Every person who decides to become a music artist, whether as an individual or in a group, dreams of producing that music and making enough profit to live off of it. The music industry is competitive and tough to make it in. However, it is easier to earn money on your music with the internet and music platforms without a significant production company backing you.

There are several ways to use the internet to promote your music and make a profit. However, it can be confusing to get yourself or your group out there and make money. Here are fifteen tips on how to make money with your music.

TIP 1: Do not use a website based on Flash. WordPress themes are much more user-friendly and SEO-friendly. Flash is difficult to use on mobile devices and challenging to deal with, so it is not a great option.

TIP 2: Your website should be easy to read. A music website should always be designed to be easy to read, find, and navigate. Please, do not use inappropriate background colors and images with strange dimensions.

TIP 3: Make it easy for your fans to be in contact. Let people who enter your website know more about you. Create an experience that they will not forget.

TIP 4: Do not allow your website to contain old and outdated content, and there is no current news and little information on what you or your band is currently working on. WordPress makes it easy to update your web page. Updating your music and events can be as easy as writing a text in Word.

TIP 5: If on your website there is no clarity, no purpose, no objectives, you will not be giving reasons for your fans to delve deeper into your website.

TIP 6: You have to control the design of your website. The downside of social profiles is that they are all the same and with many ads and information that distract the visitor. On your website, you can create a brand and make visitors recognize your logo or corporate colors, and the design can be focused on achieving your goals, whether they play a video or a song, buy a new CD, or subscribe to the newsletter.

TIP 7: Your followers have to be yours indeed. It would not be the first time that the number of Facebook or other social media followers changes overnight. If we imagined what would happen if that platform stopped working, the answer would be that we would lose all our followers.

TIP 8: You have to make your visit a pleasant experience. Be wary of using too many ads or other distracting additions to your website or social media pages.

TIP 9: You can and should make every time a visitor enters your site feel comfortable and can perform interesting and logical navigation. You control if you want to be more or less aggressive with your content and requests.

TIP 10: A domain is a sign of being serious. A domain is much easier to remember than the full address that Facebook or Twitter gives us. In addition, the visits we will receive from the search engines will be thanks to the website and the content we publish

TIP 11: Millions of people are present every day on the internet. Capturing a small percentage of users will be easy if you develop a site and other social media pages.

TIP 12: You only have to offer exciting and valuable content to gain a following on the internet and social networks.

TIP 13: It is not necessary to publish every day on all platforms simultaneously. Each social platform has its schedules, public, and favorite posts. Focus on two or three networks where you are strong and focus on the content you publish, and stay constant in the others to reach different sectors of your audience at the same time.

TIP 14: Your website has to be the center of everything, and from it will come the different channels of contact with your followers, blog, social profiles, audio, and video platforms, merchandising. Everything you post on the web will be distributed throughout the internet to achieve a spider web effect, and you will gradually attract followers from different platforms.

TIP 15: Imagine that your website is a train station and that your social profiles are the doors where travelers get on and off your train. It is essential to have a strong presence across several platforms, including music-based platforms, to ensure that you reach the possible followers and fans.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Almost every adult will purchase a vehicle at one time or another. While some may have the ability to buy a car with cash, most will need to take out a vehicle loan. Vehicle loans are unique to other lines of credit in that there are several types of loans you can get to finance your vehicle.

Before you make a car purchase, it is essential that you know and understand the types of loans available and which one will be right for you. If you don’t understand vehicle loans and their structuring, you could end up paying hundreds or possibly thousands more than you should purchase your vehicle. Here are ten types of vehicle loans for you to consider.

Secured Auto Loan

The vehicle acts as security for the debt so. If the borrower cannot make payments, the moneylender can repossess and resell the vehicle to recoup the losses. The legal arrangement for this type of loan is known as a lien.

The lender is registered as a lienholder on the car’s title, giving them the right to own the vehicle until the loan is repaid. This type of loan is how a lender can ensure they will get their money back, whether from the borrower or the resell of the car if it is repossessed.

Unsecured Auto Loan

Unsecured car loans are almost unheard of as most lenders will not issue a vehicle loan without collateral or a lien. However, some lenders will do this for buyers with excellent credit or who have proven trustworthy borrowers in the past.

Simple Interest Loan

A simple interest loan will have interest calculated on the money owed. Therefore, if you put a sizeable down payment or make larger payments than the minimum, you will owe far less because the interest is calculated on the amount of debt left.

For example, if a person paid a $30,000 loan down to $20,000, their interest will only be based on the outstanding $20K. In other words, a simple interest loan is a loan that is offered by lenders that allows a borrower to pay off their debt early to save cash.

Precomputed Interest Loan

With a precomputed interest loan, interest is calculated according to the loan duration and then divided into equal amounts spread over monthly payments. This way of calculating interest is considered more rigid than simple interest.

If a borrower-paid half of their $30,000 loan, they will still pay the same interest every month. Therefore, there is no financial advantage to early payoff or paying more than the monthly minimum.

Direct Financing

Credit unions, banks, and other finance companies give loans to their customers to purchase from a private party or a dealership. Direct financing loans allow the borrower to get pre-approved for the loan before going car shopping, generally with terms better than they can get through the dealership.

Direct financing is the best way to get a vehicle loan because you go shopping already knowing what your payments are and what type of vehicle you can afford.

