information Security Office for review.

HIPAA Compliant – A Checklist

HIPAA rules and regulations have changed, causing healthcare organizations many challenges. Its complex language has often hindered organizations, making it hard to determine if their activities are appropriately maintained according to HIPAA compliance. Healthcare organizations must address some specific rules by HIPAA, which are as follows:

HIPAA Privacy Rule

HIPAA Security Rule

HIPAA Enforcement Rule

HIPAA Breach Notification Rule

HIPAA Privacy Rule

The HIPAA Privacy Rule ensures that an individual’s healthcare information is adequately protected, including all medical records and personal information (healthcare plans, insurance, and financial). The goal is to provide security while allowing secure access to healthcare practitioners without a patient’s authorization.

The rule is to balance the disclosure of information and protect an individual’s privacy. According to the HIPAA Privacy Rule, patients have full rights over their medical information, which means they can obtain their medical records or request a correction.

HIPAA Security Rule

The HIPAA Security Rule has set the national principles to safeguard the electronic health information of an individual as declared under the privacy rule. The Security Rule ensures the electronic PHI’s reliability, security, and confidentiality. Three types of safety measures fall under the HIPAA Security Rule: Physical protection, Technical protection, and Administrative protection.

Physical Protection

Limited Access to Facility – The organization must limit physical access to its amenities and ensure that only authorized personnel are allowed.

Workstation security is paramount; organizations must enforce stringent policies for electronic device use. Covered entities must document all hardware activities, tracking individuals responsible for data transfer or movement.

Technical Protection

Access Control is critical; organizations should permit access to electronic PHI solely for authorized personnel. Any removal from the system must undergo scrutiny, ensuring proper alteration or destruction.

Audit Control– All hardware and software activities must be recorded and examined, ensuring no data theft or misuse of the information. The organization is responsible for only authorized people having access to the information.

Administrative Protection

Security Officials are essential; organizations should appoint dedicated personnel to enforce and implement e-PHI security policies and procedures.

Training Management is imperative; organizations must educate all employees on e-PHI security measures, emphasizing the consequences of policy violations.

Assessment is pivotal; organizations must regularly evaluate security measures, ensuring strict adherence to rules, minimizing e-PHI disclosure, and granting access solely to authorized personnel.

HIPAA Enforcement Rule

The HIPAA Enforcement Rule requires all healthcare organizations to enforce the Privacy Rule. If any organization fails to comply with HIPAA, it must face penalties. There are several ways the OCR implements the Privacy and Security Rules:

Investigation of complaints

Determining whether healthcare organizations comply with HIPAA

Educate organizations and provide substitute compliance if required

HIPAA Breach Notification Rule

Any organization that allows disclosure of healthcare information without authorization, under any circumstances, will be convicted of violating HIPAA rules. The organization must notify the secretary immediately if it discovers an information breach.

Conclusion

In conclusion, HIPAA (Health Insurance Portability and Accountability Act) safeguards individuals’ medical data. For healthcare organizations, compliance is paramount, and a comprehensive checklist outlines critical rules—Privacy, Security, Enforcement, and Breach Notification. The Privacy Rule ensures confidentiality, empowering patients with control over their information. The Security Rule sets national standards, emphasizing physical, technical, and administrative protections. The Enforcement Rule mandates compliance, with penalties for non-compliance. The Breach Notification Rule demands immediate reporting of unauthorized disclosures. Adhering to these guidelines is crucial for securing patient data and maintaining the integrity of healthcare practices.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

From personal expenses to business costs, life is expensive. It may seem like you must open your wallet wherever you go. One way to save more money every year is to identify and deduct legitimate tax write-offs, which intersect your personal and business expenses.

Dental and Medical Expenses

You may be able to deduct dental and medical costs for yourself, your partner, and any dependents when the total cost exceeds ten percent of your adjusted gross earnings. In addition, when you or your spouse is 65 years old or over, you can deduct all medical costs that exceed your adjusted gross income by 7.5%.

Home Renovation

Home renovation expenses are not typically deductible on an individual’s tax return. However, you can deduct such home renovations as medical costs when you make certain improvements to your house, mainly for medical purposes, such as lowering cabinets for better accessibility or adding wheelchair ramps. However, when the renovations specifically improve your home’s value, one cannot claim them as medical expenses.

Tax Preparation Charges

Whether you pay someone to prepare your taxes or do it yourself, you can write off charges on your miscellaneous tax deductions using a tax calculator and bookkeeping concepts. Expenses can include electronic filing and tax return preparation fees. However, the preparation charges should exceed two percent of your adjusted gross income to qualify for such a deduction.

Moving Expenses

When you satisfy the IRS time and distance test requirements upon your relocation for new employment, you can deduct moving expenses from your taxes. In this regard, the movement of military personnel due to service obligations does not require them to meet any time or distance qualifications.

Jury Duty Pay

When you return your jury pay, as you also received your paycheck while serving on a jury, you can deduct such pay from your overall taxable income.

Job Search Costs

Looking for employment can cost you money. You should add these expenses to the list of your write-offs. Itemizing them can help you deduct costs that occurred during your job search. It would help to remember that your job search must be most relevant to your current or most recent employment. Moreover, the search expenses that you may deduct include:

Preparation, printing, and sending your resume

Transportation that provides for a deduction of tolls, cab, parking, and 54 cents per mile fees

Employment agency fees

Other fees related to job searches

Investment Fees and Costs

Certain charges you pay for your investments’ management qualify as miscellaneous deductions. Such fees and expenses can include:

Investment counseling charges

Custodial charges paid outside of the account

Safe-deposit rental fees

Online and software services you utilized to manage your investments

Legal costs you paid to collect taxable income

All transportation expenses to and from a financial or investment advisor’s office

Costs needed to replace your lost security certificates

Airline Baggage Fees

If you are an entrepreneur, freelancer, or simply a self-employed individual, always deduct your baggage fees for the travel you do for business purposes. Your mind might be blown to see how they add up and cost you.

Home Appraisal Charges

One can deduct home appraisal fees as a miscellaneous itemized deduction only when the real estate property was an integral part of a charitable donation.

Mortgage Points

When you itemize your mortgage points or prepare the interest you paid to buy or construct your primary house, you can deduct them. Typically, when you can deduct the entire interest paid on your mortgage, you can deduct all the points.

Charges to Collect Dividends and Interest

Any charges you pay to a bank, trustee, broker, or similar agent to collect taxable dividends on shares of stock or interest on bonds are deductible. However, the actual securities, bonds, or stocks are not deductible.

Home Sale

When you sell your house at any profit, you can deduct up to $250k of profit from your income. Remember, if you are married or filing jointly, you can exclude a maximum of $500k.