Indirect Financing

Indirect financing is when the dealership obtains financing for a person looking to buy a car by requesting a loan from a potential lender. Indirect financing is more expensive because the dealership will add to the interest rate to make more profit on the sale.

These lenders are companies linked to a specific automaker or dealership and are not looking out for the best deal for the customer. However, sometimes you can better deal with these companies because they offer attractive incentives like 0% interest and rebates.

In-House Financing

In-house financing is a simple method of financing but can sometimes carry higher interest rates. In-house financing is based on a “buy here, pay here” concept. Therefore, the same dealership selling you the car will finance it.

While this type of financing is more expensive, generally, those with bad or no credit can get a loan and purchase a car. Most dealerships with in-house financing are second (or more) chance financing dealers with a target customer who needs a vehicle without good credit.

Used and New Car Loan

Loans for new and used vehicles usually have different characteristics based on the type and condition of the car and other factors. New vehicles are costlier as compared to the used ones because they have no wear and tear. New auto loans are usually longer than those for used vehicles because the used car’s life is less than that of a new car.

Auto loans for new cars often offer lower interest rates even though the vehicle is more expensive than a used car. That’s mainly because new vehicles are easier for lenders to value if they need to be re-claimed, though the risk of repossession is much lower.

Private Party Loan

Private party loans are for buyers looking to purchase a car from an individual seller instead of a dealership. These types of loans can vary depending on if the owner still owes money to the vehicle or not.

If the owner still owes money but is looking to profit, they will generally raise the monthly payments to be above what they are paying each month. If the vehicle is paid off, the owner can set any terms they would like. Most individual sellers are reluctant to do this type of lending because it is hard to recover payments or the vehicle if they default.

Lease Buyout

A lease buyout is when a person who is leasing a vehicle will opt to buy it. Generally, the payments made on the lease will be factored into the sale price. However, this will be dependent upon the dealership leasing out the vehicle.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Labor Insurance Types: 4 Coverages Your Business Needs

Labor insurance types are the four core coverages every employer needs to protect workers and stay compliant: workers’ compensation, disability insurance, unemployment insurance, and employer liability insurance. Together, these labor insurance types cover on-the-job injuries, income loss when employees can’t work, wage replacement after job separation, and the legal exposure that comes when workers’ comp alone isn’t enough to shield your business from a lawsuit.

After more than 20 years building Complete Controller into a trusted cloud-based bookkeeping and accounting partner for thousands of small and mid-sized businesses, I’ve seen one truth repeat itself: most payroll and compliance disasters don’t start with bad accounting—they start with missing or misunderstood labor insurance. The U.S. Bureau of Labor Statistics reported about 2.8 million nonfatal workplace injuries and 5,486 fatal work injuries in 2022 alone, which means the risk is real and the cost of getting it wrong is steep. In this article, I’ll walk you through each of the four essential labor insurance types, share lessons from the trenches, and give you a practical roadmap to integrate coverage with your payroll and HR systems—so you can protect your people, your profits, and your peace of mind.

What are the key labor insurance types your business needs and how do they protect you?

The four essential labor insurance types are: workers’ compensation, disability insurance, unemployment insurance, and employer liability insurance.

Workers’ compensation pays for occupational injury coverage, medical care, and wage replacement when employees are hurt on the job, and it’s mandatory in most states.

Disability insurance replaces a portion of income when employees can’t work due to a covered disability, sometimes required as a statutory employee benefit.

Unemployment insurance is funded through payroll contributions and provides temporary wage replacement for workers who lose their jobs through no fault of their own.

Employer liability insurance kicks in when workers’ comp isn’t enough—covering legal costs and damages tied to workplace injury lawsuits.

The Four Essential Labor Insurance Types Every Employer Should Understand

These four coverages are the backbone of any responsible labor insurance policy. Standard business insurance—general liability, property, or a business owner’s policy—won’t protect you against employee injury claims, lawsuits, or unemployment disputes. That’s why labor-specific coverage matters.

Here’s the simple framework I share with clients:

Workers’ compensation – primary occupational injury coverage (medical, lost wages, rehab, death benefits).

Short- and long-term disability insurance – income protection for both work and non-work-related disabilities.

Unemployment insurance – a statutory safety net funded through employer payroll contributions.

Employer liability insurance – the legal backstop when employees sue over workplace injuries.

Each one connects directly to your HR policies, job classifications, and payroll workflow. Skip one, and you’ve left a hole big enough to drive a lawsuit through.

Workers’ Compensation: The Non-Negotiable Foundation of Labor Insurance Types

Workers’ compensation is the most universally required labor insurance type—and the one with the highest penalty risk if you ignore it. With 2.8 million nonfatal workplace injuries reported by the U.S. Bureau of Labor Statistics in 2022, even “safe” office businesses face exposure.

Workers’ compensation coverage details

A solid workers’ comp policy typically pays for:

Medical treatment, hospital stays, and rehabilitation after on-the-job injuries

Partial wage replacement while the employee can’t work

Vocational rehabilitation for employees needing retraining

Death and funeral benefits for fatal workplace incidents

The key distinction is occupational injury coverage—if it didn’t happen on the job, workers’ comp generally doesn’t cover it.

Mandatory labor insurance requirements

State rules vary, and worker’s labor compliance depends on where you operate:

California: Coverage required with even one employee; failure is a criminal offense.

Georgia: Required for employers with 3 or more employees.

Illinois: Required for almost all employees whose work is localized in the state.