Casualty, Theft Loss and Disaster

It is a significantly painful experience to suffer damage or loss to your house, household items, and vehicles. If your insurance coverage does not pay for them, they are, at the very least, tax-deductible.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Embarking on the path to financial stability is a journey that goes beyond mere budgeting and debt repayment—it requires a thoughtful and strategic approach to investing. For those new to the world of financial growth, the first step is to set specific, long-term goals. This involves looking beyond the allure of quick gains and considering the bigger picture, especially in dynamic sectors like the stock market.

Recognizing the need for guidance in this intricate landscape, investing in a financial advisor becomes crucial. Despite the wealth of information available through platforms like Google and Amazon, the personalized insights provided by financial experts are invaluable. These professionals can help distinguish sound investment opportunities from fleeting trends, steering individuals away from the pitfalls of short-term advice often found on television.

Keeping costs low, even with limited initial funds, is essential in the early stages of investing. Small, prudent investments can accumulate over time, building a foundation for more significant opportunities in the future. Diversifying one’s portfolio is another fundamental principle, incorporating a mix of assets like real estate stocks, mutual funds, and retirement accounts. Thoroughly investigating different industries, including housing markets and stock prices, is necessary before venturing into the world of investments.

Knowledge is power in finance, but the complex jargon can be overwhelming. Thus, conducting in-depth research before making investment decisions is crucial. This diligence can be the determining factor between successful wealth-building and potential losses.

Lastly, considering automation in investment through tools like 401(k) plans or IRAs offers a streamlined and disciplined approach. Automatic contributions to low-cost funds ensure a consistent and sustainable investment strategy.

In the following sections, we will delve deeper into these fundamental principles, providing actionable insights for individuals to confidently navigate the path toward financial prosperity.

The following six tips for beginners can help you invest your money correctly and wisely.

Set Specific Goals

If you want to make money in the long term, you must set specific goals for yourself. You must consider the bigger picture for beginners rather than just making fast cash. For this purpose, you must consider volatile industries like the stock market.

Invest in a Financial Advisor

You might need extra coaching even with enormous resources like Google’s search engine and Amazon’s digital library. Monetary advisors are not simply an extra expense. They may be able to help you differentiate a sound investmentoption from merely a fad and give you personalized advice as well. Financial strategists, which are recommended, are avoiding TV for their stock market advice as most television critics offer only short-term information.

Keep Costs Low

Even when you only have a small amount of money, numerous small investments can build into a significant payoff. Whenever you are new to investing, you should avoid spending large sums of money, even if it is available. When you keep your costs low, you will have more funds later when you want to invest in a more significant opportunity.

Diversify Your Portfolio

Investment portfolios may include real estate stocks as well. Along with this, mutual funds and retirement accounts are included as well. Every industry has its beats, which means you are supposed to thoroughly investigate the housing markets and stock prices before you dip your toe in the water.

Do In-Depth Research

It is an understatement to say that knowledge is power, especially regarding investments. Nevertheless, the complex financial jargon can sometimes be very overwhelming and complex. Therefore, you must conduct in-depth research before deciding to invest somewhere. This research can make or break your investment, not to mention your bank account. Most of the time, investments lead to loss only because the investor ignored completing their research.

Consider Automation

Numerous types of investments can be made with automatic contributions. For instance, a 401(k) plan or an IRA is a great way to invest your money. Low-cost finds are considered to be the best for automatic deposits.

Conclusion

In conclusion, embarking on the journey toward financial stability involves more than just budgeting and paying off debt; it requires a strategic approach to investing. Setting specific long-term goals is crucial for beginners, mainly focusing on volatile industries like the stock market. Seeking guidance from a financial advisor can provide valuable insights and personalized advice to navigate the complexities of investment. Keeping costs low, diversifying your portfolio across various assets, and conducting in-depth research before making decisions are vital principles for successful investing.

Additionally, considering automated contributions through vehicles like 401(k) plans or IRAs can streamline the investment process, ensuring a steady and disciplined approach to wealth-building. By incorporating these tips, individuals can take confident steps towards saving money and making it work through intelligent and informed investments.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

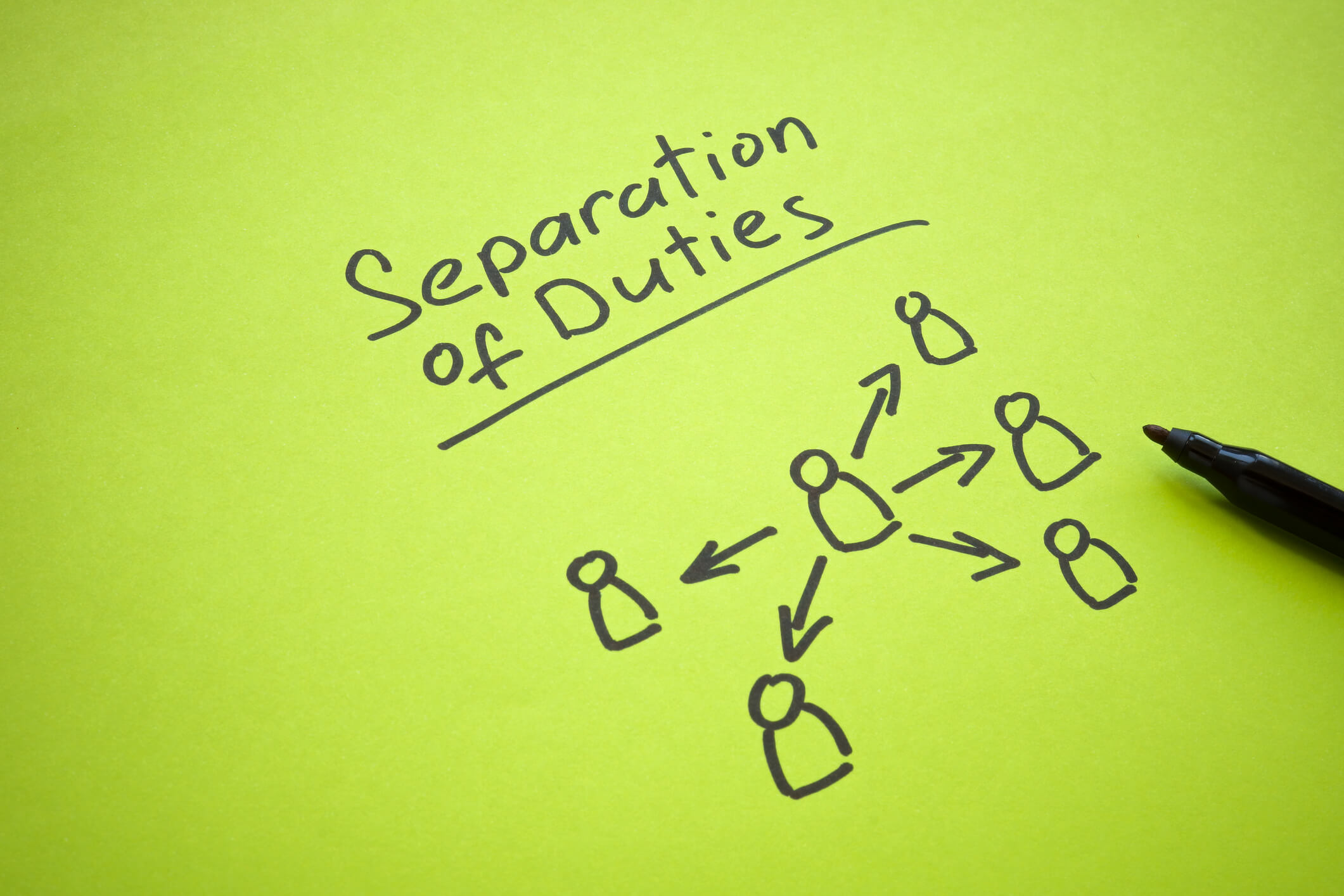

In a business, it is important to separate employee duties as it can help safeguard your assets, among many other beneficial components. Separation of duties can help you place internal controls over your company’s assets. Separation of duties can help you practice bookkeeping more efficiently and effectively as it prohibits the allocation of responsibilities to one person.

Effective business management hinges on the critical principle of segregating duties, particularly evident in both general business and accounting practices. The delineation of responsibilities, specifically the custody, authorized use, and record-keeping of assets, is a powerful mechanism. This facilitates error detection and prevention and acts as a formidable deterrent against theft and fraud.

Although challenging to implement in small businesses, adopting duty separation fully significantly enhances employee performance and overall organizational efficacy. Furthermore, this principle extends its influence to information systems, where fraud prevention is paramount.

By establishing clear roles and responsibilities, businesses fortify accountability, enhance work performance, and create a culture of trust. In the realm of employee accountability, the implementation of duty separation significantly boosts the credibility of financial reporting, mitigates the risk of fraud, and safeguards against unnecessary losses. This strategic approach ensures organizationalefficiency, minimizes workloads, and fosters a stress-free environment, underscoring the importance of involving multiple employees in tasks to prevent potential errors and reduce the opportunity for fraudulent behavior.

Application in General Business and Accounting

In general business and accounting, segregation of duties serves two essential purposes. These purposes include assurance that you are able to review and catch errors easily if there is an oversight, and it also prevents theft and fraud. Separation of duties is an important phenomenon as it involves separating three main functions:

1. Custody of assets.

2. Authorized use of assets.

3. Keeping records of assets.

Although separation of duties is difficult to achieve in small business, it should be implemented as much as possible to improve the performance of the employees in the organization.

Application in Information Systems

Business owners never want fraud to occur in their company. However, it can happen when a single person handles more than one step of the transaction style. This often happens in small businesses as there aren’t many employees. That is why setting clear roles and responsibilities for each job is essential. This gives employees a thorough list of the tasks they are expected to do when they should perform them, and who will be reviewing their work.

It plays a pivotal role in the accountability of employees. Without various levels of accountability, even the best organizations can be rendered meaningless. By separating the duties of employees, work performance is enhanced. Business owners should separate the responsibilities of each employee so that their skills can be polished and deter the staff from committing fraud.

Employee Accountability

When this process is implemented, the credibility of accurate financial reporting is vastly increased. This reduces the risk of fraud as it assures the creation of a culture of accountability. It protects the business from any type of unnecessary or unplanned loss. Separation of duties can increase efficiency towards the aims and objectives of an organization. This assures that your employees are not burdened with huge workloads and you are providing a stress-free environment. Involving multiple employees in a single task can prevent any type of potential error. Involving more than one person in the transaction cycle can prevent one person from gaining complete control over a single process. Therefore, the opportunity for fraudulent behavior is reduced.

Conclusion

In conclusion, embracing the practice of separating employee duties is crucial for safeguarding assets, enhancing accountability, and reducing the risk of fraud. Whether applied in general business, accounting, or information systems, the benefits of duty separation contribute to improved organizational performance, credibility in financial reporting, and the creation of a stress-free and efficient work environment. By recognizing the significance of dividing responsibilities, businesses can fortify internal controls and foster a culture of accountability, ultimately safeguarding against unnecessary losses and potential fraudulent activities.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Understanding the Allocation of Labor in Architecture: A Comprehensive Guide

Architecture is a complex field requiring several professionals to coordinate the successful completion of a project. As with any other field, allocating labor in architecture is a critical aspect that must be understood to ensure that the project is completed on time, within budget, and to the satisfaction of all stakeholders. This article will provide a comprehensive guide to help you understand labor allocation in architecture.

Roles and Responsibilities in Architecture

Architects, engineers, contractors, and subcontractors are the primary professionals involved in architecture. These professionals are critical in project design, construction, and management.

Architects are responsible for the overall design and management of the project. They work closely with the client to understand their needs and develop a design that meets their requirements. They also coordinate with other professionals to ensure the project is completed on time, within budget, and to the required quality standards.

Engineers are responsible for ensuring the design is structurally sound and meets all applicable codes and regulations. They work with the architect to develop the structural and mechanical systems necessary for the project. They also provide input on the selection of materials and construction methods.

Contractors are responsible for the construction of the project. They manage the day-to-day operations and ensure the project is completed on time and within budget. They also coordinate with subcontractors to ensure that the work is completed to the required quality standards.

Subcontractors are responsible for specific tasks within the project, such as electrical work, plumbing, or HVAC systems. They work under the direction of the contractor and must ensure that their work is completed to the required quality standards.

The Allocation of Labor in Architecture

The allocation of labor in architecture is a complex process that requires careful coordination between the various professionals involved in the project. The process typically involves several stages: design, construction, and management.

Design stage

During the design stage, the architect coordinates with the client to develop a design that meets their requirements. This process involves several steps, including:

Site Analysis: The architect thoroughly analyzes the site to understand the opportunities and constraints that will influence the design.

Conceptual Design: Based on the site analysis, the architect develops an abstract design that outlines the project’s overall design.

Schematic Design: The architect further refines the design by developing detailed drawings and specifications.

Design Development: The architect finalizes the design by developing detailed construction drawings and specifications.

Construction stage

During the construction stage, the contractor manages the project’s day-to-day operations. This process involves several steps, including:

Pre-Construction: The contractor works with the architect and engineers to finalize the drawings and specifications. They also obtain any necessary permits and approvals.

Site Preparation: The contractor prepares the site for construction by clearing the land and installing any necessary infrastructure.

Construction: The contractor manages the construction process, including scheduling subcontractors, ordering materials, and managing the budget.

Quality Control: The contractor ensures that the work is completed to the required quality standards and that any issues are addressed in a timely manner.

Management stage

During the management stage, the architect and contractor are responsible for managing the project and ensuring it is completed on time and within budget. This process involves several steps, including:

Project Management: The architect and contractor work together to manage the project, including scheduling, budgeting, and quality control.