Alabama: Coverage required by law and serves as the exclusive remedy for workplace injuries.

The federal baseline through the U.S. Department of Labor requires both workers’ compensation and disability coverage for most businesses with employees.

Great payroll starts with great bookkeeping. See how Complete Controller helps protect your business.

Disability Insurance: Income Protection Beyond Workers’ Comp

Disability insurance is the labor insurance type that protects income when employees can’t work due to disability—whether or not the injury happened on the job. It’s often misunderstood as optional, but federally it’s a required statutory employee benefit for businesses with employees in many situations.

Coordinating disability with payroll and HR

Disability premiums typically flow through your payroll insurance system, which means clean bookkeeping makes everything smoother. Short-term coverage fills the gap right after an event; long-term coverage protects against extended absences. Both need to coordinate with workers’ comp and any company leave policies so employees never fall through a coverage crack. A good bookkeeping process tracks disability costs by department and job role, giving you cleaner financial data and faster claims handling.

Unemployment Insurance: The Safety Net Hidden Inside Your Payroll Taxes

Unemployment insurance often hides in your payroll tax line, but it’s a critical labor insurance type that triggers audits if mishandled. According to the U.S. Department of Labor, unemployment benefits typically replace about half of a worker’s previous wages and last up to 26 weeks in many states.

Unemployment insurance as payroll insurance

Unemployment is funded by employer contributions tied to your wages and headcount. The most common mistakes I see in client books include:

Misclassifying W-2 employees as independent contractors

Underreporting wages in multi-state setups

Missing state-specific filing deadlines

These errors aren’t just clerical—they raise your experience rating, drive up future premiums, and can trigger penalties from the IRS. Documenting separation reasons and keeping clean payroll records protects you when claims hit.

Employer Liability Insurance: The Coverage Most Owners Don’t Realize They Need

Employer liability insurance fills the gap workers’ comp leaves wide open. Workers’ comp pays statutory benefits, but it generally doesn’t cover lawsuits when employees claim negligence or unsafe conditions. That’s where employer liability steps in to cover legal costs and damages.

Many contracts now require it explicitly. Loyola University New Orleans, for example, requires contractors to carry workers’ comp plus employer liability at minimum limits of $1,000,000 per occurrence. If your business signs commercial contracts or works on larger projects, employer liability isn’t optional—it’s the price of admission.

Workers’ labor compliance and closing the risk gap

Sit down with your broker and ask one simple question: “If an employee gets hurt and sues us, what happens?” If the answer isn’t immediate and clear, you have a gap.

Real-World Lessons: How One Injury Exposes a Hidden Labor Insurance Gap

In 2004, two teenage workers died in a Wisconsin sawmill. The employer was later convicted on homicide-related charges—proof that a serious workplace incident can spiral from medical claim to criminal case overnight. Workers’ comp covered medical costs and statutory benefits, but the legal exposure went far beyond what any standard policy could absorb.

What I’ve learned helping clients navigate labor insurance claims

Many founders I’ve worked with assumed their general liability policy covered employee injuries. It almost never does. The most successful approach I’ve seen ties each labor insurance type to a specific risk: injury (workers’ comp), disability (disability insurance), job loss (unemployment), and lawsuit (employer liability). Clean payroll data, documented job roles, and accurate classifications make every claim faster and cheaper to resolve.

Building a Practical Labor Insurance Policy Mix

Start with three honest assessments: your headcount, your industry risk, and your contractual obligations. From there:

Confirm workers’ comp thresholds in every state where you employ workers.

Add federally required disability and unemployment coverage.

Layer in employer liability with appropriate limits.

A reputable licensed agent and a strong bookkeeping partner can make sure your premiums match your wage categories, your class codes are accurate, and your renewal isn’t full of surprises.

Bringing It All Together: Protecting Your People and Your Business

Workers’ compensation, disability insurance, unemployment insurance, and employer liability insurance aren’t just policies—they’re the financial controls protecting your cash flow and your continuity. I’ve watched these four coverages turn fragile operations into resilient businesses that survive accidents, audits, and lawsuits. If you don’t design your labor insurance mix intentionally, regulators and plaintiffs’ attorneys will design it for you.

Audit your current coverage, verify compliance in every state where you operate, and build a simple claim documentation process. When you’re ready to align your bookkeeping, payroll, and labor insurance strategy, visit Complete Controller and let our team help you build the financial backbone your business deserves.

Frequently Asked Questions About Labor Insurance Types

What are the main types of labor insurance a small business needs?

The four essentials are workers’ compensation, disability insurance, unemployment insurance, and employer liability insurance. These differ from general liability or a business owner’s policy because they specifically protect against employee-related risks—injuries, income loss, job separation, and lawsuits.

Is workers’ compensation insurance mandatory for my business?

In most states, yes. California requires it with even one employee, Georgia requires it at three or more, and Illinois requires it for nearly all in-state employment. The federal Department of Labor sets a baseline requiring workers’ comp and disability coverage for businesses with employees.

What’s the difference between workers’ compensation and employer liability insurance?

Workers’ comp pays statutory benefits for workplace injuries—medical bills, lost wages, rehab. Employer liability covers legal costs when an employee sues you over a work-related injury or unsafe conditions that go beyond what workers’ comp will pay.

How do I file a labor insurance claim for an injured employee?

Report the injury promptly, provide the employee with required notices and claim forms, document everything, and follow your state’s timeline (California, for example, requires one-day response on certain forms). Keep HR, operations, and finance coordinated.