Change Management: Any changes to the project, such as design changes or scope changes, must be carefully managed to ensure that they do not impact the overall project schedule or budget.

Commissioning: Once the project is completed, the architect and contractor work together to ensure that all systems are functioning as intended.

Conclusion

The allocation of labor in architecture is a critical aspect that requires careful coordination between the various professionals involved in the project. By understanding each professional’s roles and responsibilities and the project’s various stages, you can ensure that your project is completed on time, within budget, and to the required quality standards. So, whether you are a client, architect, engineer, contractor, or subcontractor, understanding the allocation of labor in architecture is essential for the successful completion of any project.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Boost Your Leadership with Executive Cyber Training Insights

Executive cyber training equips senior leaders with specialized cybersecurity education that combines strategic risk management, incident response leadership, and security culture development to protect organizational assets and executive reputation. This targeted approach goes beyond standard employee awareness programs to address the unique threats facing C-suite executives, including sophisticated whaling attacks, mobile device vulnerabilities, and crisis communication challenges.

As someone who has led a cloud-based financial services company for over two decades, I’ve witnessed cybersecurity evolve from an IT concern to a boardroom imperative. The statistics are sobering—72% of senior executives admit feeling unprepared for cyberattacks, while 89% of organizations experienced cyber incidents last year. Through my work with businesses across all sectors at Complete Controller, I’ve seen how proper executive cyber training transforms leadership confidence and organizational resilience. This article will equip you with proven frameworks for risk assessment, crisis management strategies, and implementation best practices that reduce breach costs by an average of $1.5 million.

What is executive cyber training and why should leaders prioritize it?

Executive cyber training is comprehensive security education tailored specifically for senior leadership roles and decision-making responsibilities

It addresses unique risks executives face, including whaling attacks, social engineering, and reputation management during incidents

Training focuses on strategic frameworks for risk assessment, budget allocation, and building organization-wide security culture

Programs include crisis leadership simulations, incident response protocols, and stakeholder communication strategies

Effective training reduces organizational risk by up to 45% while improving executive confidence in cyber decision-making

Understanding the Executive Cyber Threat Landscape

Modern cybercriminals specifically target senior leaders through sophisticated social engineering techniques that leverage publicly available information. The 2019 WhatsApp attack on Amazon CEO Jeff Bezos demonstrates how even security-conscious executives fall victim to advanced threats. These targeted campaigns exploit the unique vulnerabilities of executive roles—constant connectivity, public visibility, and decision-making authority.

Research reveals that 96% of executives believe organization-wide training will reduce cyberattacks, yet implementation gaps persist. Threat actors invest weeks researching targets, analyzing travel schedules, business relationships, and communication patterns to craft personalized attacks. This intelligence gathering enables precisely timed strikes during vulnerable periods such as major transactions or organizational transitions.

Advanced persistent threats targeting leadership

Executive-focused attacks involve multi-stage campaigns designed to bypass traditional security measures. Cybercriminals create elaborate schemes impersonating board members, regulatory authorities, or trusted partners to manipulate executives into authorizing fraudulent transactions. These sophisticated operations exploit the pressure executives face to make rapid decisions with limited information.

The mobile security challenge for executives

Senior leaders’ reliance on mobile devices creates significant security vulnerabilities. Corporate security policies often fail to address executive mobility requirements, leaving critical communication channels exposed. Personal devices used for business purposes compound these risks, creating attack vectors that traditional security frameworks cannot adequately protect.

Essential Components of Effective Executive Cyber Training

Successful executive cybersecurity programs address strategic decision-making and organizational risk management rather than technical implementation details. Leaders require skills to evaluate threats within business contexts, considering revenue protection, brand reputation, and regulatory compliance implications.

Cybersecurity training for executives: Strategic risk assessment

Modern programs emphasize risk-based decision frameworks that align security investments with business objectives. Executives learn to quantify cyber risks in financial terms, enabling informed decisions about security budgets and risk tolerance levels. This strategic approach transforms cybersecurity from a cost center to a business enabler.

Advanced awareness training covers supply chain compromises, insider threats, and nation-state attacks. Leaders develop capabilities to recognize early warning signs of targeted campaigns and understand how their digital footprints create vulnerabilities. This awareness extends to family members and personal activities that could compromise organizational security.

Corporate cybersecurity training: Building organizational resilience

Executive training emphasizes establishing security-conscious cultures throughout organizations. Leaders learn to communicate security priorities effectively across stakeholder groups while integrating security considerations into strategic planning processes. This cultural transformation proves more effective than technology solutions alone.

Leadership in Cybersecurity: Crisis Management and Incident Response

Cyber incidents require executives to transition rapidly from strategic oversight to tactical crisis management. Among Fortune 100 companies, only 51% have directors with cybersecurity backgrounds, dropping to 17% for S&P 500 companies—highlighting critical expertise gaps during crisis situations.

Risk management for executives: Decision-making under pressure

Crisis simulations prepare leaders for time-sensitive decisions with incomplete information. Executives practice evaluating containment options, communication strategies, and business continuity measures while managing multiple stakeholder groups. These exercises reveal decision-making patterns and improve response protocols.

Stakeholder communication during cyber incidents

Effective incident communication balances transparency with legal requirements while maintaining stakeholder confidence. Training addresses investor relations, customer communications, and media management during active incidents. Communication timing and messaging significantly impact both immediate response effectiveness and long-term reputation recovery.

Executive Cyber Training Courses: Program Structure and Delivery

Leading programs combine online modules, workshops, and scenario-based simulations to accommodate executive schedules while delivering comprehensive skill development.

Carnegie Mellon University’s twelve-week Cybersecurity Leadership program exemplifies effective online delivery for working professionals. Short, focused modules enable learning during travel or between meetings while maintaining access to expert instructors and peer networks.

Cybersecurity training programs for leaders: Immersive experiences

Duke University’s Executive Cybersecurity Certificate Programs demonstrate the value of intensive multi-day experiences combining classroom instruction with hands-on simulations. These programs enable deep engagement with complex scenarios, fostering stronger peer connections and accelerated skill development.

Best Practices in Executive Cybersecurity Training

Organizations implementing executive training must address time constraints, varying technical backgrounds, and confidentiality requirements. A UK financial institution’s comprehensive program reduced phishing click rates from 25% to 4% within one year, while a US retail company achieved 60% reduction in email attacks, saving $2 million annually.

Executive protection training: Personal security integration

Comprehensive programs integrate personal security with organizational protocols, recognizing that executives’ personal and professional digital lives are inseparable. Training addresses secure communication methods, travel protocols, and family cybersecurity awareness.

Measuring training effectiveness and ROI

Global data breach costs average $4.45 million, but organizations with strong security awareness training reduce breach costs by $1.5 million. Successful programs track incident response times, decision quality during simulations, and security budget allocation changes to demonstrate tangible returns on training investments.

Conclusion

Executive cyber training represents a fundamental shift in viewing cybersecurity as core leadership competency rather than technical concern. The programs and strategies outlined demonstrate that effective cybersecurity leadership requires dedicated training, ongoing development, and integration with business strategy. Through my experience leading Complete Controller’s digital transformation, I’ve learned that executives who invest in comprehensive cyber training protect their organizations more effectively while making confident security decisions. Contact the experts at Complete Controller for guidance on strengthening your cybersecurity leadership capabilities and building organizational resilience.

Frequently Asked Questions About Executive Cyber Training

What makes executive cyber training different from regular employee cybersecurity training?

Executive cyber training focuses on strategic decision-making, crisis leadership, and risk management responsibilities specific to senior leadership roles, rather than operational security tasks.

How long do executive cybersecurity training programs typically last?

Programs range from intensive 2-3 day workshops to comprehensive 10-12 week online courses, with most effective programs combining multiple formats and ongoing education components.

What are the main topics covered in executive cyber training?

Core topics include strategic risk assessment, incident response leadership, crisis communication, regulatory compliance, security culture development, and advanced threat awareness.

Do executives need technical cybersecurity knowledge for leadership roles?

While deep technical expertise isn’t required, executives need sufficient understanding to make informed decisions about security investments, risk tolerance, and strategic priorities.

How often should executives participate in cybersecurity training updates?

Leading practices recommend annual training updates with quarterly briefings on emerging threats and regulatory changes, plus immediate training following significant industry incidents.

Sources

BlackCloak. “Cybersecurity Training for Executives: What Business Leaders Need to Know.” BlackCloak Blog, 13 Feb. 2025, blackcloak.io/cybersecurity-training-for-executives-what-business-leaders-need-to-know/.

Carnegie Mellon University Executive Education. “Cybersecurity Leadership.” CMU Institute for Software Research, execed.s3d.cmu.edu/elearning/programs/cybersecurity-leadership/index.html.

National Association of Counties. “NACo Enterprise Cybersecurity Leadership Academy.” NACo Professional Development, 1 Aug. 2023, www.naco.org/page/naco-enterprise-cybersecurity-leadership-academy.

SANS Institute. “Cybersecurity Leadership Training.” SANS Focus Areas, 29 July 2025, www.sans.org/cybersecurity-focus-areas/leadership.

Duke University. “Duke Executive Cybersecurity Certificate Programs.” Duke Continuing Studies, 10 June 2025, cisoeducation.duke.edu.

ISC2. “ISC2 Survey: More Cybersecurity Leadership Training Needed.” ISC2 Insights, 12 Dec. 2024, www.isc2.org/Insights/2024/12/ISC2-Survey-Cybersecurity-Leadership.

CM Alliance. “The Importance of Cybersecurity Training for Executives in 2025.” CM Alliance Cybersecurity Blog, 8 July 2025, www.cm-alliance.com/cybersecurity-blog/the-importance-of-cybersecurity-training-for-executives-in-2025.

Security Boulevard. “Cyber security training for executives: Why and how to build it.” Security Boulevard, 6 Feb. 2025, securityboulevard.com/2025/02/cyber-security-training-for-executives-why-and-how-to-build-it/.

Whatfix. “Cybersecurity Training for Employees: Best Practices, Courses.” Whatfix Blog, 2 Jan. 2023, whatfix.com/blog/cybersecurity-training/.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

Consumer Side Resource Accounting: Taking Control of Your Cloud Costs

Consumer-side resource accounting empowers businesses to independently track, monitor, and optimize their cloud spending through self-managed monitoring systems rather than relying solely on provider-generated billing statements. This approach transforms passive cloud consumption into active resource management, giving organizations complete visibility and control over their infrastructure costs.

Over my 20 years as CEO of Complete Controller, I’ve witnessed countless businesses struggle with unexpected cloud bills and unclear resource allocation. The shift to consumer-controlled accounting represents a fundamental change in how smart companies manage their digital infrastructure. This article reveals the specific tools, strategies, and methods that leading organizations use to slash cloud costs by 20-40% while gaining unprecedented control over their spending patterns. You’ll discover practical implementation techniques for budget management, cost allocation systems, and optimization strategies that transform cloud accounting from a monthly surprise into a strategic advantage.

What is consumer-side resource accounting, and how do you master it?

Consumer-side resource accounting means independently tracking and managing your cloud costs through self-implemented monitoring systems

It involves using specialized tools to monitor resource consumption beyond basic provider billing

Organizations achieve 20-40% cost savings through improved visibility and control

Success depends on combining automated monitoring with strategic resource management

The Foundation of Consumer-Controlled Cloud Monitoring

Consumer-side resource accounting fundamentally shifts control from cloud providers to individual organizations, placing detailed visibility and management capabilities directly in users’ hands. Traditional cloud billing aggregates usage data at high levels, making it nearly impossible to understand which departments, projects, or applications drive specific costs.

The concept emerged from research at Newcastle University, which demonstrated that consumers could successfully implement independent accounting systems for cloud services. This groundbreaking work established that organizations need not accept provider billing as the only source of truth about their resource consumption.

Modern implementation involves deploying parallel monitoring systems that collect granular usage metrics across compute, storage, networking, and application services. These systems operate independently from provider billing, offering customized reporting formats and real-time visibility that aligns with specific organizational needs.

The methodology encompasses multiple tracking dimensions:

Compute resource utilization patterns

Storage consumption trends

Network bandwidth analysis

Service-specific usage metrics

Application-level cost attribution

Companies implementing these strategies report dramatic improvements in cost predictability and resource efficiency. The approach correlates business activities directly with infrastructure costs, enabling data-driven decisions about technology investments and optimization priorities.

Essential Tools for Independent Resource Tracking

The contemporary monitoring landscape offers sophisticated technologies specifically designed for consumer-side resource accounting. Native cloud provider tools like Amazon CloudWatch, Azure Monitor, and Google Cloud Operations Suite provide foundational monitoring capabilities with direct service integration.

Third-party platforms have emerged to address native tool limitations, offering enhanced functionality for cost optimization and multi-cloud management. These specialized solutions provide:

Unified dashboards across multiple cloud providers

Advanced analytics for cost trending

Automated anomaly detection

Predictive forecasting capabilities

Custom alerting mechanisms

Cost monitoring tools represent a critical category, with platforms offering detailed spending analysis and waste identification. According to Flexera’s State of the Cloud Report, companies waste an average of 32% of their cloud budget, with overprovisioned resources (59%) and idle resources (66%) being the primary culprits.

Container monitoring solutions address the unique challenges of modern microservices architectures. These tools provide visibility into Kubernetes costs, container resource consumption, and orchestration platform expenses that traditional monitoring often misses.

Automation platforms enable policy-driven resource management, automatically responding to monitored conditions with predefined actions. These systems can scale resources based on demand, implement cost controls at budget thresholds, and optimize configurations based on performance metrics.