How often should I review or update my labor insurance coverage?

Review annually at renewal, and any time you hire in a new state, add new job roles, or sign a contract with specific insurance requirements. Coverage that fit you last year may not fit you this year.

Sources

ADP. “Workers’ Compensation Insurance in California Explained.” ADP Resources. https://www.adp.com/

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Jennifer BrazerFounder/CEO

Jennifer is the author of From Cubicle to Cloud and Founder/CEO of Complete Controller, a pioneering financial services firm that helps entrepreneurs break free of traditional constraints and scale their businesses to new heights.

Brittany McMillen is a seasoned Marketing Manager with a sharp eye for strategy and storytelling. With a background in digital marketing, brand development, and customer engagement, she brings a results-driven mindset to every project. Brittany specializes in crafting compelling content and optimizing user experiences that convert. When she’s not reviewing content, she’s exploring the latest marketing trends or championing small business success.

When you are eighteen and receive all those credit card offers in the mail, it may seem easy as “free” money. It is challenging to get off once in the way of reckless credit card expenses, and you can get into serious trouble. Credit card debt is not impossible to eliminate, and in many ways, it is like any other type of debt. To manage your credit card debt, you need to have a financial plan and the self-discipline to carry it out.

The debt is all the same when it comes to this; whether it is mortgage debt, personal debt, car debt, or credit card debt, eliminating that debt all boils down to the same simple principles. It would be best if you had a plan. Sit with your spouse, by yourself, or with a financial advisor if necessary, and outline how you must manage your finances so that you can free yourself from your growing mounds of debt. When making your financial plan, collect all your accounts and your information so you can see everything at once. When you can see all your financial obligations side by side, it is easier to see where your money is most needed to go. (A chart is an excellent and quick way to see everything at once).

Make a priority list of your payments. Pay the most urgent needs first and then move on to your fewer binding obligations.

With what compensation, you are focused on trying and paying more than the minimum amount. It will take much longer than you want to pay off your debt if you only pay the minimum. Budget your money so you can spend even a little more than the minimum (you also do not want the interest to keep accruing-pay it off fast!)

Another thing to keep in mind is to pay the smaller balances at first. You have more time and resources to deal with your large balance bills when you get them in the way. Get the “extra” more minor things out of the way, and you can fine-tune your most significant debt.

If you can, stop using your credit cards altogether (at least for a while). When you can get an idea of your debt and what it’s worth, the next time you think about a credit card, you better know how to handle the situation and what to look for. If you have your credit cards for at least a few months, then you can start with a clean slate and work on improving your probably damaged credit score. Eliminate the temptation, and the problem will be easier to remedy.

The reduction (and eventually elimination) of your credit card debt has planning and discipline in mind. You can do it, and all you need is a plan. A plan is the best place to start, and freedom is the reward at the end of the tunnel.

There is no need to spend money on reducing credit card debt as it is the most cost-effective for all. But you cannot consider it the best way to reduce the aspect of all financial situations. What are those exact techniques that are only suitable for reducing debt removal? Several strategies include the following one as the most effective one.

If you want to get rid of all debts, you will have to prioritize the debt payment process. For this, you will have to eliminate the highest APR debts from the lowest ones. It means to pay those debts that have an immense amount you owe then. You will move towards the lower ones. After the payment of all debts then, you can save money on total interest rates.

In the end

If you want to multiply your cash flow, you will have to streamline your budget well. It is only possible when you pay all your bills, including the credit card, on time. Quick cash flow not only maximizes your sales, but it also helps you in reducing debts so fast. Spend as much on your debts rather than others.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Even in the best of times, running a company is challenging. However, during a recession or other economic downturn can seem impossible. In most cases where recession is the distressing factor, there is a warning that it is coming. Therefore, with the proper preparation, your company can survive a recession.

A recession comes from consumers spending less due to overall economic-financial stresses. This fall in spending then slows the flow of money in small and large businesses. Most larger companies will whether a recession, but many small businesses will fold under economic pressure.

The fall in this spending is worrisome since it represents a considerable percentage of the country’s economy and almost always grows, albeit slowly. Even in the last recession of 2001, consumer spending in the US never fell, only slowed its growth.

Because of Covid-19 and a sharp rise in gas prices and taxes expected this year, a recession is looming over the horizon. Many economists predict it to be worse than the last recession felt by the US and warn companies to prepare themselves to weather it the best they can.

Consumers are not only concerned about paying their debts; companies are also suffering. The process of “deleveraging” is typical of a recession, but reversing the credit operations made through external financing (“leveraged purchases”) can be a violent measure.

Because many companies have debt and other ongoing expenses, it is suggested that business owners find a way to overcome the deficit and pad their revenue. Further steps need to be taken to safeguard against a recession.

Don’t Wait

In a recession, you must find a way to continue to operate your company. How? The wisdom and experience of other executives and consultants can guide you in taking the steps.

As in any critical situation, much depends on the speed of your actions. It is in our nature to avoid facing bad news and imagine that problems will be solved quickly and easily. But all experts advise doing just the opposite: assume that circumstances will worsen more than you expect.

“Assuming the worst scenario, you will identify the areas where you think you will be most efficient, then you’ll just have to get down to work,” suggests Intuit CEO Brad Smith. Anticipating future reality before your competitors can make a difference when it comes to survival.

The most effective decisions and actions that you can make to prosper during a recession are worth saying, the ones you established from the beginning. In times like this, the strong gets more robust, and the weak end up as devoured.

For example, in the third quarter of 2008, when Washington Mutual and IndyMac banks went bankrupt, Bank of America (which disposed of subprime mortgages in 2001) attracted 21 million new deposits as consumers sought security.

Something similar happened with the furniture chain, Wickes. When it declared bankruptcy, more than 100 trucks transported furniture to its stores, then the retailer -who had taken care of its financial health- acquired all the furniture chartered at a bargain price.

Remember those lessons for the next. For now, what is done is done. Regardless of the type of business you run, the following ten recommendations will benefit you:

Adjust your priorities to the new reality: if before your focus was to expand to new markets, expand the workforce or increase profits, you must change direction, assume another mentality that helps you to face the crisis, like being more frugal, avoiding unnecessary expenses and weigh any investment.

Keep investing in the essentials: never stop financing the pillars of your company (be it customer service, innovation, employee training, etc.)

Always communicate, balancing realism and optimism: many executives often enter a period of silence when they go through uncertain times and have no answers. Good managers communicate more than ever in those moments, employees want to know your point of view, and you have to be honest and direct, keep hope alive, give confidence and reaffirm the company’s leadership.

Look for new solutions to your clients’ new problems: no matter what your business is, you can constantly redefine the value for the client and propose strategies that benefit both.

Do not rush to cut prices: reducing prices is not always wise because you have to generate more sales; now is the time to study your market and measure price sensitivity.

Focus on the capital, how you will get it and how you will use it: in times of fat cows, the most critical business rule is forgotten: to earn a return on capital that exceeds the cost of capital. As the credits are lax and at low rates, you leave aside the importance of the sources of capital and their efficient management.

Reassess your staff: it is an essential task because you choose well if you get to lay off workers. Do not make the mistake of punishing your best employees by reducing their salaries or bonuses due to the recession. Take care of them.

Re-examine the compensations and incentives: what are incentives? Learn from the Wall Street case, whose programs incentivized risk; hence everyone would want to win regardless of the consequences. You can implement a system that encourages your workers in the long term to see the recession as part of a more promising cycle.

Think twice about offshoring: it is not profitable to manufacture in China and Malaysia in some industries. The wage gap is no longer significant, and transportation costs often make it less attractive to offshoring. Also, think about taxes, tariffs, and speed. Offshoring is not always the best option.

Analyze acquisitions and mergers with intelligence: If you have adjusted your belt, you can not follow Warren Buffett’s advice to be ambitious when others are fearful, but if your finances are solid, then it is time to act. It is an excellent opportunity to acquire small businesses and make their talent.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

First, it would be prudent to understand the Quantity Theory of Money (QTM) and its relation to inflation. Essentially, QTM is a theory that can be the primary cause of changes to money’s purchasing power. What QTM primarily derives is that any effect on the price of money, such as deflation percentage, interest rates, etc., is determined mainly by the currency in circulation.

When money supply shows an increasing trend instead of money demand, which is less, the consumer has to withstand the worst price increase of commodities. In other words, purchasing power falls. If the money supply decreases and money demand rises, the purchasing power also climbs, and regular prices fall. To put it simply, an increase in money supply and a decline in money demand are related, and therefore the rate of inflation increases.

Secondly, QTM suggests any monetary policy impact by a central bank, which could be a change in Cash Reserve Ratio (CRR), discount rate, or Open Market Operations (OMO), will primarily affect the inflation preceded by the desired price level. To put it simply, this is a cause-and-effect relationship, where the money is an active variable, and the price level is the passive-dependent variable.

Review of the QTM and its assumptions

Initially, teething issues did come into play while determining the QTM to create a much more plausible association between money supply and demand. Therefore, it became imperative to formulate a simple equation, i.e., P=V + M – Y, where (P) denotes Inflation rate, and V, M, and Y as the growth rate of money output, velocity, and stock (currency in circulation).

Any change between money supply and demand, whether minimal or substantial, is bound to affect the rate of money growth and, consequently, the inflation rate. Primarily the notion behind this theory is that the velocity and growth rate of money will remain constant.

An increase in circulation in circulation will have no influence on Real Gross Domestic Product (GDP) growth in the long run.

A good amount of experimental findings of the QTM considers the velocity and growth rate of money as a constant variable. However, on the contrary, the postwar US data reveals the velocity of money is a theoretical concept by considering it as a constant variable. Instead of pretentious that the velocity of money is a constant variable, we can rework the above equation of QTM to V= P + Y – M, allowing changes and directly affecting inflation, output, and money.

The relationship between money growth and inflation

In addition to the above, we can also divert our perception in determining the scopeof money. If we use US data, we can quickly discover that the accumulated “nominal output plus and stock market capitalization” is narrowly associated with the currency in circulation, which in turn supports one of the pivotal propositions by Milton Friedman. Thus, we can conclude that the monetary policy must keep a close watch on the money supply factor to foil the end-users and asset price inflation.

There is sufficient realistic data that supports the hypothesis that growth in the money supply will affect the end consumer and the price of products and goods.