Implementing Effective Cost Allocation Strategies

Cost allocation forms the cornerstone of successful consumer-side resource accounting by mapping cloud expenses to specific organizational dimensions. Without proper allocation, organizations cannot understand which projects, departments, or applications drive their cloud costs.

Successful implementation begins with developing a comprehensive tagging strategy. Effective tags typically include:

Automation proves critical for consistent tagging implementation. Organizations should embed tagging requirements into infrastructure-as-code templates, automated provisioning workflows, and governance policies that enforce standards at resource creation time.

Cost allocation reporting transforms raw data into actionable intelligence through multi-dimensional analysis capabilities. Modern platforms provide drill-down functionality, trend analysis, and comparative reporting that supports detailed optimization planning.

Integration with business intelligence systems enables correlation between cloud costs and business outcomes. This connection facilitates development of cloud cost models aligned with business planning processes, enabling accurate forecasting based on projected growth patterns.

Budget Management Systems That Prevent Overspending

Comprehensive budget management prevents unexpected cloud bills through proactive monitoring and automated controls. Effective systems combine predictive forecasting, real-time tracking, and intelligent alerting to maintain spending within acceptable parameters.

Hierarchical budgeting structures align with organizational needs:

Enterprise-level budgets for overall spending control

Department budgets for team accountability

Project budgets for initiative tracking

Environment budgets for development vs. production costs

Alert configuration requires multiple threshold levels to provide escalating warnings. Organizations typically set notifications at 50%, 75%, and 90% of budget consumption, ensuring adequate response time before limits are exceeded.

Forecasting capabilities analyze historical patterns and growth trends to predict future spending. Machine learning algorithms identify seasonal variations and usage anomalies, providing accurate predictions that enable proactive budget adjustments.

Automated response mechanisms implement cost controls when thresholds are exceeded. These might include resource scaling limitations, approval requirements for new provisioning, or automatic shutdown of non-production environments during off-hours.

Integration with financial management systems incorporates cloud budgets into organizational financial planning. This alignment supports sophisticated analysis of cloud ROI and enables standard financial reporting of technology investments.

Advanced Optimization Techniques for Maximum Savings

Resource optimization translates monitoring insights into concrete actions that improve efficiency and reduce unnecessary spending. Rightsizing strategies match cloud resource capacity with actual workload requirements, eliminating overprovisioning while maintaining performance.

Analysis examines multiple utilization metrics:

CPU usage patterns

Memory consumption trends

Storage I/O requirements

Network traffic volumes

Application response times

Auto-scaling technologies enable dynamic optimization responding to demand fluctuations without manual intervention. Properly configured policies scale resources up during peak periods and down during quiet times, maintaining optimal utilization continuously.

Reserved instance optimization provides significant savings for predictable workloads through commitment-based pricing. Organizations analyze usage patterns to identify suitable workloads and select appropriate reservation terms, often achieving 40-60% cost reductions compared to on-demand pricing.

Storage optimization implements tiering strategies based on access patterns. Automated lifecycle policies move infrequently accessed data to lower-cost storage tiers, while identifying and eliminating orphaned volumes that continue incurring charges.

Spot instance utilization offers substantial discounts for fault-tolerant workloads. Organizations implement hybrid architectures combining spot, on-demand, and reserved instances to achieve optimal cost-performance balance across different workload types.

Final Thoughts

Consumer-side resource accounting transforms cloud cost management from reactive bill payment to proactive resource optimization. The combination of independent monitoring, strategic cost allocation, comprehensive budgeting, and continuous optimization enables organizations to achieve significant savings while maintaining performance and reliability.

Success requires commitment to implementing proper tools, establishing clear processes, and fostering a culture of cost accountability across technical teams. Organizations that master these techniques gain competitive advantages through improved resource efficiency and predictable technology spending.

The experts at Complete Controller help businesses implement comprehensive cloud accounting strategies tailored to their specific needs. Contact us today to discover how consumer-side resource accounting can transform your cloud cost management and deliver measurable savings to your bottom line.

Frequently Asked Questions About Consumer Side Resource Accounting

What exactly is consumer-side resource accounting?

Consumer-side resource accounting is the practice of independently monitoring and managing cloud resource usage and costs through self-implemented tracking systems rather than relying solely on cloud provider billing statements. It gives you granular visibility and control over your cloud spending.

How much can companies save with consumer-side resource accounting?

Organizations implementing comprehensive consumer side resource accounting typically achieve 20-40% cost savings. These savings come from identifying waste, rightsizing resources, optimizing reserved instances, and implementing automated cost controls.

What tools do I need to start consumer-side resource accounting?

You’ll need monitoring tools (native or third-party), cost allocation systems with tagging capabilities, budget management platforms with alerting features, and optimization tools for rightsizing and automated scaling. Many platforms combine multiple capabilities in unified solutions.

How long does it take to implement consumer-side resource accounting?

Basic implementation can begin immediately with native cloud monitoring tools. A comprehensive system including tagging strategies, budget controls, and optimization workflows typically takes 2-3 months to fully deploy, with benefits starting within the first month.

What are the biggest challenges in implementing consumer-side resource accounting?

Common challenges include inconsistent tagging practices, integrating data from multiple cloud providers, organizational resistance to cost accountability, and a lack of specialized expertise. Success requires strong governance policies and executive support for cost transparency initiatives.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

There is no denying that cutting business expenses and controlling costs has become extremely challenging in today’s business environment. Modern trends indicate that companies must reduce expenses to achieve their business goals and objectives effectively.

However, establishing control over your business and finances requires much motivation, knowledge, skills, and expertise. Why? Because only a clear-cut strategy and well-laid-out plan can make cutting down your monthly expenses hassle-free.

Are you cutting business expenses? Not a problem!

Moreover, reducing business expenses and increasing revenue can greatly impact a company’s profitability and are two ways companies can maximize their profitabilityindex. According to industry experts, increasing sales and revenue is hard because it requires a lot of planning and strategy. It takes time and effort to come up with a brilliant execution plan.

On the contrary, cutting business expenses can be done easily, without much stress. All that it takes is a little bit of your time. Moreover, reviewing your bookkeeping and accounting records to understand your company’s standing before making solid decisions regarding controlling your costs is important.

Reduce Supply Expenses

If you expect to reduce supply expenses, you must look outside your pool of traditional vendors. Look for the vendors, manufacturers, or suppliers who can offer you the best price, as large discounts help you cut business expenses and costs.

Bulk purchasing is ideal in every sense. Always seek multiple bids to get ideal rates, and never make a long-term contract for supplies with a single party or vendor, as the savings can greatly impact your bottom line.

Lower Financial Expenses

Hiring an in-house accounting or auditing professional can be a costly decision. That’s why most businesses rely on external accounting agencies or individuals who offer competitive rates for their services. Cutting your business expenses means saving money on insurance and additional bills.