Objectives and tools of the Fed’s monetary policy

Central banks governing the conduct of the economic policy of the central reserve bank in an environment, which is prone to low inflation, needs a close look. Controlling inflation and price is viewed as one of the pivotal questions facing central banks worldwide. By re-engineering an efficient regulatory framework, including transparency and freedom from socio-political influences, central banks worldwide have primarily achieved their directive.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

The mortgage business has seen different variations since the housing crash in 2008. However, with different views, it will be the death of the mortgage business. The crash became a chance for the mortgage brokers to choose better impeccable services and products. Creating your account needs more than only getting your mortgage license. You should finish all necessary documentation by the nationwide mortgage licensing system (NMLS).

Establish a business entity

Before you can list with the NMLS, you must make a business entity. Go to the secretary of state with your chosen business name. Find the business listing to ensure you have chosen a different name because the business name cannot finish. Complete the registration and then visit the IRS website to select a tax identification number. After you contain these, continue with NMLS application procedures.

NMLS Registration Process

The NMLS listing or registration registers companies and individuals for the mortgage processing services. However, this is a federal need; it is checked at the beginning level—Cheick and your state NMLS regulatory department for charges within your state. If you contain a license as an individual, ensure that you are not licensed with a federally regulated institution like a bank.

This designation has various needs, and you night required to fulfill extra paperwork or testing if you have this mortgage license designation. If you are not licensed, pass the needed NMLS team and have the licenses.

Create a business plan

If you are willing to start your business self-sufficiently, you will need to plan help to create your structure and explain your objectives to potential employees and investors. Explain the industry you want to reach and how you plan to focus on them. As the mortgage business is crowded, you will have to find how you intend to make and fill a niche in the market in the face of stiff competition.

Finish forms and provide documentation

Finish the form MU1 filing. This is a needed application for all new units. It contains the basic organization information or data and the economic history of the organization and the officers. Finish this in detail to save delays or denial. Give any supplemental documentation needed. Finish a credit check and background.

If you plan to be a mortgage loan provider – the original lender- some additional economic documents are needed in the application procedure. Most mortgage organizations broker the loan out looking for a suitable situation for their customer and are not loan providers.

Bonds and insurance

The NMLS needs a security bond. A surety bond is a forte insurance product that gives minimal protection. Based on your state. You required a bond ranging from $25,000 to $75,000. If a customer experiences a loss because of your business, the bond pays the customer, and the bond organization reclaims the charge from you.

It is wise to also get other relevant insurance strategies. Any workspace needs a usual liability building protection and policy. However, this policy needs leases and positive to have, would not safe you from client claims if your company makes issues.

For this, you require professional liability and insurance. Communicate with a commercial insurance agent for the correct rules in your state.

Basic mortgage business logistics

Various mortgage conducts the mainstream of their business online and moves part from brick-and-mortar space; however, this can be a challenging benefit to fascinate customers who want to calmly sit and review their economic situations. Whether or not you contain physical space and maintain a way of communication with customers that is efficient and quick.

Maintain relationships with mortgage financers that underwrite loans. Contain a series of lenders and banks that work with brokers to provide loans, equity lines, and refinances.

Hire qualified staff

Establish how many different mortgage brokers you would like to hire and the pay scale. It is normal for most mortgage brokers to work on commission or a salary plus commission plan. Select a program that motivates employees and attracts talents.

Market your business

Start a company website and phone lines and get business cards. Start networking with national, local real estate agents to grow power partnerships. Utilize social media to spread the word.

Bottom line

If you are beginning out at a one-person company, you do not require a team. Although a small mortgage brokerage business generally has a team of 3 to 4 people. You might work as a loan officer. You might require someone to answer the queries.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

Investment funds are among the most attractive products to grow your savings due to their versatility and high diversification capacity. Before signing any contract, it is important to clarify some basic concepts. People consider such funds a mutual fund or an investing vehicle. It has an asset portfolio that investors purchase. As a financial professional, you can manage your assets by establishing mutual funds. You can also attempt them to produce returns on investment for their investors. Most retired people use investment funds and save their money in an individual retirement account.

What is an investment fund?

The investment funds are Collective Investment Institutions that add the contributions of many savers to manage them through a single-vehicle.

A fund will invest in different assets to obtain maximum profitability within its investment policy. To understand it better, a fund takes the money from its savers and moves it by buying shares, bonds, treasury bills, and other funds.

In this sense, there are different funds, depending on where they invest and how they do it. Thus, one can speak of fixed income, variable income, mixed, global, guaranteed funds of funds, or real estate funds. At the same time, it is possible to distinguish between passive or active management funds and accumulation and distribution funds.

Those who participate in the funds

It is also necessary to know who is involved in its operation to understand how an investment fund works.

Everything starts with the participants, that is, the savers. The unitholders are the fund’s owners, which divide its assets into shares.

A management company manages the fund as its name indicates who manages the fund and who decides how and where the money is invested.

More than one fund manager cannot manage a fund, but a fund manager can have several funds.

In addition to the manager, there is the figure of the fund’s depositary, who will be the custodian and monitor the assets that make up the fund. This entity must be registered with the CNMV.

How an investment fund works

The basic operation of an investment fund is very simple. The participant who wants to invest acquires shares of the fund. The manager is responsible for making money, and the fund grows.

The shares are the aliquots or parts that form a fund. Unlike the actions of a company, it is not a fixed number since, at any given time, there may be someone who sells theirs or who buys new ones.

The price of each share will be determined by dividing the fund’s assets between the number of shares, which will be the purchase or sale value at a particular time. It can vary by the entry or exit of investors or by changes in the market value of the assets that make up the fund. The latter will affect the performance you get from a fund. As an investor, you can choose to withdraw your money from the fund at any time. However, some have specific windows for withdrawal.

Commissions of the funds

Like most financial products, mutual funds charge a series of commissions to the unitholders. These commissions have to do with both operations and custody. These commissions are marked by law and can never exceed the following percentages for each of the following concepts:

The subscription fee is paid to the fund manager for investing in the fund and is calculated as a percentage of the capital invested, which means that in the end, you invest less than you think.

The reimbursement commission is charged when selling the fund’s holdings.

The management fee is paid to the manager for their services, investing the fund’s money. This commission is accrued daily and is already deducted from the net asset value. In other words, it subtracts from what your shares are worth. In general terms, active management funds will be more expensive than passive management funds.

A commission for success can be added to the management committee, which will subtract up to a maximum of 9% of the profits obtained by the fund.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

The opinions expressed by the employees of entrepreneurs are personal. An entrepreneur is exposed to certain risks from the day his company starts, even before hiring the first employee.

A lawsuit or a catastrophic event outside the company’s control is enough to destroy a business before it can react. Fortunately, numerous types of insurance can save your business and avoid the pain of an external event to end with him and your dreams.

However, there are situations that a large percentage of small and medium enterprises face equally and can be prevented with good insurance.

Here we explain five types of insurance for your company.

Company owner policy

Provides liability coverage if a member or a product of your business causes damage to third parties.

It also protects in case of suspension of activities. The coverage applies to the actual loss that the business has had because of the interruption of activities derived from a loss that is covered by the policy. For example, can you imagine the losses that Do they generate in a call center if the light is cut by a thunderstorm one day?

Although no insurance covers the needs of each business, many business products are highly customizable.

Property damage insurance

Here we talk about securing equipment, inventory, workspace, furniture, etc.

Suppose that there is a fire in your workspace for some reason, there is a robbery. There are strong winds that destroy part of the furniture. How much would it cost to replace all your work material? Even if your business is in your own home, you should consider insurance of this type.

There are natural disasters, such as a flood caused by a hurricane or an earthquake, whose damage will probably not be covered by a standard policy.

In other cases, property damage insurance does not cover damages for the deterioration (use) of the property itself. Ensure that your policy covers losses outside the property, especially if you frequently travel outside the company with valuable products.

Medical expenses insurance

Although the type of work that employees develop is relatively low physical effort, not having this insurance can result in a costly demand in case of not having coverage and suffering an accident during working hours.

Vehicle insurance

Hire auto insurance covers (at least) damages to third parties to the employee who drives it, protecting the automotive unit.

If the employee uses his unit for work purposes, this must also be insured and protect both the driver and third parties.

Life insurance

Some insurers include this benefit under a payroll deduction scheme, allowing companies to have life insurance for their employees without disbursing large amounts of money. This insurance consists of providing a sum of money to the family member, designated by the employee, in death.

Insurance for your business is as personal as your company needs it. The most common coverages are those against fire, theft of merchandise, and general civil responsibility. The total insurance premium with the basic coverages is between $1,800 and $3,000, depending on the business requirements.

Having protection for your company is as essential as your car or your medical expenses insurance because it means the difference between the loss of your business or its success. Insurance for your business will always be budget able. A catastrophic event without insurance never will be.

Crucial considerations before purchasing business insurance

Conduct thorough research to find out the best business insurance plan.

If you are a newbie in the business field and do not have an idea of upcoming risks, you should hire experienced professionals and select accordingly.

Check all your needs and make a list of them before a planned purchase.

You will inform your insurer fast if you need extra coverage for the damages that occurred due to disasters.

Identify your business peril to buy a plan. You must have maximum coverage for damages, and its premium costs must be affordable.

You can get higher insurance coverage against your requests. Only you will have to deduct an insurance amount to minimize it.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