You must regularly contribute to your savings account to meet financial emergencies and consider a business expansion. Lastly, please don’t take on unnecessary debt to make ends meet because you may eventually find it hard to pay back the money you borrowed from the bank with interest. Before making such decisions, you must do a thorough cost-benefit analysis and future forecasting.

Take Advantage of Social Media Marketing

Traditional marketing can cost you a fortune. This indicates that you must look at cheaper alternatives like social media marketing like Facebook, Twitter, and other dynamic platforms. You can build your customer base there, as studies have revealed that social media marketing is more effective than traditional marketing on the mainstream media, ultimately reducing your business expenses.

Try to Achieve Economies of Scale

By maximizing your productivity in manufacturing, you can expect to take your expenses to a minimum level. Improved R&D and market knowledge will help you achieve economies of scale, ideal for maximizing profitability.

Review Your Finances and Business Books Quarterly

To get a clear picture of your finances and business condition, you must review and maintain them. And manage your business books, if not every month, then quarterly. Moreover, it would help if you audited your monthly subscription billing to cut business expenses. Switch to the software applications or talent worth your investment and money.

Look for Affordable and Suitable Office Alternatives

You can always consider relocating your office to a more affordable area to cut business costs. Companies frequently don’t need their offices in prime, expensive locations in the digitalization age. You can move your office to a convenient location that offers affordable rates to reduce commercial rents.

Conclusion

In conclusion, navigating the challenging landscape of business expenses requires strategic planning and a clear-cut approach. While increasing revenue demands a meticulous strategy, cutting expenses can be easily achieved. It is crucial to explore various avenues, from supply and financial expenditures to marketing strategies, embracing cost-effective alternatives. Regular financial reviews, prudent decision-making, and exploring affordable office solutions contribute to sustained cost reduction. By adopting these measures, businesses can enhance profitability, positioning themselves for long-term success in today’s dynamic business environment.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Understanding Accounting and Economic Costs: Key Differences

Accounting vs economic costs represent two fundamentally different approaches to measuring business expenses, where accounting costs track only the explicit money spent while economic costs include both explicit expenditures and the opportunity costs of foregone alternatives. The distinction between these measurement methods dramatically impacts how businesses evaluate profitability, allocate resources, and make strategic decisions about future investments.

Over my 20 years as CEO of Complete Controller, I’ve watched countless businesses struggle with profitability despite showing positive numbers on their financial statements. The missing piece? They focus exclusively on accounting costs without considering the economic reality of their choices. When you understand that every dollar invested in one area means sacrificing potential returns elsewhere, your entire approach to business strategy transforms. This article will equip you with the framework to analyze both cost types, apply them strategically to your business decisions, and avoid the common pitfalls that trap companies in suboptimal resource allocation patterns.

What are accounting vs economic costs?

Accounting costs measure explicit, out-of-pocket expenses while economic costs include both explicit expenses and implicit opportunity costs

Accounting costs track actual money spent on operations, materials, labor, and overhead expenses

Economic costs add the value of foregone alternatives to provide a complete picture of resource allocation decisions

Understanding both cost types enables better strategic planning and resource optimization

The difference between accounting profit and economic profit reveals whether resources generate optimal returns

Defining Accounting Costs in Business Operations

Accounting costs form the foundation of traditional financial management by tracking every dollar that flows out of your business bank accounts. These explicit expenses include wages, rent, utilities, raw materials, equipment purchases, marketing expenses, and any other payment made to external parties. The defining characteristic of accounting costs lies in their tangible, documentable nature—each expense creates a paper trail through invoices, receipts, and bank statements that accountants use to prepare financial statements and tax returns.

The systematic tracking of accounting costs serves multiple critical business functions beyond simple expense monitoring. Financial statements built on accounting costs provide stakeholders with standardized performance metrics, enable tax compliance and regulatory reporting, support loan applications and investor communications, and create benchmarks for operational efficiency. A manufacturing company that spends $250,000 monthly on rent, salaries, and materials knows exactly where its money goes and can compare these figures against industry standards to assess competitive positioning.

Components and categories of accounting costs

Direct costs represent expenses clearly attributable to specific products or services, including raw materials, direct labor, and manufacturing supplies. Indirect costs encompass overhead expenses like administrative salaries, facility maintenance, and general business insurance that support overall operations rather than specific production activities. Fixed costs remain constant regardless of production volume, while variable costs fluctuate with business activity levels.

Small businesses often struggle with proper cost categorization, leading to pricing errors and profitability miscalculations. A bakery might track flour and sugar as direct costs but mistakenly classify the baker’s salary as overhead rather than direct labor, distorting product profitability analysis. Accurate categorization enables precise product costing, informed pricing decisions, and strategic resource allocation based on actual expense patterns rather than assumptions.

Understanding Economic Costs Through Opportunity Analysis

Economic costs expand the cost analysis framework by incorporating opportunity costs—the value of the best alternative sacrificed when making any business decision. This comprehensive approach recognizes that resources committed to one purpose cannot simultaneously serve another, creating implicit costs beyond the explicit accounting expenses. Economic cost analysis transforms business planning from a simple expense-tracking exercise into a strategic evaluation of competing alternatives and their relative value creation potential.

The power of economic thinking becomes clear when examining real business scenarios. A successful consultant earning $150,000 annually who launches a startup faces economic costs far exceeding the explicit startup expenses. Beyond the $50,000 in equipment and marketing costs, the economic analysis includes the $150,000 in foregone consulting income, representing a total economic cost of $200,000 for the first year. This perspective reveals why many seemingly profitable small businesses actually destroy economic value when opportunity costs exceed accounting profits.

Calculating implicit costs in economic analysis

Implicit costs manifest in various forms depending on the resources involved and alternatives available. Common implicit costs include the owner’s foregone salary from alternative employment, lost investment returns on capital tied up in business operations, rental income sacrificed by using owned property for business purposes, and the depreciation of skills or professional networks when pursuing different career paths. Each category requires careful evaluation to quantify the true economic impact of business decisions.

Business owners frequently underestimate implicit costs because they lack the obvious documentation associated with explicit expenses. A software developer who quits a $120,000 job to launch a mobile app company might celebrate breaking even on accounting costs within six months, not realizing the business has actually lost $60,000 in economic terms when considering the foregone salary. This disconnect between accounting success and economic failure explains why many entrepreneurs work longer hours for less total compensation than traditional employment would provide.

Critical Differences Between Accounting vs Economic Costs

The fundamental distinction between accounting vs economic costs extends beyond mere calculation methods to encompass entirely different business perspectives and decision-making frameworks. Accounting costs provide historical documentation of actual expenses, supporting compliance requirements and operational management through objective, verifiable data. Economic costs offer forward-looking insights into resource allocation efficiency, revealing whether current strategies maximize value creation compared to available alternatives.

These complementary perspectives serve distinct but equally important business functions. Accounting costs excel at answering questions about expense levels, budget compliance, and tax obligations, while economic costs address strategic concerns about resource optimization, competitive positioning, and long-term value creation. A retail chain might use accounting costs to track store performance and manage inventory levels while applying economic cost analysis to evaluate whether opening new locations generates better returns than investing in e-commerce capabilities or acquiring competitors.

Strategic implications of cost perspectives

The choice between accounting and economic cost analysis profoundly impacts business strategy and resource allocation decisions. Companies focusing exclusively on accounting costs often pursue growth opportunities that appear profitable but actually destroy economic value by generating returns below the opportunity cost of capital. Conversely, businesses that emphasize economic costs might reject accounting-profitable projects that fail to exceed opportunity cost thresholds, potentially missing viable expansion opportunities due to overly conservative analysis.

According to research from SAP Concur, companies that incorporate opportunity cost analysis into their resource allocation decisions optimize limited resources to areas with the highest impact and gain strategic clarity into projects that truly move the needle for business growth. This balanced approach combines accounting cost discipline with economic cost insights to identify strategies that satisfy both financial reporting requirements and long-term value creation objectives.

Patagonia’s decision-making process during their digital transformation exemplifies how economic cost analysis drives superior strategic choices. Facing the choice between opening twenty new retail locations or investing in e-commerce infrastructure, the outdoor clothing company conducted comprehensive cost analysis beyond simple expense comparisons. The accounting costs appeared similar—approximately $15 million for either retail expansion or digital platform development—but the economic analysis revealed dramatically different opportunity costs and strategic implications.

The retail expansion strategy would have required extensive management attention, limiting leadership’s ability to focus on product innovation and environmental advocacy initiatives that differentiated the brand. Additionally, physical stores would lock the company into long-term lease commitments and geographic constraints, reducing flexibility to respond to changing market conditions. The digital investment, while requiring similar upfront costs, preserved organizational agility and aligned with the company’s core competencies in brand building and sustainable product development.

Patagonia’s e-commerce platform now generates over $52 million in monthly revenue, validating their economic cost analysis. The digital strategy enabled rapid market expansion without the opportunity costs associated with physical retail management, allowing the company to maintain focus on product excellence and environmental leadership while achieving superior financial returns. This case demonstrates how economic thinking transcends simple ROI calculations to incorporate strategic considerations about organizational focus and capability development.

Small Business Applications of Economic Cost Analysis

Small business owners often dismiss economic cost analysis as an academic exercise irrelevant to their daily operations, yet this framework provides particularly valuable insights for resource-constrained enterprises. Consider the restaurant owner who works 70-hour weeks to generate $80,000 in annual accounting profit while possessing culinary skills that could earn $90,000 as a head chef elsewhere with better work-life balance. The economic loss of $10,000 plus quality of life considerations might justify selling the restaurant and pursuing employment that better utilizes their talents.

Burnt, a restaurant industry startup, provides a concrete example of opportunity cost calculation in practice. Facing a choice between investing $40,000 in securities offering 20% annual returns or purchasing new hardware and software systems, their analysis showed securities generating $4,000 and $4,400 in profits during years one and two respectively. However, the technology investment would yield $10,000 annually starting in year three, demonstrating how time horizons affect opportunity cost calculations and investment decisions.

Practical implementation strategies

Small businesses can implement economic cost analysis through systematic decision frameworks that balance thoroughness with practical constraints. Start by identifying the two or three most viable alternatives for any significant resource allocation decision. Calculate explicit costs for each option using standard accounting methods, then estimate implicit costs by considering what opportunities each choice eliminates. Focus particularly on owner time allocation, as entrepreneur hours often represent the scarcest resource in small businesses.

The key to successful implementation lies in avoiding analysis paralysis while maintaining analytical rigor. Create simple templates for common decisions like hiring versus outsourcing, equipment purchase versus leasing, and market expansion alternatives. Document assumptions about opportunity costs and revisit them quarterly as business conditions change. This structured approach transforms economic cost analysis from an abstract concept into a practical tool for improving business decisions and resource allocation.

Advanced Applications in Strategic Planning and Pricing

Economic cost analysis reaches its full potential when applied to complex strategic decisions involving multiple stakeholders, extended time horizons, and uncertain outcomes. A consumer packaged goods company that implemented comprehensive cost-to-serve analysis achieved a 12% increase in EBITDA by accurately identifying and quantifying the full cost of serving each customer, including both explicit costs and hidden service requirements. This granular understanding enabled strategic customer segmentation and pricing optimization based on true economic profitability rather than simplistic revenue or gross margin metrics.

Pricing strategy represents another sophisticated application where economic costs provide crucial insights beyond traditional cost-plus models. Professional service firms often discover that certain client types or project categories consume disproportionate resources relative to their revenue contribution, creating negative economic value despite positive accounting margins. By incorporating opportunity costs into pricing analysis, these firms can establish minimum price thresholds that ensure projects generate returns exceeding the value of alternative resource deployments.

Dynamic resource allocation models

Leading companies develop dynamic resource allocation models that continuously evaluate economic costs across business units, product lines, and customer segments. These models incorporate both historical performance data and forward-looking opportunity cost estimates to guide investment decisions and operational priorities. Regular recalibration ensures that resource allocation remains aligned with changing market conditions and emerging opportunities rather than following static budgets based on historical patterns.

The most effective models balance analytical sophistication with practical usability, providing clear guidance without requiring extensive data collection or complex calculations for routine decisions. Successful implementations typically feature automated data feeds for accounting costs, simplified opportunity cost templates for common scenarios, and exception-based review processes that flag decisions requiring deeper economic analysis based on predetermined thresholds.

Common Pitfalls in Cost Analysis

Business leaders frequently fall victim to analytical errors that distort cost analysis and lead to suboptimal decisions. Recent Harvard University research reveals that apparent sunk cost fallacy—the tendency to consider past investments when making future decisions—may actually reflect rational behavior when properly analyzed. This finding emphasizes the importance of careful economic analysis rather than applying simplified behavioral rules that may mischaracterize sound business judgment.

The most damaging pitfall involves ignoring implicit costs entirely, leading to decisions that appear profitable based on accounting metrics but destroy economic value. Small business owners particularly struggle with this challenge, celebrating ventures that generate modest accounting profits while sacrificing substantial opportunity costs. A freelance graphic designer who launches a print shop might achieve breakeven on accounting costs while forgoing lucrative design contracts, creating economic losses despite apparent financial success.

Building robust analytical frameworks

Effective cost analysis requires systematic approaches that identify relevant costs while excluding irrelevant factors like sunk costs or emotional attachments to past decisions. Develop checklists that prompt consideration of both explicit and implicit costs for major decisions, establish clear criteria for distinguishing between relevant and irrelevant costs, and create review processes that challenge assumptions about opportunity costs and alternative returns.