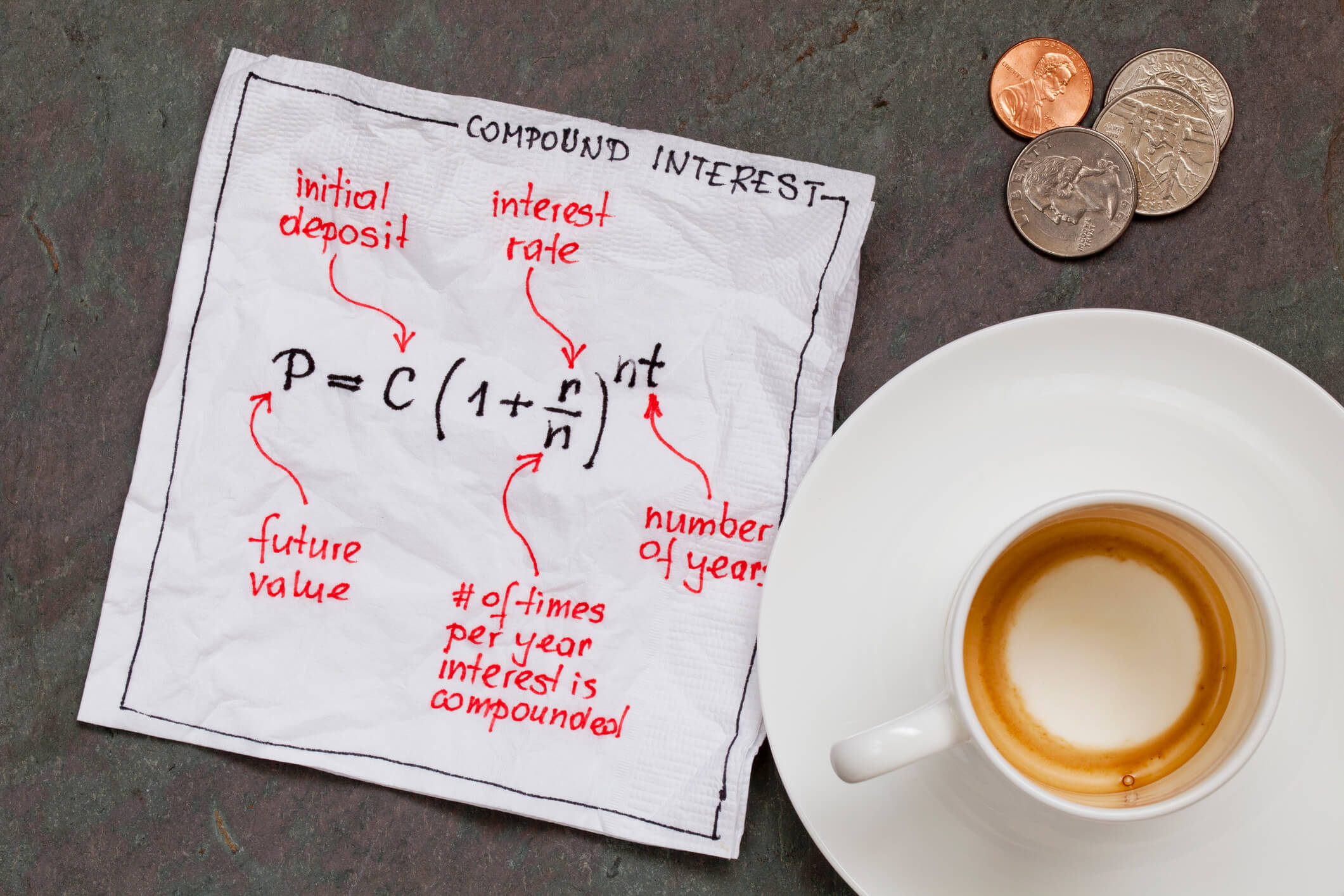

When managing the finances, it is best to have a clear picture of all financial concepts, including simple and compound interest. Simple interest is easily understandable by all. It works simply with the principal amount, and a fixed rate of interest is paid or earned after fixed time intervals. Things get complicated under the light of the compound interest.

What is compound interest?

Unlike simple interest, compound interest applies to the sum of the initial principal amount and the accumulated interests from the start on loan or a deposit. In the case of a deposit, it can work miraculously in growing the deposit. While in the case of repayment of the loan, if not paid regularly, an individual ends up paying way more than the initial amount. The amount earned or paid at the end depends upon the length of the compounding period. The amount payable at the end of the compounding period of two years will be lower than the amount payable at the end of a compounding period of five years.

Working of compound interest

Interest applied on previously earned interest is the perfect way to define compound interest and its working. It is a continuous cycle, and it paves the way for the exponential growth of the principal deposited amount.

To understand the working of this concept, take an example of a person who deposited $100 in the bank at an interest rate of 5%. At the end of the first interest period, the person earns $5 over the deposit. A person will keep earning a fixed amount of $5 at the end of every interest period in simple interest. But in compound interest, the person will make $5 over the first period. Over the next period, the person will not earn interest on the principal amount of $100, but it will be applied to $105 instead.

That is why compound interest works wonders for people who deposit their savings in the bank and works against the borrowers. It is because, with time, the principal amount will increase if there is a slight error in estimation. Borrowers end up paying way more than they borrowed.

Perfect use of compound interest

The working of compound interest is greatly beneficial if used in the right manner. Here are ways through which people can ensure that it works in their favor.

Starting early savings

Compound interest is an ideal saving technique for people who have the patience to leave their money untouched for a long time. The first two to three interest periods will not bring big returns, but with time people can earn huge amounts just by keeping their money in one place. The earlier a person starts saving, the higher will be the amount earned at the time of retirement. It also covers the period during which a person fails to save due to increased monetary burdens.

Debt payment

People who have borrowed a loan with compound interest smartly dealing with it can help them pay with much ease. Borrowers must try to pay extra payments if their budget allows. It helps in preventing the balance from growing and helps in a quick repayment of debts. Another way to handle compound interest smartly is to keep the amount borrowed amount as small as possible.

A smart move for savers is to deposit the amount saved in the banks. Without putting in any effort, they will be able to earn money on their saved amount. Time is key; therefore, the longer these savings are kept in a bank, the higher the returns will be. So being patient and allowing the returns to mature is the best option.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.

About Complete Controller® – America’s Bookkeeping Experts Complete Controller is the Nation’s Leader in virtual bookkeeping, providing service to businesses and households alike. Utilizing Complete Controller’s technology, clients gain access to a cloud platform where their QuickBooks™️ file, critical financial documents, and back-office tools are hosted in an efficient SSO environment. Complete Controller’s team of certified US-based accounting professionals provide bookkeeping, record storage, performance reporting, and controller services including training, cash-flow management, budgeting and forecasting, process and controls advisement, and bill-pay. With flat-rate service plans, Complete Controller is the most cost-effective expert accounting solution for business, family-office, trusts, and households of any size or complexity.